23rd Oct 2025. 9.07am

Regency View:

BUY Polar Capital (POLR)

Regency View:

BUY Polar Capital (POLR)

Polar Capital: Quality, cash and consistency

It is not often you find a mid-cap fund manager offering a forecast dividend yield above 8%, trading on less than 10 times earnings, and carrying one of the highest quality scores on the market. Yet that is exactly what you get with Polar Capital (POLR). The boutique asset manager has just delivered a record quarter for assets under management, signalling that sentiment toward active managers may finally be turning a corner.

A specialist fund manager with global reach

Polar Capital is one of the City’s better-known specialist asset managers, managing £26.7bn in client money across a range of thematic, regional and sector-focused funds. The firm’s strategy has always been clear: stay focused on active management, keep capacity limited to preserve performance, and build deep expertise in niche areas rather than chasing scale.

Its funds cater primarily to institutional investors and wealth managers seeking differentiated exposure, whether that is through the flagship Technology Fund, Emerging Market Stars or Japan Value strategies. This boutique model has given Polar the flexibility to move quickly and attract top-tier managers while keeping overheads low and margins strong. Even as some competitors have struggled with fee compression and outflows, Polar has continued to prove that a focused model can deliver both performance and profitability.

With just over 200 employees and a strong balance sheet, the group remains small enough to be nimble but large enough to sustain meaningful fund flows. Its high returns on capital, consistently above 35%, demonstrate the underlying quality of the business and its ability to generate healthy profits even in challenging market conditions.

Momentum returns as assets hit a record

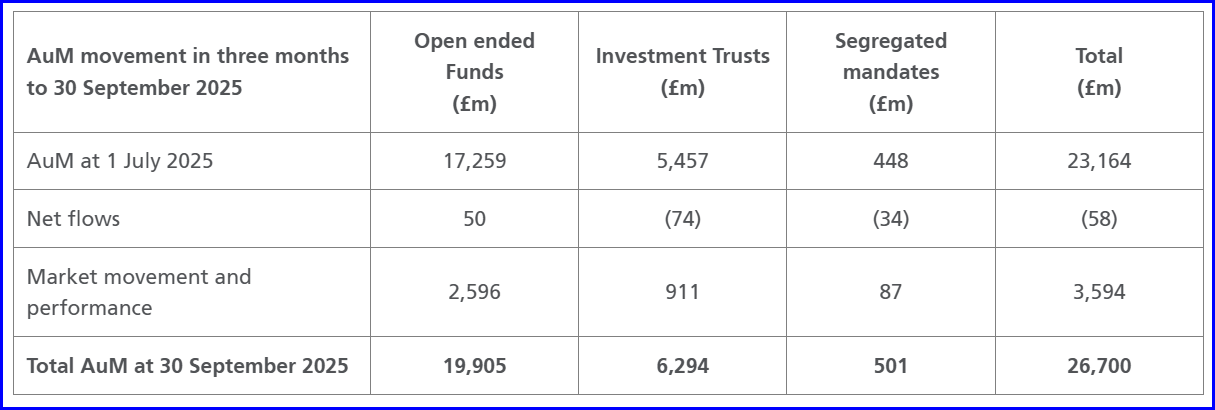

After a tough spell for active managers, the tide appears to be turning in Polar’s favour. The company’s latest quarterly update showed assets under management rising 15% over the three months to 30 September, hitting an all-time high of £26.7bn. That growth was driven by £3.6bn of positive fund performance and market movements, offset by modest net outflows of just £58m, a fraction of the £632m lost in the prior quarter.

The rebound reflects improving appetite for Polar’s higher-growth strategies. The Technology and Artificial Intelligence funds both attracted fresh inflows, with the Global Technology Fund pulling in £226m after outperforming its benchmark by 18% year to date. Other growth-oriented funds such as Emerging Market Stars and Biotechnology also saw net inflows, while European and UK strategies remained out of favour.

Chief Executive Iain Evans, who took the helm earlier this year, struck a confident tone in his commentary. He pointed to signs of a more supportive environment for active managers, a slowdown in redemptions and stronger fund performance across the board. For investors, the key takeaway is that Polar’s core specialisms, particularly technology and innovation, are once again in demand, setting the stage for stronger earnings momentum through 2026.

Financial strength and valuation appeal

From a numbers perspective, Polar’s investment case rests on three pillars: quality, value and income. The company’s quality metrics are outstanding. Return on capital sits at 37%, operating margins are north of 22%, and the balance sheet carries net cash of £176m. These figures underline a disciplined business that converts a large portion of its revenue directly into free cash flow, over 80p per share in the last full year.

Valuation remains compelling. At 539p, Polar trades on a forward P/E of 9.9 and an EV to EBITDA multiple of just 6.6, well below the sector average. Its price-to-free-cash-flow ratio of 8.5 highlights that investors are paying very little for a business with a long track record of consistent profitability. With analyst forecasts pointing to modest earnings growth of 8% this year and 17% next, there is scope for a gentle re-rating if momentum continues.

Then there is the dividend. Polar has paid a steady 46p per share since 2022, equating to a forecast yield of 8.6%. Dividend cover is expected to improve to around 1.2 times as profits normalise, and management’s conservative approach to payouts means that income investors can rely on a steady stream of cash. For those seeking income in an uncertain market, few AIM-listed financials offer this combination of yield, coverage and quality.

It is also worth noting the company’s prudent capital structure. With a current ratio of 2.6 and no meaningful debt, Polar is well placed to maintain dividends through market cycles. Cash represents more than 80% of total assets, offering ample flexibility for investment, buybacks or special distributions if management sees fit.

Momentum indictors turn bullish

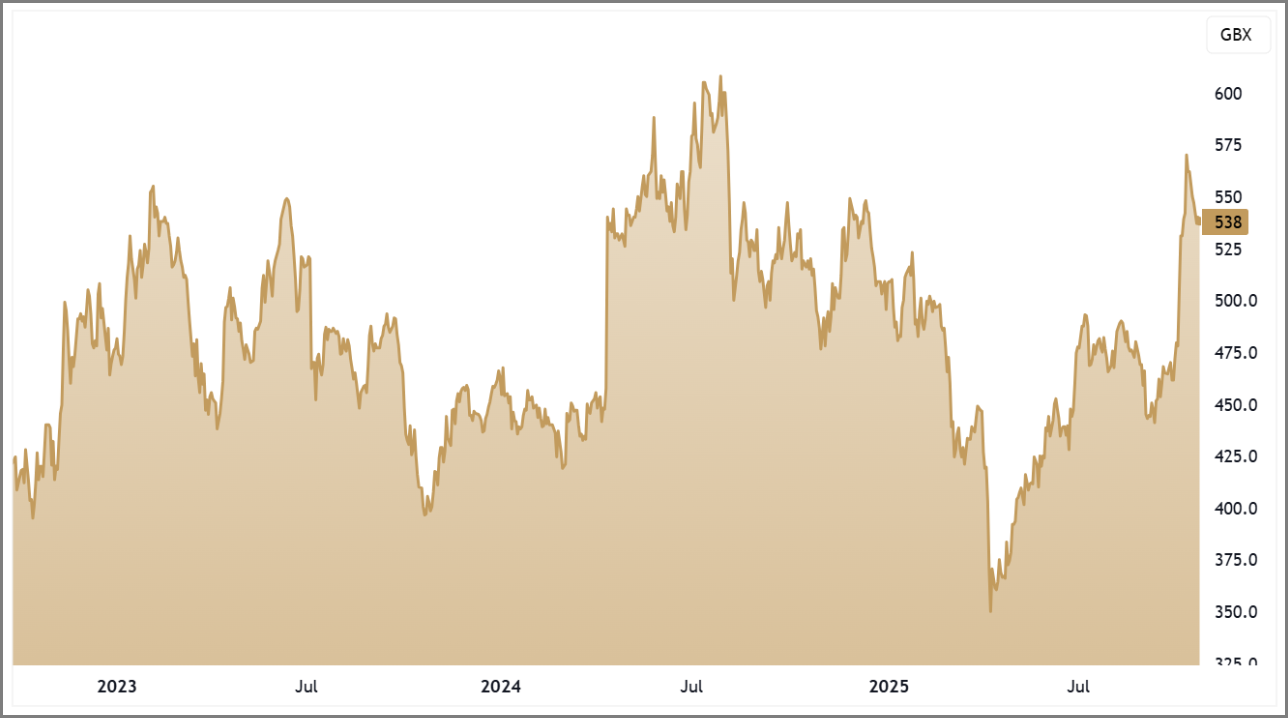

Technically, the picture has improved dramatically over the past six months. After forming a long base around 340p, the shares broke decisively above the 200-day moving average in September, with the 50-day crossing higher, a bullish signal of trend confirmation. That breakout was fuelled by the AuM update and the return of confidence in growth-oriented funds.

Prices have since pulled back slightly from recent highs near 580p, consolidating above former resistance levels in the low 500s. This kind of pause following a breakout often represents healthy consolidation of gains rather than exhaustion. As long as the shares continue to hold above the 50-day moving average, the broader uptrend remains intact.

From a trend perspective, the story is one of re-rating. The market appears to be rewarding Polar’s combination of quality and income after two years of relative underperformance. Momentum indicators support that shift, with six-month relative strength up 30% and the shares now trading comfortably above both major moving averages.

For investors seeking exposure to a profitable, cash-generative business with momentum building on both the charts and in the fundamentals, Polar Capital ticks every box. It is a rare blend of value, income and quality, and right now it is delivering on all three.

Key takeaways

1. Record assets under management: Polar Capital’s AuM rose 15% in the latest quarter to a record £26.7bn, reflecting strong fund performance and a sharp slowdown in outflows.

2. High quality metrics: The business consistently delivers returns on capital above 35% and operating margins above 20%, underlining its reputation as one of AIM’s most profitable asset managers.

3. Exceptional dividend yield: With a forecast yield of 8.6% and expected cover of around 1.2 times, Polar offers one of the most reliable income streams in the financials sector.

4. Attractive valuation: Trading on just 9.9 times forward earnings and 6.6 times EV to EBITDA, the shares remain undervalued relative to peers despite recent gains.

5. Technical momentum building: The recent breakout above long-term moving averages confirms a change in trend, with prices consolidating above former resistance as investor confidence returns.

POLR 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.