4th Jun 2026. 9.00am

Regency View:

BUY Personal Group (PGH) Second Tranche

Regency View:

BUY Personal Group (PGH) Second Tranche

Growth, Income and a Second Bite

Back in August last year, we first highlighted Personal Group (PGH) as a business quietly building momentum beneath the surface. Since then, the company has continued to deliver exactly the sort of progress we hoped to see, with strong earnings growth, expanding partnerships and a steadily improving market position.

While many AIM shares remain heavily dependent on a single product, customer or catalyst, Personal Group’s strength comes from something far less exciting but arguably far more valuable: recurring revenues, high customer retention and a business model that becomes more relevant as financial pressures on employees continue to increase. The shares have responded accordingly, climbing to fresh highs in recent weeks.

Importantly, the investment case no longer rests on what management says it plans to do. It is increasingly about what the business is already delivering. With trading momentum continuing into 2026 and several new growth initiatives gaining traction, we believe there is a strong case for adding a second tranche to our position.

A Business Built on Retention

Personal Group operates in the workforce benefits and insurance market. Put simply, it helps employers provide insurance products, healthcare benefits and wellbeing services to their employees.

The group generates revenue through two core divisions. The first provides employee-paid insurance products that offer financial support when workers are unable to work through illness or injury. The second provides employee benefits technology and wellbeing services through its SaaS platform.

What makes the model attractive is the recurring nature of the revenue. More than 90% of group revenue now comes from recurring insurance premiums and software subscriptions. Once employers and employees are onboarded, relationships tend to be long-lasting, creating predictable cash generation and strong visibility over future earnings.

As labour markets remain competitive and employers continue to focus on staff retention, benefits packages have become increasingly important. That creates a favourable backdrop for Personal Group’s products and services.

Partnerships Open New Doors

One of the most encouraging developments over the past year has been management’s success in expanding distribution through strategic partnerships.

In March, Personal Group announced a new partnership with Simplyhealth, one of the UK’s largest healthcare providers with more than 2.5 million members and approximately 12,000 corporate client relationships. The arrangement allows Personal Group to introduce its insurance products to a significantly larger audience while combining them with Simplyhealth’s healthcare offerings.

This follows the company’s earlier partnership with Sante and forms part of a broader strategy to accelerate growth through third-party distribution channels.

Meanwhile, management continues to make progress through its relationship with Sage, helping drive further penetration into the SME market. The latest AGM statement highlighted continued benefits platform growth alongside strong new insurance sales and ongoing momentum across its partnership network.

Taken together, these developments suggest that growth is becoming increasingly diversified and less reliant on any single sales channel.

Strong Growth Backed By Strong Cash Generation

The latest full-year results demonstrated that operational progress is translating into financial performance.

Revenue increased 11% to £48.3m during 2025, while adjusted EBITDA rose 22% to £13.2m, ahead of market expectations. Normalised earnings per share increased 24% to 22.2p.

Perhaps most impressive was the growth in shareholder returns. The full-year dividend increased by 41% to 23.3p per share, continuing a long track record of cash distributions.

The balance sheet remains a major strength. Net cash increased to £24.6m, equivalent to almost 20% of the company’s market capitalisation. That financial flexibility gives management room to continue investing in growth initiatives while maintaining an attractive dividend policy.

Looking ahead, analysts expect revenue to increase from £48.3m to approximately £54.4m this year, while earnings are forecast to continue moving higher. Management has also outlined ambitious longer-term targets of £100m revenue, £30m EBITDA and £20m of SaaS annual recurring revenue by 2030.

While those targets remain several years away, recent trading updates suggest the business is moving in the right direction.

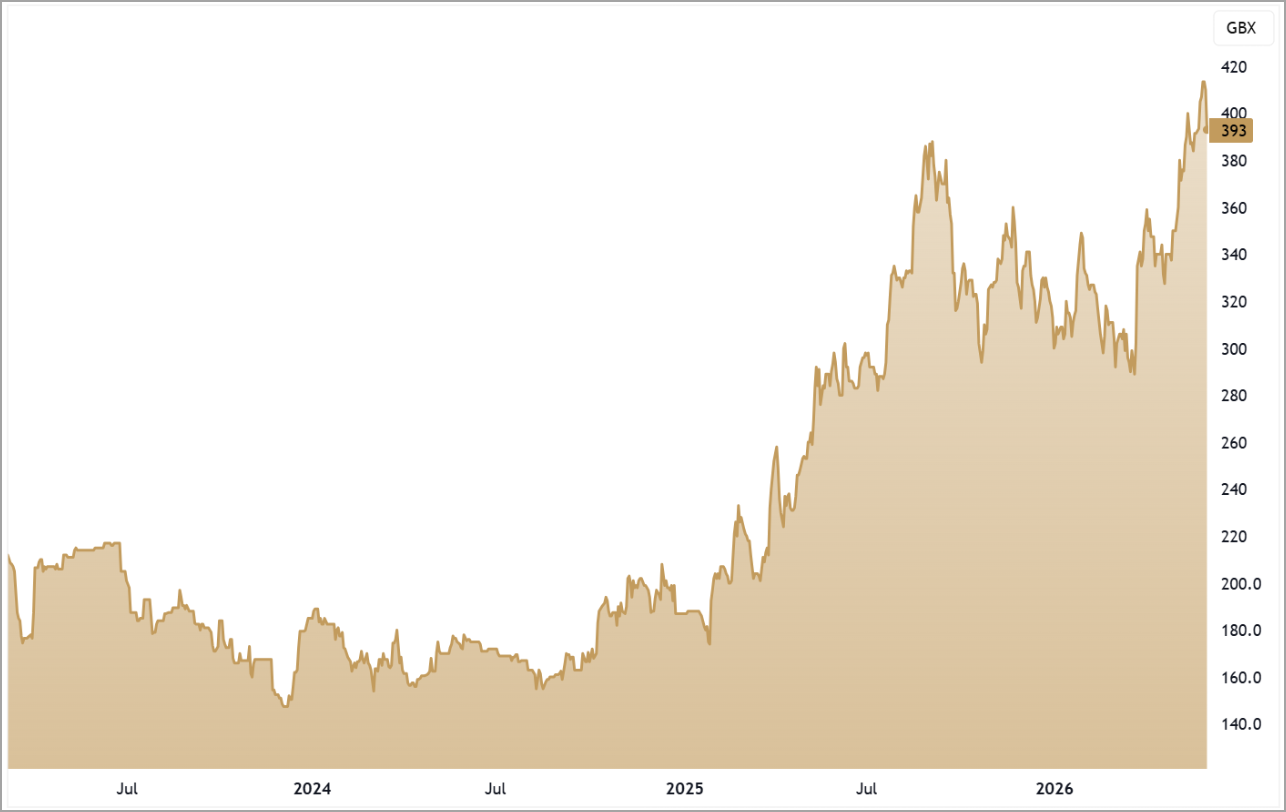

The Trend Continues

One of the reasons we favour adding a second tranche at this stage is that the chart is confirming the improving fundamentals.

Following a lengthy consolidation phase throughout much of 2025, the shares have established a clear series of higher highs and higher lows. The stock recently broke out to fresh multi-year highs before experiencing a modest pullback.

Importantly, that pullback has so far done little damage to the broader trend. The shares remain comfortably above both the rising 50-day and 200-day moving averages, while relative strength continues to outperform much of the AIM market.

The recent pause appears more consistent with profit taking after a strong advance than a meaningful deterioration in the underlying trend. In many ways, this is exactly the type of price action we would expect to see from a successful second tranche candidate.

At around 15 times forward earnings, Personal Group is no longer the bargain it once was. However, quality businesses rarely stay cheap forever. With recurring revenues, strong cash generation, growing partnerships and a supportive technical backdrop, we believe the company remains well positioned to continue delivering attractive shareholder returns over the years ahead.

Five Key Takeaways

1. Recurring Revenues: More than 90% of revenue comes from recurring insurance premiums and SaaS subscriptions, providing strong earnings visibility.

2. Partnership Growth: New agreements with Simplyhealth, Sante and Sage are expanding distribution and opening access to thousands of additional employers.

3. Strong Finances: Revenue increased 11% to £48.3m in 2025, while adjusted EBITDA rose 22% to £13.2m, ahead of expectations.

4. Cash Rich: Net cash climbed to £24.6m, supporting investment, acquisitions and a dividend yield above 6%.

5. Trend Confirmed: The shares recently reached fresh multi-year highs and continue to trade above rising 50-day and 200-day moving averages.

PGH 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.