4th Dec 2025. 9.10am

Regency View:

BUY Michelmersh Brick (MBH)

Regency View:

BUY Michelmersh Brick (MBH)

Laying the foundations for a re-rating

The brick market has not exactly been the most exciting corner of the stock market this year. Construction has slowed, sentiment has wobbled and investors have looked anywhere but small cap UK building materials. Yet, in the background, Michelmersh Brick (MBH) has been strengthening its foundations and the market has not taken notice.

Shares are down nearly 30% over twelve months, but the business keeps generating profits, growing its order book and paying shareholders a healthy 5.6% dividend. The price has crumbled, but the fundamentals have not. And for long term investors, that is usually where opportunity begins.

Building better

Michelmersh Brick is not just another commodity brick maker. They specialise in premium clay bricks and prefabricated brick components used in upmarket residential builds, commercial developments and heritage projects. Think higher margin architect led design rather than sheer volume output. When quality matters, Michelmersh products are the ones chosen.

The company operates through well established brands such as Blockleys, Carlton and Freshfield Lane, each with its own heritage and loyal customer base. These brands sit in a sweet spot of the market where customers are more concerned about aesthetics and longevity than they are about shaving a few pennies off each brick. That gives Michelmersh a natural defensive advantage during downturns.

It is also worth mentioning sustainability. Clay bricks are expected to remain a preferred building material for decades due to their strength, thermal performance and recyclability. Michelmersh has been investing in energy efficiency and lower carbon production methods which makes its product range increasingly attractive to developers focused on environmental standards and long term building performance.

This is a fully United Kingdom based manufacturing story. Production facilities across multiple regions support efficient logistics and short lead times. The company has also built a reputation for strong customer service and collaborative pricing which has helped preserve forward demand despite the wider slowdown in the sector.

Growth plans grounded in solid strategy

The last year has not been easy for anyone in construction. Yet Michelmersh has pulled the right levers to stay in a strong position.

The company invested heavily in the first half to modernise facilities and improve productivity. Those upgrades are now complete which should help restore margin progress into 2026 as volumes improve. When demand picks up, Michelmersh should see operating leverage flow quickly to the bottom line without needing to increase capital spending.

Forward order intake remains positive and underpins a well balanced pipeline. Some projects have been delayed due to caution around economic announcements and planning uncertainty, but the demand for premium brick has not disappeared. Michelmersh has been able to protect customer relationships and pricing which sets it up well for when confidence improves.

Shareholder returns remain a priority even through the cycle. A £2m buyback programme is expected to complete by year end and dividends continue to rise slowly but steadily. Management have shown that they are committed to balancing reinvestment with cash returns which is exactly what investors want from a well run industrial business.

When a company invests into weakness it is usually positioning itself for stronger returns when the cycle turns.

Income while you wait

The valuation case here is very clear. The shares trade on a forward price to earnings multiple of 9.4 times which looks remarkably modest for a profitable business with low financial leverage and a clear plan for growth. The PEG ratio of 0.6 highlights that the share price is failing to reflect market expectations for an earnings rebound next year which sits above 20%.

Enterprise value to EBITDA is 6.9 times which again shows the disconnect between the current share price and underlying cash generation. The price to book ratio of 0.84 suggests the market is even valuing the company at a discount to its tangible asset base which includes valuable land and manufacturing infrastructure that would be costly to recreate.

Revenues are expected to finish the year around £69m with adjusted EBITDA of £12.5m. Despite challenging sector conditions profits remain consistent and the balance sheet is set to be broadly cash neutral with net gearing barely above 1%. Michelmersh has options and flexibility which many peers lack.

Dividends are well covered and have grown steadily over the years. Investors are effectively being paid meaningful income while they wait for the cycle to recover. And if analysts are correct with their target price of 134.5p which would deliver more than 50% upside then shareholders stand to benefit from both yield and capital growth.

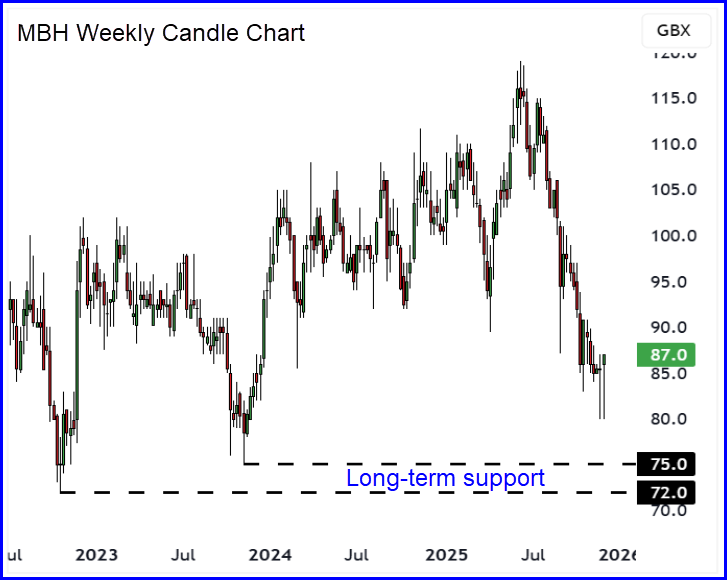

Approaching key support levels

Michelmersh is ticking all the boxes for an unloved stock. Momentum is weak and trading volumes are light. That is typical late cycle behaviour and often a sign of widespread investor apathy. It is also often what the bottom of a chart looks like.

After trading sideways for much of the last two years the share price is now approaching the major cluster of lows formed in 2022 and 2023. This long term support area has held firm multiple times. Buyers have historically defended these levels and early signs suggest that selling pressure may be drying up again.

Price action has shifted from a slow grind lower to a more stable base forming pattern. There is no panic selling and investor behaviour feels more like quiet accumulation than capitulation. If the shares can climb back above the 200 day moving average it would be the first clear indication that the recovery phase is underway.

This is not a fireworks chart but it does resemble the early stages of a turnaround where valuation and patience tend to win.

A quality business on sale

Michelmersh Brick makes a product Britain will continue to need for decades to come. It generates cash, owns real assets and consistently rewards shareholders. It has used this slowdown to invest intelligently and strengthen its market position rather than retreat.

Right now the shares are priced as if the downturn will drag on forever. But downturns end. Projects restart. Confidence returns. And when that happens the companies that kept investing tend to emerge with greater share and improved pricing power.

Michelmersh Brick looks like one of those stories that will feel obvious with hindsight. It is a quality business currently trading at a sale price with the prospect of rising earnings, improved margins and a solid dividend to enjoy in the meantime.

Five Key Takeaways

1. Premium positioning: Michelmersh focuses on higher quality clay bricks and components where demand remains resilient and pricing power is stronger.

2. Attractive valuation: The shares trade on modest value multiples that fail to reflect forecast earnings growth and underlying asset worth.

3. Strong financial footing: Low gearing, stable profitability and a cash neutral balance sheet provide confidence through the cycle.

4. Income while you wait: A growing dividend and active buyback programme support shareholder returns even in a slower market.

5. Well placed for recovery: With investment complete and key support levels holding, even a small uptick in construction activity could drive a meaningful re rate.

MBH 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.