5th Jun 2025. 9.05am

Regency View:

BUY Kitwave (KITW) Second Tranche

Regency View:

BUY Kitwave (KITW) Second Tranche

Kitwave: A breakout, a beat, and a buying window

Some stocks go sideways forever. Others sleep, then leap. Kitwave (KITW) has just done the latter.

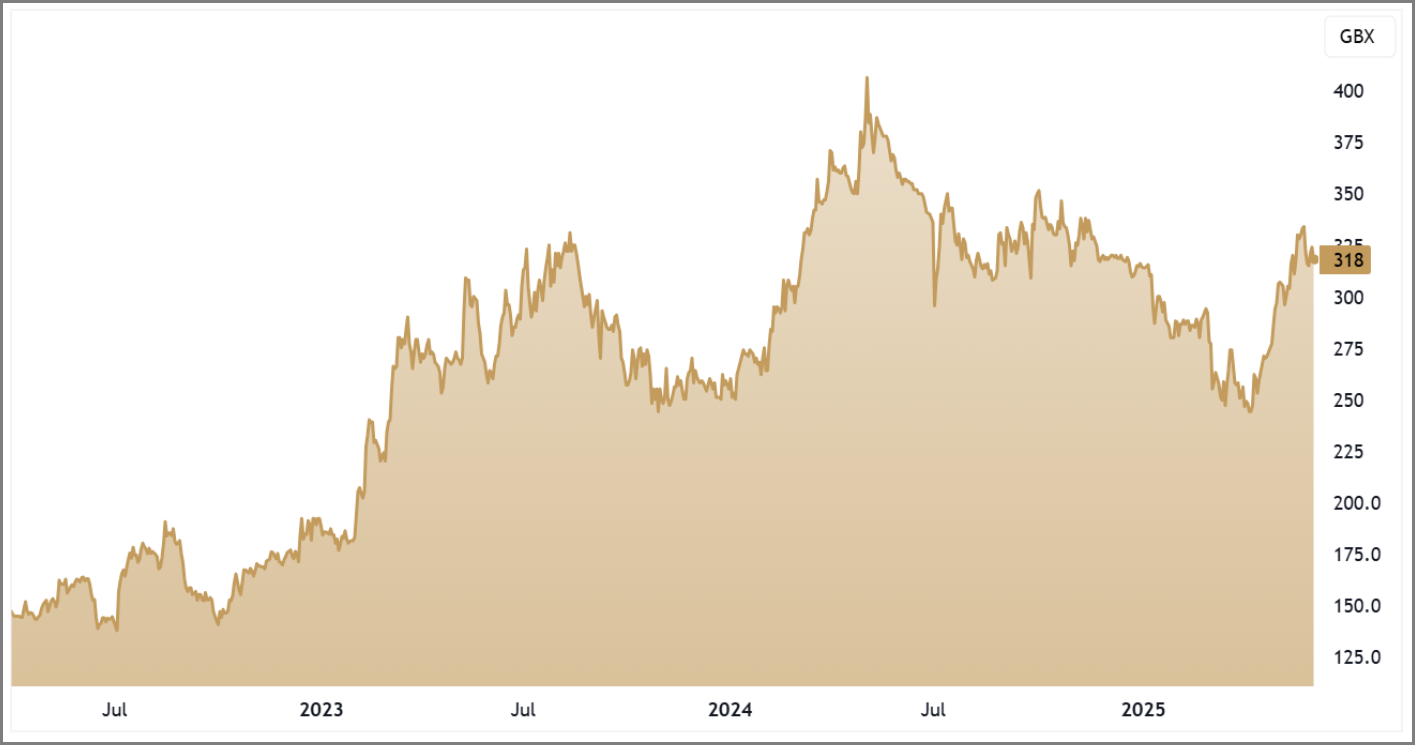

Since we first flagged the shares in April, the price has rallied over 20%, breaking decisively above a long-held descending trendline that had capped upside since early 2023. This isn’t just technical noise it’s confirmation that the market is re-rating the stock on the back of solid delivery and a structural growth story.

With a well-covered 3.8% dividend, forecast double-digit earnings growth, and plenty of headroom for multiple expansion, we’re initiating a second tranche buy.

Let’s unpack why.

Holding firm in choppy waters

On 7th May, Kitwave released a pre-close trading update for the six months to 30 April. The headline was reassuring: trading was in line with expectations, despite some early softness in hospitality demand. That hit the Foodservice division in January and February but recovered as the Easter season approached. The Retail & Wholesale division held steady with positive like-for-like sales.

For a consumer-facing business to maintain trajectory in a cost-pressured, patchy economic environment is no small feat. While many peers are still adjusting to post-Covid normality, Kitwave has moved into the next phase: network optimisation, operating leverage, and synergistic integration.

Creed is now a national platform

The integration of Creed Foodservice, acquired in late 2023, is now bearing fruit. Kitwave is already seeing operational benefits from its extended national reach, particularly in logistics. That’s crucial because distribution efficiency is the lifeblood of wholesale. There’s still more to come: the Board expects tangible synergy benefits to kick in during H2, with deeper systems harmonisation set for 2026.

Creed was a smart buy. Not only does it strengthen the Group’s scale, but it also brings in a high-quality brand that enhances Kitwave’s positioning in the foodservice market. That matters as the business shifts towards higher-margin, less commoditised operations.

New infrastructure, smart investment

One feature that often separates good operators from great ones is how they handle operational change. Kitwave opened a new foodservice distribution centre in the South West during the period and chose to front-load investment to protect customer experience. That meant higher near-term costs, but it’s the kind of short-term pain that sets up long-term gain. The rest of the cost base was kept in line, with depreciation rising as expected from recent fleet upgrades.

Importantly, management isn’t just spending it’s streamlining. With National Insurance and other structural headwinds, Kitwave is actively targeting operational efficiencies to maintain margins. This is a team that runs a tight ship.

Financials: Quality at a discount

Let’s talk numbers. Kitwave’s forward P/E is just 9.7x with forecast EPS growth of 15.3%. That gives a PEG ratio of 0.7, squarely in GARP (growth at a reasonable price) territory. The shares yield 3.8%, comfortably covered by earnings and backed by strong cash generation free cash flow is running at a multiple of just 11.2x. That’s the kind of profile that ticks both income and growth boxes.

The EV/EBITDA multiple stands at 9.4x, reflecting the Group’s scalable model and recent investment phase. Operating margins of 4.3% might seem modest, but in wholesale, scale and efficiency matter more than headline margins. Return on capital is healthy at 13.2%, and ROE is an impressive 16%, underlining the business’s ability to generate attractive returns without overextending.

From a value perspective, the price-to-sales ratio is just 0.41x. That’s low for a business with sticky customer relationships and a growing foodservice footprint. Price to book sits at 2.18x – hardly stretched given the strong returns.

Momentum is building

This isn’t just a value story. After lagging the market for much of 2023, Kitwave has finally caught a bid. The shares are up more than 23% over the past three months and have decisively broken above both the 50- and 200-day moving averages. Price action is now above the long-term descending trendline, which had acted as resistance for more than a year.

The breakout is real and supported by volume, even as short-term participation remains modest. In short, the chart has gone from frustrating to exciting (yes, charts can be exciting if you’re that way inclined). We’re now watching for a potential flag or consolidation pattern above 310p, with scope to retest 52-week highs around 365p.

The one-year relative performance still shows a 14.5% decline, which tells you there’s room for catch-up. With investor attention returning and institutional appetite growing, we’re entering a fresh leg of the trend.

Why a second tranche now?

The market cap remains modest at £271m, and the group is still under the radar for most institutions. That gives retail investors a continued edge. With the shares trading at a forward P/E below 10x, yielding close to 4%, and the company on track to meet full-year expectations, this is an asymmetric setup.

Creed integration, new infrastructure, and a bounce-back in Foodservice all point to stronger H2 delivery. Seasonality also favours the second half, historically the stronger part of the year. With synergies just starting to land, we expect margin expansion and EPS upgrades to follow.

In short: the breakout has happened. The valuation still hasn’t caught up. That’s the ideal moment for a second tranche buy.

KITW 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.