13th Mar 2025. 9.00am

Regency View:

BUY Johnson Service Group (JSG)

Regency View:

BUY Johnson Service Group (JSG)

JSG: A recovery story with momentum and value

Johnson Service Group (JSG) has come through a period of retracement, but the business itself has never been in better shape. With a resilient model, strong financials, and a share price bouncing from a key level, it’s a stock that’s starting to look interesting again.

The latest full-year results confirm that growth is still firmly on track, and with valuation metrics pointing to a “growth at a reasonable price” opportunity, the setup is hard to ignore. When price action and fundamentals align, it’s usually worth paying attention.

What does JSG do?

JSG is a leader in the textile rental and laundry services market, providing businesses with everything from fresh linen to industrial workwear. It serves industries like hospitality, healthcare, and manufacturing, handling the collection, cleaning, and delivery of textiles so clients don’t have to. It’s the kind of service most people don’t think about—until they need it—but for the businesses that rely on it, it’s essential.

The company operates on a contract-based, repeat business model, which gives it a level of revenue visibility that many consumer cyclicals lack. When a hotel, restaurant, or factory signs up for JSG’s services, they aren’t just making a one-off purchase; they’re committing to an ongoing partnership. This creates a steady stream of income, with new client wins and price increases driving organic growth.

Sustainability is also a natural advantage. Renting and reusing textiles is inherently more efficient than buying and disposing of them, and JSG has continued investing in energy and water-saving initiatives. This isn’t just good for the environment—it helps keep costs down and strengthens relationships with large corporate clients looking to improve their own sustainability credentials.

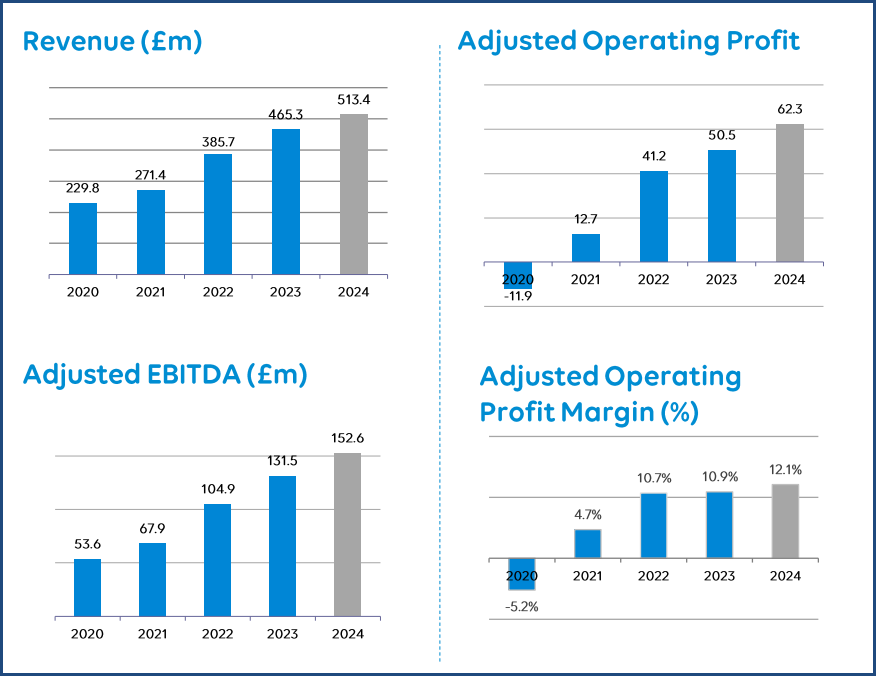

The numbers: A strong year for growth

JSG’s full-year results confirm that the business is still growing, still profitable, and still generating plenty of cash. Revenue came in at £513.4m, reflecting strong demand across its core sectors. Adjusted operating profit reached £62.3m, while adjusted EBITDA came in at £152.6m, reinforcing just how much cash the business is generating.

Margins are holding up well, too. The adjusted operating margin landed at 12.1%, a solid figure that highlights the company’s pricing power and operational efficiency. This ability to maintain strong profitability, even in a competitive sector, is what makes JSG a compelling long-term hold.

I’ve included an image here with four charts—revenue, adjusted profit, adjusted EBITDA, and operating margin. On the surface, it’s just an image of some financial graphs, but for analysts, the key takeaway is that the trajectory of those key metrics are pointing firmly in the right direction.

A platform for sustainable growth

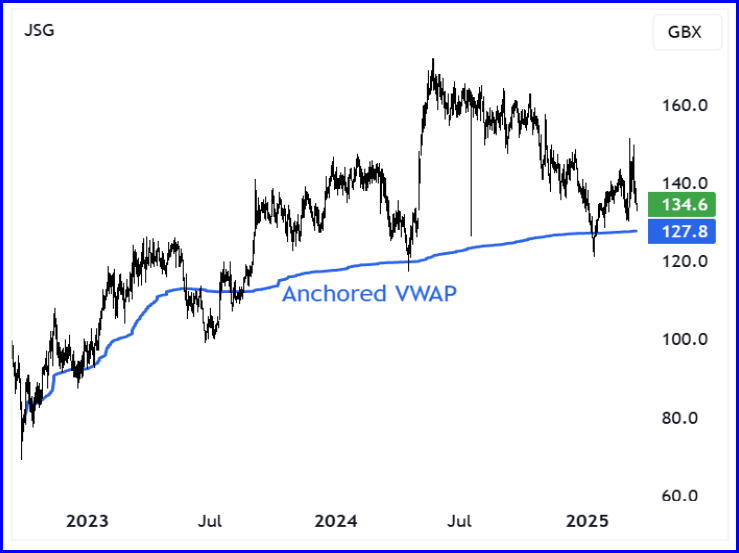

Technicals: A bounce from a key level

JSG’s share price has been recovering since mid-2022, carving out a broad series of higher swing lows. After rallying to fresh trend highs in mid-2024, the stock has spent most of the last year in retracement mode, consolidating gains rather than giving them up entirely.

Now, prices have reached an interesting area. Anchoring a VWAP (volume-weighted average price) to the 2022 lows—effectively measuring the true average price of those who bought at the bottom—shows a level where the stock has repeatedly found support. In recent weeks, JSG has bounced from this zone again, and this time, it has done so alongside the release of full-year results.

The timing matters. A stock bouncing from a key level is one thing, but when that bounce coincides with a strong set of financials, it suggests renewed confidence from investors. If this level continues to hold, it could provide the springboard for the next leg higher.

Valuation: Growth at a reasonable price

JSG trades at a forward P/E of 11x, which isn’t particularly cheap or expensive relative to the sector. But what makes it stand out is its PEG ratio of 0.4. The PEG ratio (Price/Earnings to Growth) compares a stock’s valuation to its expected earnings growth, and in JSG’s case, with forecasted EPS growth of 33.5%, that figure suggests the stock is undervalued relative to its growth potential.

Beyond earnings, JSG also offers a 3.62% dividend yield, providing a solid income stream for investors. On top of that, the company has a share buyback scheme, which adds further support to the stock price by reducing the number of outstanding shares.

With manageable debt levels and a business model that generates consistent cash flow, JSG strikes a healthy balance between growth and quality. The combination of steady profitability, improving momentum, and a reasonable valuation makes this a stock worth watching.

JSG 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.