7th May 2026. 9.03am

Regency View:

BUY James Cropper (CRPR)

Regency View:

BUY James Cropper (CRPR)

Turning Progress Into Profit

Turnaround stories on AIM can be dangerous things. The market often gets excited far too early, bids the shares higher on optimism, then loses patience when operational improvements fail to feed through into the numbers. James Cropper now looks like it may finally be moving beyond that stage.

The latest trading update was important because for the first time in a while, the progress inside the business is starting to show up clearly in profitability, cash generation and debt reduction. After a strong initial reaction, the shares have since pulled back sharply, giving investors another chance to look at a recovery story that appears to be gaining traction beneath the surface.

A business rebuilding from the inside

James Cropper operates across advanced materials and specialist paper and packaging, supplying products into markets ranging from luxury packaging through to hydrogen technology, aerospace and recycling solutions. While the business still carries the heritage of a traditional industrial manufacturer, the growth engine increasingly sits inside the higher value advanced materials division.

That shift matters. Advanced Materials delivered low double-digit revenue growth in the latest year, while management also reported high single-digit EBITDA growth despite continued investment into operations and capacity. The division gives James Cropper exposure to structural themes such as lightweight composites, fuel cells and sustainable materials, helping move the business away from being viewed purely as a paper manufacturer.

At the same time, the weaker Paper & Packaging division is beginning to stabilise. Following a difficult period that included the loss of a significant merchant customer, the business delivered an EBITDA profit during the second half of the year. That may sound like a small detail, but in turnaround situations the first signs of stabilisation are often where sentiment starts to shift.

The numbers are finally improving

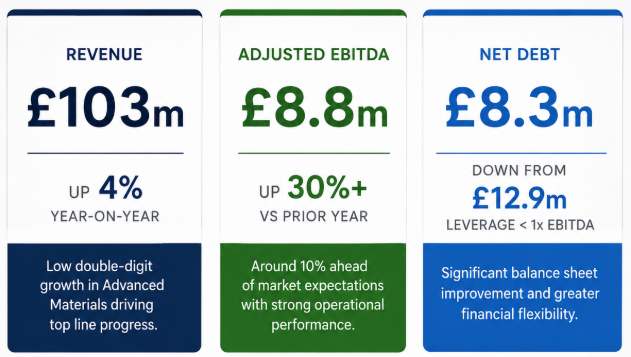

The latest full year trading update showed a business beginning to regain control operationally. Group revenue increased 4% to £103m, while adjusted EBITDA is expected to come in at £8.8m, around 10% ahead of market expectations and more than 30% above the prior year.

Perhaps more importantly, the balance sheet improved materially. Net debt reduced from £12.9m to £8.3m, leaving leverage below 1x EBITDA. For a micro-cap industrial business, that is a meaningful improvement in financial flexibility and removes some of the pressure that had been weighing on sentiment over the past two years.

FY26 Trading Update Financial Highlights

Cash generation also continues to stand out. Despite the operational challenges of recent years, the group has still been producing healthy free cash flow, with the shares currently trading on a price to free cash flow multiple of around 5.7. Meanwhile, the forward P/E ratio sits near 7.3.

Those valuation metrics still look more consistent with a struggling cyclical business than a company showing improving profitability, strengthening cash generation and stabilising operations. That disconnect is what makes the setup interesting.

A recovery story the market still does not fully trust

One of the more interesting aspects of the James Cropper story is that despite the improving operational backdrop, the market still appears somewhat sceptical about the durability of the recovery.

That hesitation is understandable. Trailing operating margins remain weak, return on capital is still negative on a historical basis and the company is operating in markets that remain sensitive to industrial demand and input costs. Management itself acknowledged the uncertain geopolitical backdrop and the risk around raw material and energy pricing.

But this is often how recoveries begin. The market rarely waits for perfect numbers before rerating a stock, it starts responding when direction of travel improves. In James Cropper’s case, the direction now appears materially better than it did 12 months ago.

The fact the company is delivering these improvements while still investing into Advanced Materials also adds weight to the longer-term opportunity. Management is not simply cutting costs to manufacture short-term profits. They are trying to reshape the quality of the business while stabilising the weaker areas at the same time.

The chart is starting to get interesting again

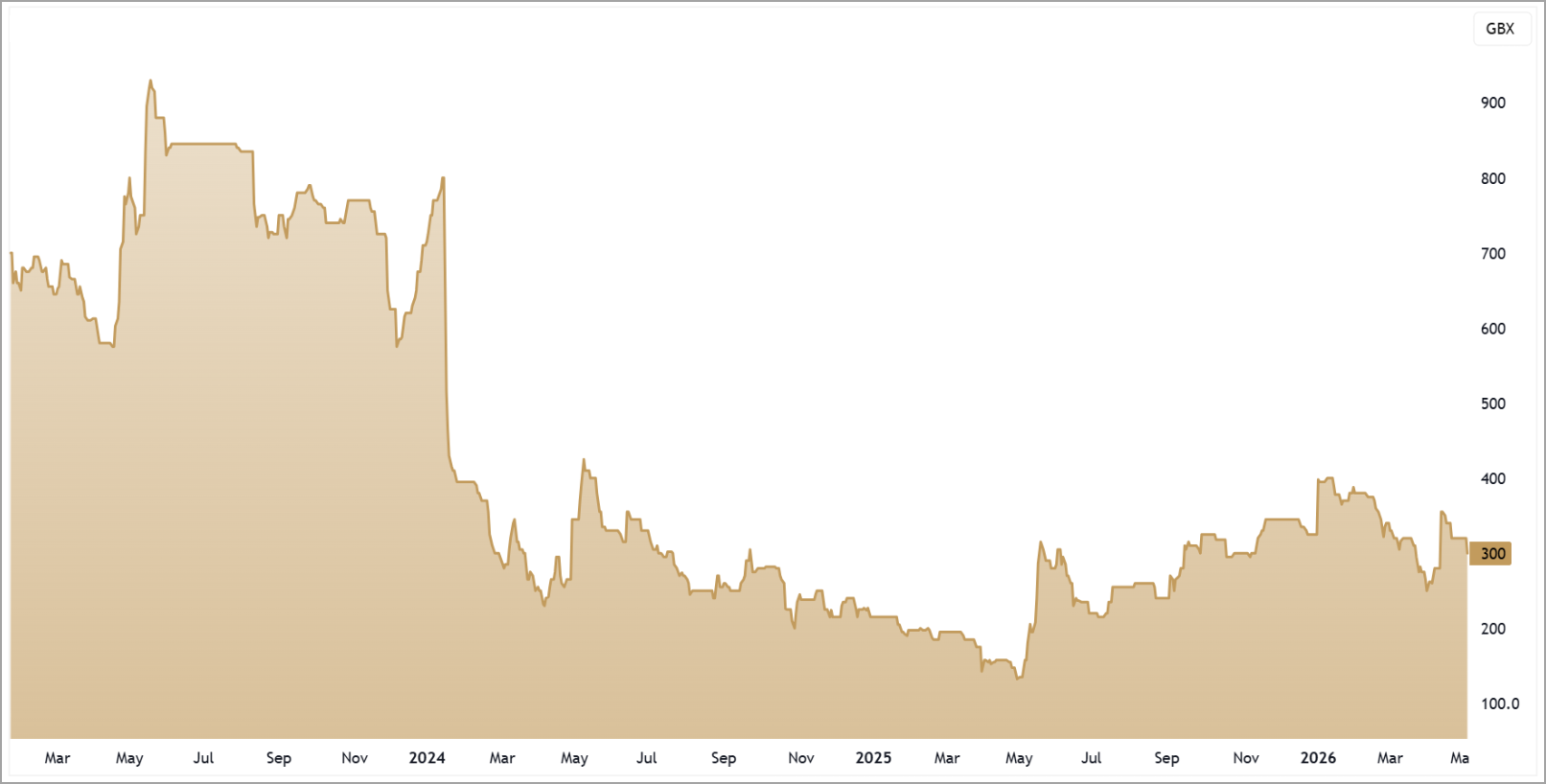

From a technical perspective, the shares have undergone a sharp reset over recent months. After trading above 400p earlier in the year, the stock sold off aggressively into April before finding support around the 250p region.

The latest trading update then triggered a strong gap higher as investors reacted positively to the improving numbers and strengthening balance sheet. Since then, however, the shares have retraced much of that move and are now trading back near the rising 200 day moving average.

That pullback may actually improve the setup.

Rather than continuing vertically higher after the update, the market has spent several weeks digesting the move and retracing back towards prior support levels around the 280p area. Importantly, the shares have so far avoided a complete collapse back through the gap, suggesting the market is beginning to accept a higher valuation range than before the update.

The broader structure also remains constructive. Despite the volatility, the stock is still trading well above the major April lows, while the 200 day moving average continues to trend gradually higher underneath price. If buyers begin stepping back in around current levels, the recent weakness may ultimately prove to be more of a reset within a developing recovery trend rather than the start of a fresh breakdown.

Five Key Takeaways

1. Operational Progress: EBITDA is expected to come in more than 30% ahead of the prior year and above market expectations.

2. Debt Reduction: Net debt has fallen sharply to £8.3m, with leverage now below 1x EBITDA.

3. Advanced Materials: Higher value growth areas continue to expand despite wider industrial uncertainty.

4. Valuation Reset: The shares trade on a forward P/E near 7 despite improving profitability and cash generation.

5. Technical Structure: Following a deep pullback, the shares are attempting to stabilise around key support and the rising 200 day moving average.

CRPR 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.