20th Nov 2025. 9.08am

Regency View:

BUY Ingenta (ING)

Regency View:

BUY Ingenta (ING)

Ingenta: A mispriced micro cap

It has been a long time since we have featured a company of this size in AIM Investor, but Ingenta (ING) earns its place for all the right reasons…

Ingenta is an example of a small business with real depth behind it. The share price does not reflect the quality of the underlying company, and that creates an opportunity worth acting on.

At first glance, Ingenta looks unexciting. It serves the global publishing industry with software and services that manage intellectual property, rights, royalties and digital content. There is nothing fashionable about it. But there is a great deal to like once you step past the surface.

The business is financially strong, consistently profitable and run with a level of discipline that stands out among companies twenty times its size. It is small in market cap terms but far from small in terms of financial maturity.

Quality that the market has overlooked

The attraction here lies in the contrast between the company’s financial strength and the valuation the market applies to it. Ingenta consistently delivers returns on capital close to 35% and returns on equity near 29%. Operating margins sit above 23% and free cash flow generation is steady. The company carries no debt at all and holds close to four million pounds in cash.

Despite these characteristics, the shares trade on a price to earnings multiple of about seven and an enterprise value to EBITDA of roughly three. Free cash flow is valued at around six times earnings and the dividend yield sits close to 5% with solid cover. These are the kind of metrics usually associated with businesses facing material headwinds, yet Ingenta is anything but distressed.

Part of the reason for this valuation gap is that revenue has been stable rather than fast growing. Many investors instinctively screen out companies with flat top lines. Yet the more important story lies in profitability rather than revenue. Ingenta has modernised its delivery model, strengthened its cloud infrastructure and increased the share of recurring managed services. Costs have been controlled and margins have expanded steadily, which means earnings have grown even in the absence of strong top line growth.

Interim results point to further progress

The interim results published in September demonstrate the company’s operational strength. Revenue increased to 5.2 million pounds compared with 5.1 million pounds in the previous period. Recurring income rose to 88% of total revenue. Gross margins improved from 48% to 51% and adjusted EBITDA increased to 0.9 million pounds, which represents a 29% rise. Cash generated from operations climbed 75% to 0.7 million pounds and overall cash reached 3.9 million pounds.

Adjusted earnings per share rose 38% to 5.86p. The interim dividend was increased 17% to 1.75p. Commercial revenue grew 9% as customers expanded their use of managed services. The decline in Content revenue was expected due to older client contracts rolling off. The company has now completed the expansion of its sales and marketing teams, which should support a more active pipeline in the second half of the year and into 2026.

These results do not reflect rapid transformation, but they do reflect careful execution and financial control. Ingenta continues to do the simple things well and that creates a reliable foundation for future growth.

A balance sheet built for resilience

One of Ingenta’s most appealing features is the strength of its balance sheet. The company has no borrowings and no lease liabilities, yet it holds almost four million pounds of cash. Cash represents more than 40% of total assets. Trade receivables have declined as payment cycles improved and legacy provisions have now been resolved. The deferred tax asset remains valuable as the company continues to expand its sales resources.

This level of financial strength is rare among micro caps. It reduces operational risk, eliminates refinancing concerns and gives the business time and flexibility to pursue opportunities. It also means Ingenta can continue to reward shareholders without compromising investment in future growth.

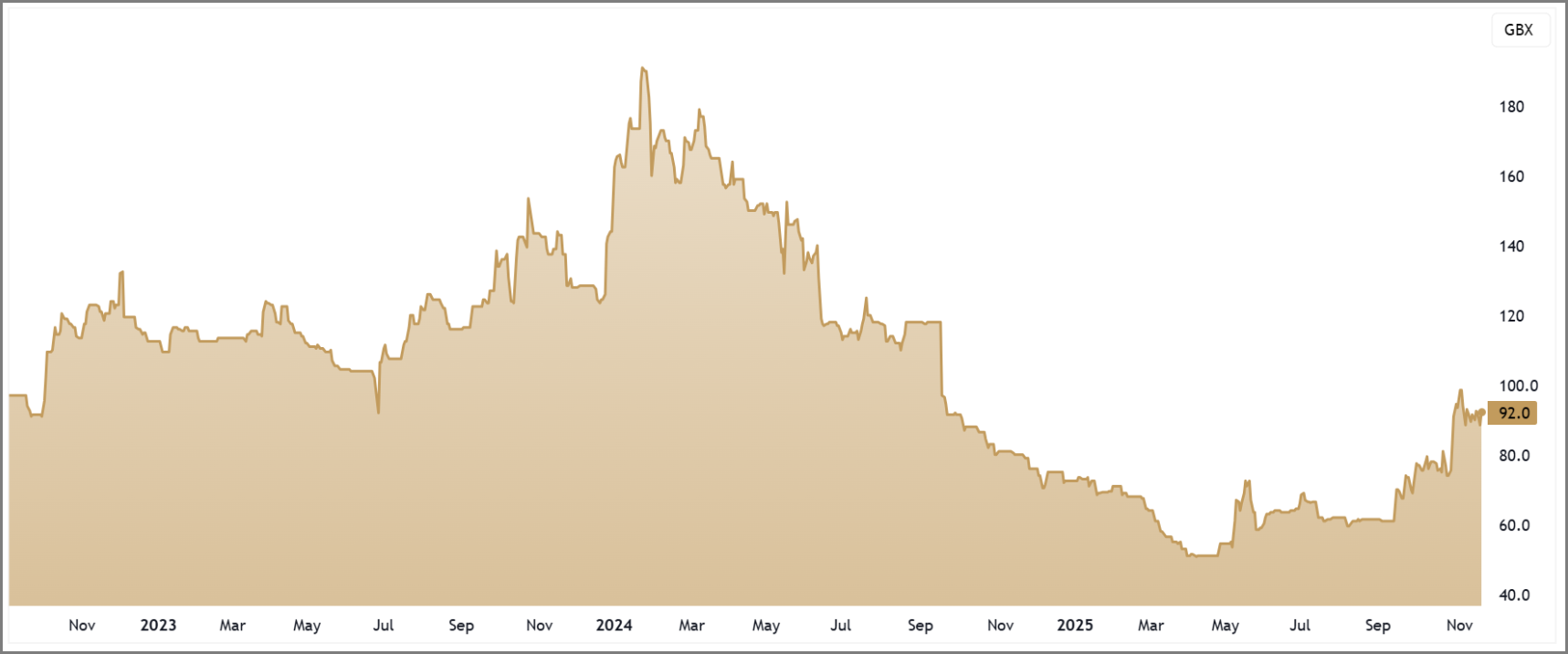

Technical picture showing a shift in sentiment

The behaviour of the share price in 2025 supports the view that sentiment is improving. After years of subdued trading, the shares finally broke higher in May following a strong trading update. The market paused during the summer before another decisive move in September after further positive news. These moves were sharp and driven by genuine demand rather than speculation.

The structure of the advance is encouraging. The shares have developed a clear pattern of higher swing lows and higher swing highs. The 50 day moving average now sits above the 200 day moving average and both are trending upward, which reflects a meaningful change in momentum. The recent consolidation following the early November high appears healthy. Prices remain comfortably above both moving averages and the uptrend remains intact.

Micro caps often move in short bursts as investors reassess the story. Ingenta’s chart behaviour suggests the early stages of a rerating as the market begins to recognise the quality behind the numbers.

Our view

Ingenta combines high returns, strong cash flow, a resilient balance sheet and an attractive valuation. The interim results reinforce the view that the company is executing well and the technical picture points to a market that is beginning to reassess the story. This is not a speculative play. It is a well run, consistently profitable business that has been undervalued for too long.

We are adding Ingenta to the AIM Investor list of open positions as a high quality mispriced micro cap with genuine rerating potential.

Five Key Takeaways

1. High quality: Strong margins, cash generation and returns far above typical micro cap levels.

2. Mispriced valuation: Shares trade at value multiples that do not reflect the underlying strength.

3. Robust balance sheet: No debt, significant cash and reliable liquidity provide real resilience.

4. Improving momentum: Price structure and moving averages confirm a clear shift in sentiment.

5. Early rerating: Market recognition has begun but the opportunity still looks underappreciated.

ING 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.