26th Feb 2026. 9.02am

Regency View:

BUY Ingenta (ING) Second Tranche

Regency View:

BUY Ingenta (ING) Second Tranche

Ingenta: From rerating to reinforcement

When we first added Ingenta (ING) to AIM Investor back in November, the case was built around a simple mismatch. A small, quietly profitable software business with strong returns, a clean balance sheet and dependable cash generation was being priced like something far more fragile. Since then, the shares have done what we hoped they would do. The market has started to take the business more seriously, and the valuation has begun to move in the right direction.

With the stock now up around 45% from our original entry, the easy decision would be to sit back and declare the job done. But investing rarely works in neat chapters. What matters more than the share price is whether the underlying story is still improving. January’s trading update suggests it is, which is why we are comfortable reinforcing the position with a second tranche rather than treating this as a closed book.

The original thesis is being validated

Nothing in the past few months has undermined the core reasons we bought Ingenta in the first place. The business remains profitable, cash generative and conservatively run. It still operates in an unglamorous but sticky niche, providing mission-critical software to the publishing and media industries. And it still converts a high proportion of revenue into cash, supported by a large base of recurring income.

What has changed is not the character of the business, but the confidence around it. The market is no longer treating Ingenta as a forgotten micro cap with flat revenues and no obvious catalyst. Instead, it is starting to recognise a small software company that is financially robust, operationally disciplined and capable of compounding value steadily rather than spectacularly.

That shift in perception is exactly what a rerating looks like in practice. It does not arrive with fireworks. It shows up through better price behaviour, improving liquidity and a growing willingness from investors to pay a more reasonable multiple for reliable earnings.

January’s update: Quiet progress, real substance

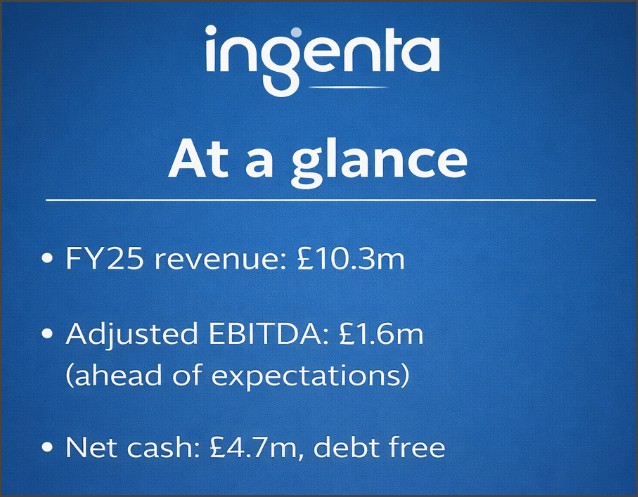

The January trading update did not try to dress anything up. Revenues for FY25 are expected to come in at £10.3m, broadly in line with the previous year. But adjusted EBITDA is set to beat market expectations at £1.6m, and the more important story is again sitting on the balance sheet and the cash flow line.

Ingenta generated £1m of cash during the year and finished December with £4.7m of cash and no debt. A year earlier, that figure was £3.6m. This is not a business living off accounting adjustments or one-off items. It is a business that is consistently generating cash, funding its own development and still increasing shareholder returns at the same time.

The proposed 10% increase in the full-year dividend to 4.5p underlines that point. This is not a token payout. It is a sign of confidence in the sustainability of earnings and cash flow, and it reinforces the idea that Ingenta has moved firmly into the category of small, dependable compounders rather than speculative turnarounds.

Execution before acceleration

Strategically, the past year has been about laying foundations rather than chasing headlines. Management has been investing in sales and marketing to build a broader and more durable pipeline for future growth. Progress on hiring has been slower than ideal, but the direction of travel is clear, and the update points to a growing number of sales opportunities and partnerships starting to gain traction.

In the meantime, the existing customer base continues to do the heavy lifting. Revenue growth in FY25 came largely from current clients, and another Edify customer has gone live, adding further depth to the recurring revenue base. This is exactly how these businesses scale in the real world. First you stabilise and optimise the core. Then you widen the funnel. Only after that does growth start to show up more clearly in the headline numbers.

For 2026, management has been careful not to overpromise. The high level of recurring revenue provides a solid floor under performance, while further profitability growth will depend on how quickly new customers are onboarded. That is a sensible, credible framework, and it fits with the steady, disciplined way this business has been run for years.

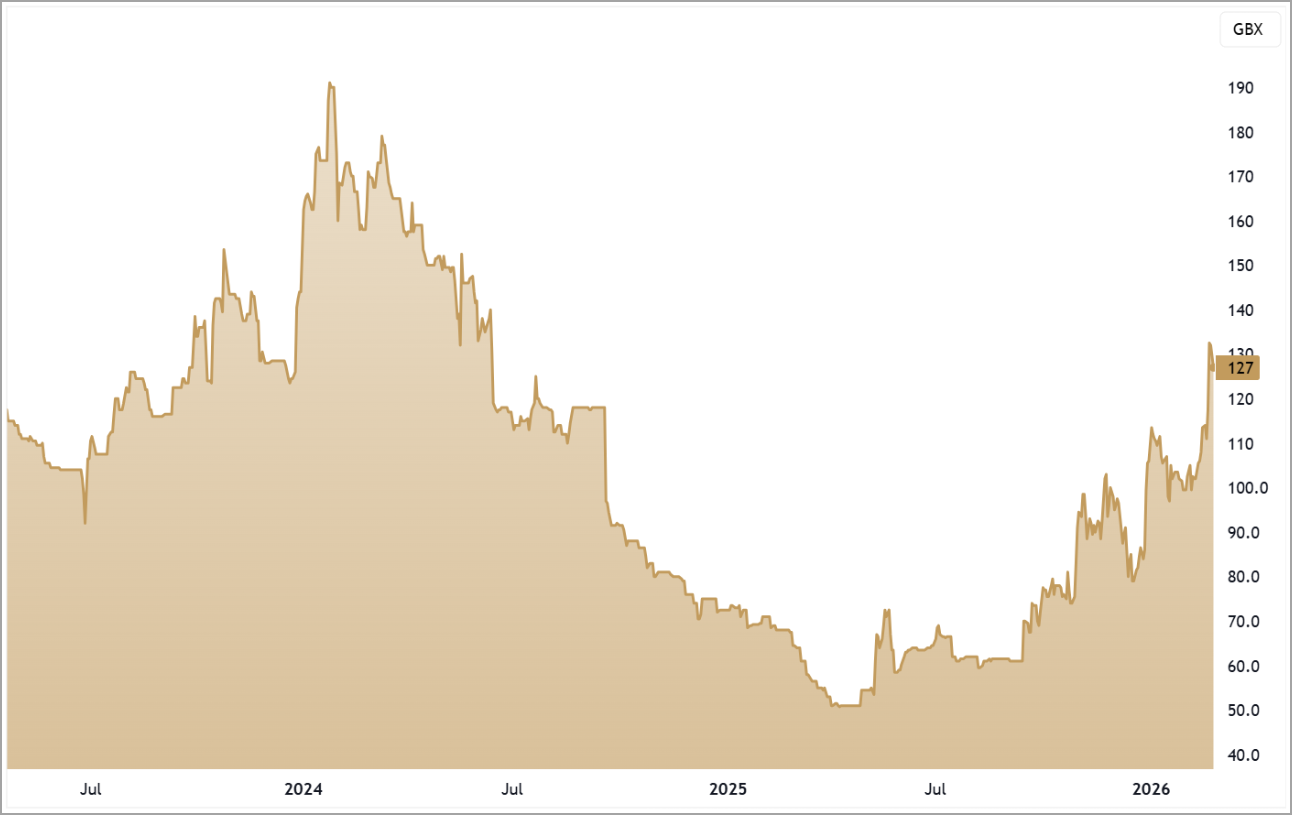

Chart shows momentum

The technical picture has continued to improve since our original write-up. After a long period of base-building, the shares are now in a clear, orderly uptrend. Prices are well supported by the longer-term moving averages, and the rally since the January update has been constructive rather than frantic.

This matters because it suggests the move is being driven by a gradual reassessment of the business rather than short-term speculation. In small caps, that distinction is important. Sustainable trends tend to come from improving fundamentals and rising confidence, not from one-off bursts of excitement.

In other words, the chart is now confirming what the financials have been signalling for some time: Ingenta is a stronger, more resilient business than it was a few years ago, and the market is slowly adjusting its view accordingly.

Why add, rather than just hold?

Adding to a position after a strong run always feels harder than making the first buy. Psychologically, it is more comfortable to anchor to the original price. But good portfolio management is about anchoring to the quality and direction of the business, not to where you happened to buy it.

Since November, Ingenta’s risk profile has improved. The cash balance is higher. The dividend is higher. The business is still debt-free. Execution remains steady. And the market’s perception is moving in the right direction. That combination justifies a larger position size than it did when the story was still being rediscovered.

This is not about chasing momentum. It is about increasing exposure to a business that is doing what we expected it to do: generate cash, run conservatively, reward shareholders and gradually earn a better valuation. The shares are no longer “mispriced” in quite the same way they were, but they still look reasonable for a high-return, cash-generative software business with a growing dividend and improving commercial momentum.

Progress will not be linear, and growth will not suddenly become explosive. But that is not the point. Ingenta’s appeal lies in its ability to compound quietly, with downside risk cushioned by cash, recurring revenues and financial discipline. That is exactly the kind of profile where adding a second tranche makes sense as the story continues to de-risk and mature.

Five Key Takeaways

1. Thesis working: The original quality and mispricing case is playing out, with fundamentals and sentiment moving in the right direction.

2. Cash generative: Strong cash inflows and a growing cash balance underline the resilience of the business model.

3. Recurring base: A high level of repeat revenues provides stability, visibility and support for steady compounding.

4. Disciplined execution: Investment in sales and marketing is being funded from cash flow, not leverage or dilution.

5. Trend supportive: The share price remains in a clear uptrend, reinforcing the improving fundamental story.

ING 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.