17th Jul 2025. 9.05am

Regency View:

BUY HSS Hire (HSS)

Regency View:

BUY HSS Hire (HSS)

HSS Hire: A Turnaround Story with Strong Growth Potential

HSS Hire (HSS) is undergoing a transformation, shedding its past struggles and re-establishing itself as a powerhouse in the tool and equipment hire industry…

After a tough few years, the company is finally on the upswing, with its stock breaking out of long-standing lows and showing impressive momentum. With a focused strategy in place, HSS is leveraging its streamlined operations and a more efficient business model to capture growth in a recovering market.

For investors seeking a turnaround opportunity, HSS Hire presents an enticing proposition. Positioned at an attractive valuation and with solid growth prospects, this is a company ready to deliver strong returns as it capitalises on its newfound momentum.

Restructuring allows each division to focus on its core markets

HSS Hire is a leading player in the UK and Ireland’s tool and equipment hire market, providing a wide range of tools, machinery, and equipment to businesses and individuals alike. Whether it’s heavy-duty machinery for construction or smaller tools for everyday tasks, HSS serves a diverse range of industries. Its ability to meet varied customer needs, from large construction projects to everyday maintenance tasks, has cemented its reputation as a reliable, go-to provider.

However, the real story lies in the company’s recent restructuring. In a bold move, HSS separated its operations into two distinct business units: HSS ProService and HSS The Hire Service Company (THSC). This split allows each division to focus on its core markets, enabling greater efficiency and more tailored strategies. ProService is capitalising on its growing Self Serve marketplace, while THSC is strengthening its B2B customer base and building out its builders merchant model. By honing in on these areas, HSS is positioning itself to take full advantage of the opportunities in its industry.

This shift in business focus is not just about simplifying operations, it’s about creating a company that’s more adaptable, streamlined, and ready to capitalise on the demand for reliable equipment hire as the market recovers.

A path to greater opportunity

HSS Hire’s growth strategy is built around its ability to tap into expanding markets and improving operational efficiency. At the forefront of this strategy is the development of ProService, which continues to gain traction through its Self Serve platform. This platform allows customers to easily access and rent equipment, streamlining the process and driving acquisition in a more tech-savvy, customer-focused way. The platform is already proving to be a hit with a wide range of customers, further enhancing HSS’s market presence.

In parallel, THSC is also making moves to increase its footprint, particularly in the builders merchant space. This model focuses on building direct relationships with businesses, providing the tools and machinery needed for construction and other high-demand industries. By targeting these specific sectors, THSC is positioning itself for solid growth in a recovering market. Together, the two business units represent a more agile and dynamic HSS Hire, ready to move quickly and effectively in the market.

These strategic efforts show that HSS is not only transforming its internal operations but is also positioning itself to meet growing demand as the UK and Ireland’s construction and industrial sectors expand.

Turning numbers into growth

HSS Hire’s financial performance is starting to reflect the progress of its turnaround. Total revenue for the latest 12-month period reached £349.1 million, a modest 5% increase. However, gross margin dipped to 45.2% from 47.0%, due to a shift in the sales mix towards rehire business, which is less profitable than seasonal sales. Despite these pressures, HSS is projecting EBITDA of £48.5 million and EBITA of £10 million for the upcoming year, suggesting that the company is managing to stabilise its earnings as it works through its transformation.

Looking at HSS’s valuation, the company’s forward PE ratio of 10.9 is well below the broader market average, which suggests it could be undervalued, particularly given its growth potential. The price-to-book ratio of 0.37% indicates that the stock is trading below its intrinsic value, presenting an opportunity for investors looking to buy into a company that’s set to rebound. Additionally, the price-to-sales ratio of 0.19% further points to the market’s underappreciation of HSS’s long-term potential.

The company also offers an attractive dividend yield of 6.35%, though the dividend coverage ratio of 1.45x suggests caution. Investors should monitor the sustainability of dividends as the company continues its recovery. Nevertheless, HSS’s valuation, combined with its solid prospects, makes it an interesting opportunity for value investors looking for upside.

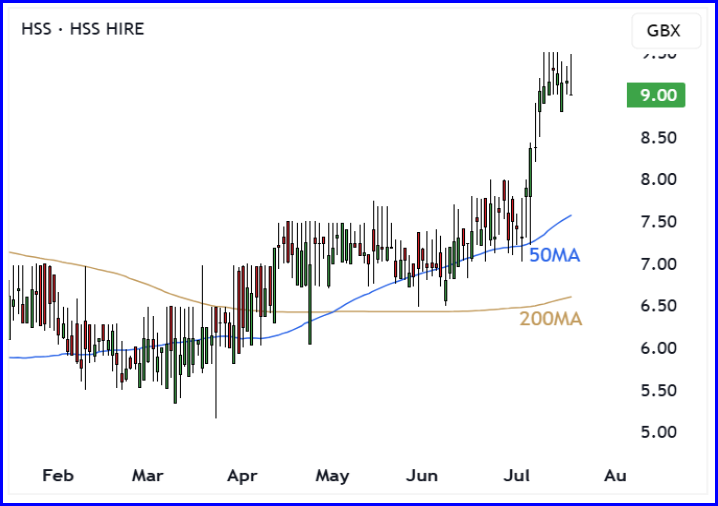

Technical analysis: A change in trend

HSS Hire’s technical outlook has dramatically improved in 2025. After several years of underperformance, the stock has moved above the key 200-day moving average, signalling a shift in trend. Even more compelling is the golden cross formed by the 50-day moving average crossing above the 200-day. This is a classic bullish signal that often precedes sustained upward momentum.

The golden cross indicates that the market is beginning to recognise the positive changes within the company. With the stock now consistently holding above key moving averages, the technical outlook is positive, suggesting that the upward trend could continue. However, investors should be cautious, as no trend is ever guaranteed. If the stock breaks below these key levels, it could indicate a reversal, but for now, the trend looks firmly in favour of the bulls.

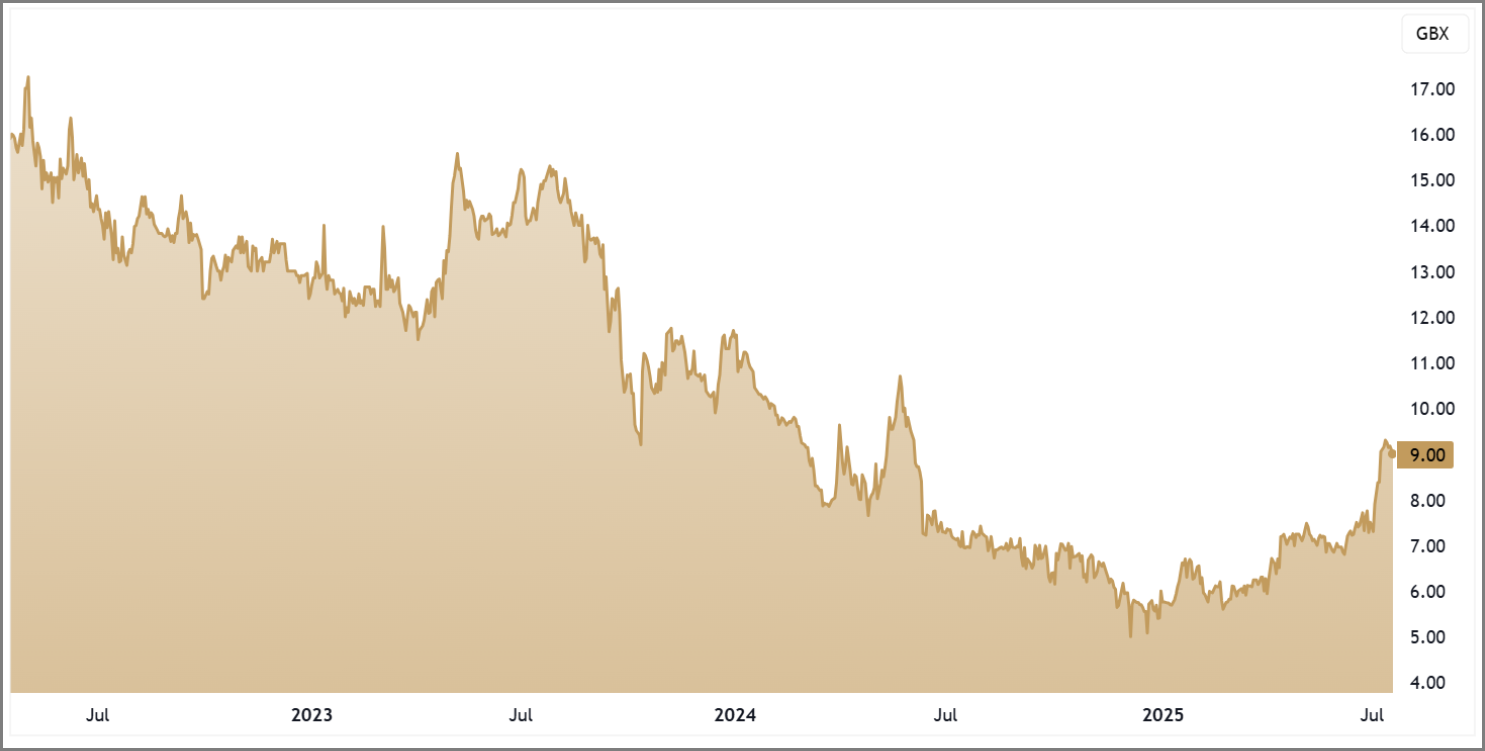

HSS 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.