16th Jan 2025. 8.56am

Regency View:

BUY Concurrent Technologies (CNC)

Regency View:

BUY Concurrent Technologies (CNC)

Concurrent Technologies: A small-cap with big momentum

Jim Slater famously said, “Elephants don’t gallop.” It’s a simple truth of investing: smaller companies often outperform because they’re nimble, agile, and focused on growth.

Concurrent Technologies (CNC) is a prime example. As a leader in high-performance computing, it has carved out a niche in mission-critical industries, delivering innovation and financial strength in equal measure.

With record-breaking growth, a rapidly expanding systems division, and major contract wins, Concurrent has cemented its position as a standout in the small-cap space. For retail investors seeking a company with momentum and market-leading potential, this is one to watch.

Inside Concurrent: Innovators in computing

Concurrent Technologies designs and manufactures high-performance computing hardware and systems for industries where reliability isn’t just important—it’s critical. Defence, aerospace, and telecommunications are just some of the sectors that rely on Concurrent’s cutting-edge solutions to operate in the toughest environments.

The company’s business model is built on two pillars: the Products division, which delivers advanced computing boards and components, and the Systems division, which provides fully integrated solutions tailored to customer needs. This dual approach lets Concurrent address both niche technical challenges and large-scale operational demands.

Sector Diversification

Products that perform

The Products division is the foundation of Concurrent Technologies’ business, delivering high-performance computing boards designed for reliability and precision. These boards are crucial for industries like defence and telecommunications, where failure isn’t an option. Products such as the Rhea VME processor board have solidified Concurrent’s position as a trusted supplier of mission-critical technology.

A key differentiator is the company’s ability to anticipate market trends and deliver solutions that meet evolving needs. The TR MDx/6sd-RCR PIC processor, for instance, offers compliance with the latest SOSA standards, ensuring compatibility with modern defence systems. Secure data storage and exceptional processing power are standard features, making Concurrent’s products indispensable for its clients.

Beyond their technical capabilities, these products contribute significantly to the company’s financial growth. With high margins and repeat orders from long-term clients, the Products division is a reliable revenue driver. By staying ahead of technological trends and maintaining strong relationships with customers, Concurrent ensures its product portfolio remains competitive and in demand.

Systems division: Driving expansion and growth

The Systems division is the heart of Concurrent’s growth story. The strategic acquisition of Phillips Aerospace has significantly bolstered its presence in the lucrative US market, opening doors to new opportunities.

Recent wins, including a £3m contract in the Asian defence sector, underline the division’s growing influence. With a state-of-the-art facility in Los Angeles set to open and key leadership hires already in place, the Systems division is well-positioned for sustained growth.

These contract wins are more than just numbers—they’re a testament to Concurrent’s ability to compete on a global scale. Each deal strengthens its credibility, enhances its pipeline, and secures a steady flow of future opportunities.

Breaking down the numbers

Concurrent’s financials tell a story of growth and resilience. In the first half of 2024, revenue surged 39% year-on-year to £16.8m, while profit before tax leapt 130% to £2.3m, up from £1m in the same period the previous year.

Order intake rose 23% to £17.8m, reflecting strong demand across sectors. The company’s growing backlog now exceeds £12m, providing clear visibility for future revenues. Meanwhile, its cash position tripled to £8.9m, compared to £2.9m a year earlier, reinforcing its ability to fund further expansion and innovation.

With a balance sheet that includes no long-term debt and strong free cash flow generation, Concurrent stands out as a small-cap with both stability and growth potential.

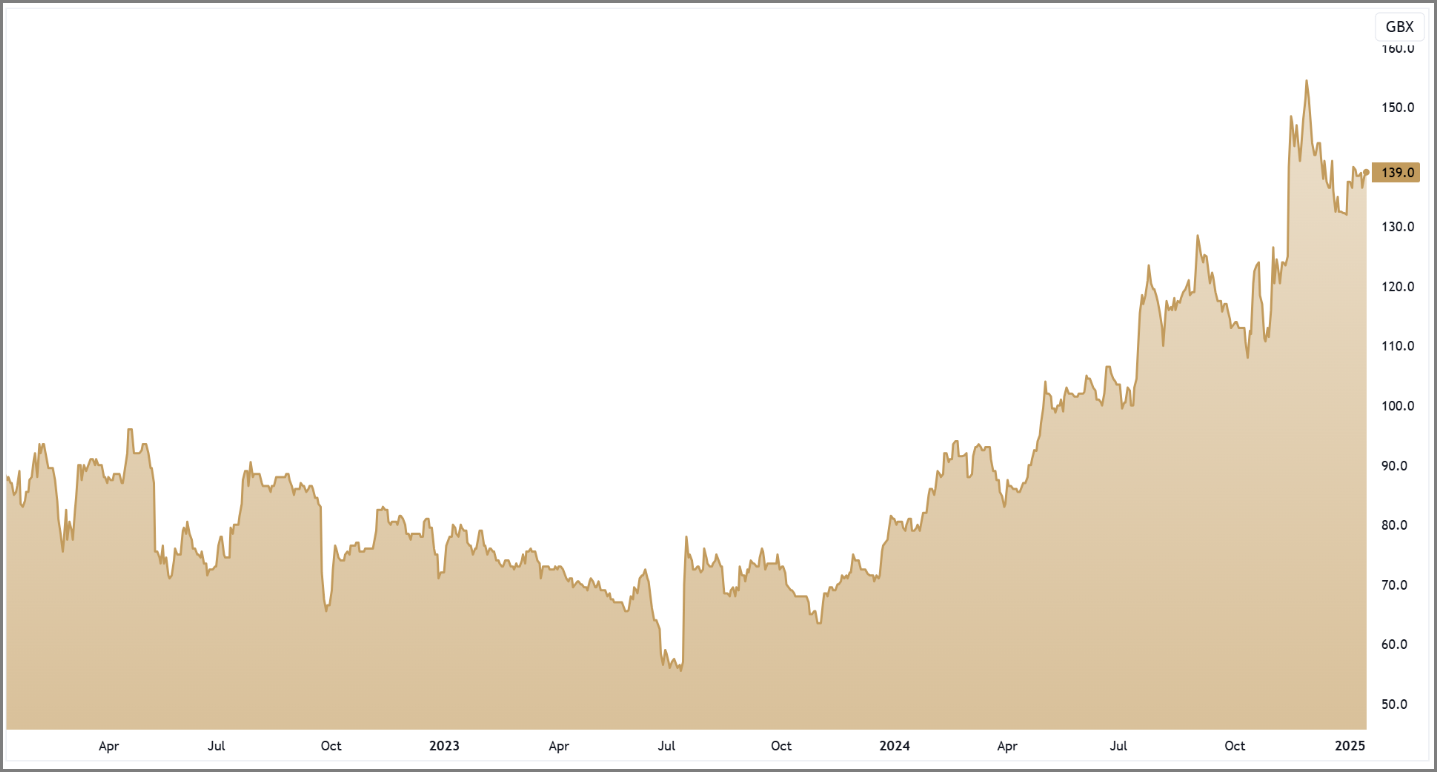

Technical analysis: Riding the uptrend

Concurrent’s share price mirrors the company’s strong momentum. The stock’s long-term uptrend is clear, with the 50-day moving average diverging above the 200-day moving average—a textbook signal of sustained bullish momentum. This alignment indicates continued market confidence in the company’s growth story.

In November, the shares hit new highs, driven by multiple contract wins. Since then, the price has pulled back to the support of the 50-day moving average, creating a healthy consolidation. For retail investors, this pullback presents a potential entry point to join the broader trend without overpaying.

From a valuation perspective, this period of consolidation offers a chance to capitalise on the company’s growth trajectory. With the technical indicators pointing to continued strength, the stock appears poised to resume its upward climb. For those looking to ride the momentum, now might be the time to act.

A record year in the making

Concurrent’s unscheduled trading update this morning, confirms that FY24 will be a record year. Revenue is set to jump 25% year-on-year, while profit growth reflects operational scaling despite strategic investments in the Systems division. The achievement of 22 design wins, including 10 major contracts, underscores the company’s ability to secure long-term revenue streams.

With a growing order book, a strong balance sheet, and an expanding global footprint, Concurrent is entering 2025 with momentum and optimism. For investors seeking a small-cap with big potential, this company is proving that it can deliver growth, stability, and market-leading performance.

CNC 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.