18th Dec 2025. 9.07am

Regency View:

BUY Boku (BOKU)

Regency View:

BUY Boku (BOKU)

Boku: The infrastructure behind the global payment shift

Payment technology is full of companies promising to disrupt the way the world pays. Very few actually do it. Boku sits in a far more durable position. It is not trying to reinvent payments, but rather to connect the world’s largest digital merchants to the systems real consumers already use. As global commerce moves steadily away from cards and towards localised digital payment methods, Boku’s network has become essential infrastructure for reaching the next billions of users.

The interesting part is that Boku already operates at a scale most AIM companies never achieve. It processes billions in payment volume, connects merchants to nearly one hundred million monthly users and continues to grow at rates that would turn heads on the Nasdaq. Yet despite this, sentiment around the stock remains calm, almost quiet. It is an unusual mix of rapid operational progress and steady market perception. For long term investors, that combination often creates opportunity.

A network built for a new world of payments

Boku’s role is simple to describe but difficult to replicate. It provides the pipes that allow global merchants to accept mobile wallets, account to account payments, real time bank transfers and carrier billing. In markets where credit cards are not dominant, Boku is often the only way major digital brands can reach their customers.

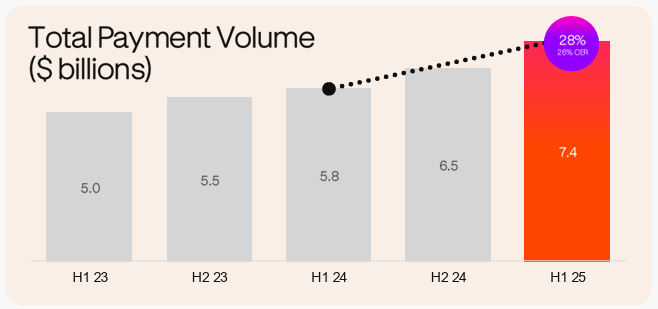

This is not theoretical. Monthly active users reached 95.5m in June, up 20% in a year, with 44m new users added in just six months. Total payment volume increased to $7.4bn and the company delivered 60 new merchant connections during the half. Behind these numbers sits a powerful network effect. Each new merchant makes the platform more attractive to users, and each new user makes the platform more attractive to merchants. This circular dynamic compounds over time.

The growth engine is shifting decisively towards digital wallets and account to account methods. Revenues in these segments grew 89% in the first half. This is exactly where consumer behaviour is moving, particularly in emerging markets, and Boku has positioned itself ahead of the curve. Carrier billing still contributes meaningfully, especially through bundling arrangements, but the long term story is firmly anchored in next generation payment methods where Boku has a clear operational advantage.

Execution that matches the ambition

Operationally, the company is delivering with impressive consistency. First half revenue grew 34% to $63.3m and adjusted EBITDA increased by 53% to $21.8m. Margins sit comfortably above 30%, demonstrating strong operating leverage as the network scales.

Underlying performance is even cleaner once temporary launch phase pricing is excluded. On this basis, revenue grew more than 25% and digital wallet and account to account revenue grew more than 60%. In a sector where many competitors are struggling to defend margins, Boku has managed to expand them.

The balance sheet is a major strength. Total group cash reached $192m at the half year and Boku’s own cash increased to $87.3m even after repurchasing $12.3m of its own shares. Net debt is negative by a wide margin. This gives Boku the freedom to invest, acquire and innovate without funding risk or dilution.

Management reaffirmed medium term guidance for more than 20% organic revenue growth on a compound basis and EBITDA margins above 30%. That level of confidence is meaningful, particularly in an industry undergoing so much change.

A valuation supported by growth, quality and cash

Boku trades on a forward price to earnings ratio of 25.9 times which places it in quality growth stock territory. The PEG ratio of 1.2 highlights that valuation and growth are broadly aligned, especially given forecast EPS growth of 27.4%.

Price to sales of 7.15 times may appear high at first glance, but it reflects a business with exceptional margin potential and minimal incremental cost per new transaction. The price to free cashflow ratio of 14.5 times seems modest given the balance sheet strength and the scale of cash generation relative to market value.

The company’s ability to self fund expansion is a strategic differentiator. With more than $190m of cash on hand, Boku can accelerate product development, broaden its network and pursue targeted acquisitions. Many fintechs do not have that luxury.

Analysts currently hold a target price of £3.20 which implies more than 50% potential upside from current levels. That reflects not a speculative rerating, but a normalisation of valuation in line with peers achieving similar growth and margin profiles.

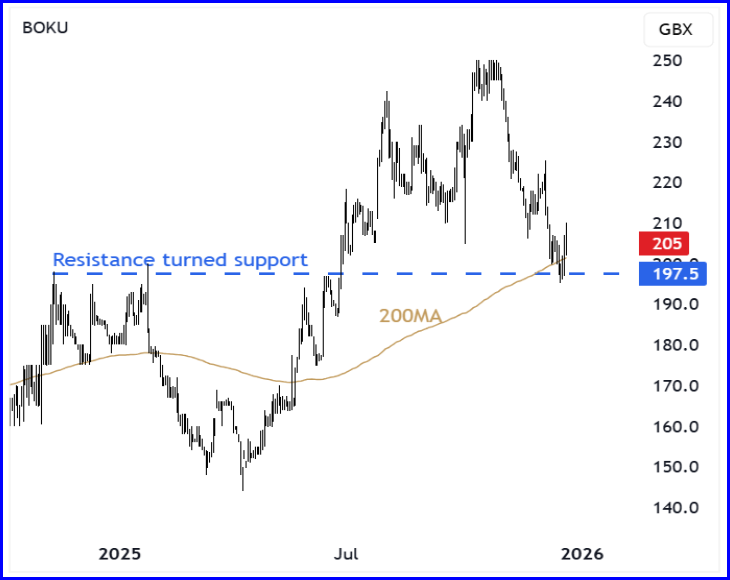

A constructive technical backdrop built on confluence

In technical analysis, confluence matters because it highlights areas where multiple forms of support come together. Boku is currently trading back at one of those key zones. Prices have pulled back to retest a broken resistance level that previously acted as the launch point for the last leg higher. This same area now coincides with the 200 day moving average.

In uptrends, broken resistance often holds as support. Traders who entered during the breakout tend to defend their positions when price revisits that zone. The 200 day moving average adds a second layer of support since it remains one of the most widely observed indicators among long term investors and institutions. When a high quality growth stock pulls back into this type of confluence and begins to stabilise, it often marks the start of the next continuation phase.

Boku’s price action fits that template. Momentum has cooled, but the broader structure remains intact. The market appears to be resetting, not reversing.

A company built for the long term transition in payments

Boku sits at the heart of a structural shift in how people pay online. It is enabling merchants to reach users in ways traditional payment systems cannot. It is growing rapidly in the right segments, delivering strong margins and building a balance sheet that offers genuine optionality. Most importantly, it is doing all of this with remarkable consistency.

The share price does not fully reflect the scale, quality or resilience of the business. For investors looking to own a high growth infrastructure provider in one of the most enduring themes in global commerce, Boku offers a compelling blend of visibility, financial strength and long term upside.

Five key takeaways

1. Structural growth leader: Boku is powering the global shift toward digital wallets and account to account payments.

2. Strong execution: Revenue rose 34% and EBITDA grew 53% with margins holding above 30%.

3. Fortress balance sheet: More than $190m of cash and no debt provide real strategic flexibility.

4. Growth at a fair price: A forward P E of 25.9 and PEG of 1.2 reflect a reasonable valuation for the pace of expansion.

5. Confluent support zone: The pullback into prior resistance and the 200 day average offers a constructive technical backdrop.

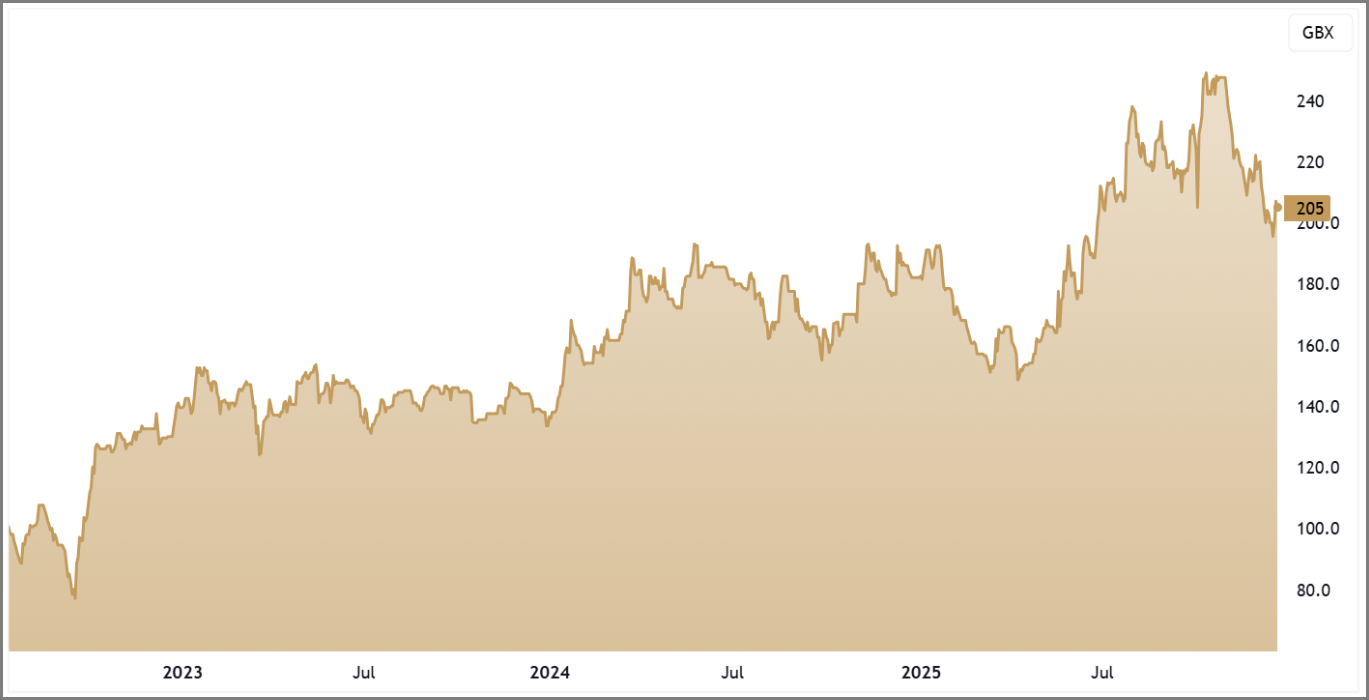

BOKU 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.