21st May 2026. 9.04am

Regency View:

BUY accesso Technology (ACSO)

Regency View:

BUY accesso Technology (ACSO)

Too Cheap to Overlook

Momentum investors usually have an easy life. You find a company producing strong numbers, the chart points from bottom left to top right and the market does most of the heavy lifting for you. accesso Technology (ACSO) is different.

The shares have lost more than half their value over the past year and the chart still carries the scars of that decline. Yet underneath the surface, the business itself appears to be moving in the opposite direction. Profits are rising, cash continues to build and management has been buying back shares aggressively. When a share price and business performance start moving in different directions, it can sometimes create opportunity.

The market may be focusing on the wrong story

accesso provides technology solutions for attractions, venues and leisure operators around the world. Its software helps businesses manage ticketing, virtual queues, guest experiences, eCommerce and payments. Put simply, if you have booked a ticket online, skipped a queue at a major attraction or interacted with digital guest systems, there is a reasonable chance accesso’s technology has been working in the background.

The business now serves more than 1,100 venues across 31 countries, giving it a broad customer base and reducing reliance on any individual customer relationship. While investors often think of accesso as a ticketing company, the model has evolved into something much wider, with multiple products increasingly integrated into a broader platform.

Importantly, this creates opportunities for cross selling. Once a customer adopts one solution, accesso can potentially introduce additional products across payments, commerce and guest management. That matters because recurring software revenues and deeper customer relationships tend to create more predictable earnings over time.

The numbers continue moving in the right direction

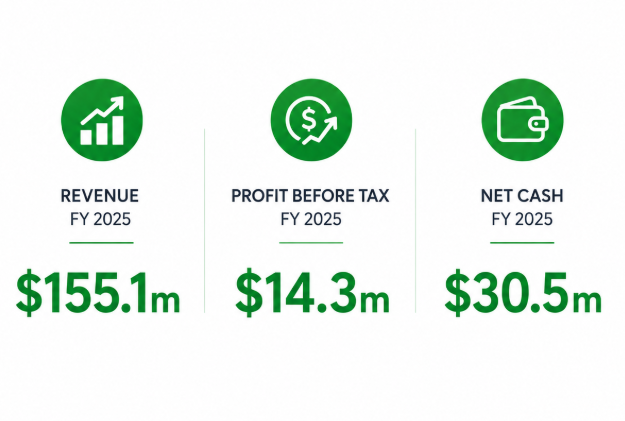

The latest full year results painted a better picture than the share price might suggest. Revenue increased 1.8% to $155.1m, although stripping out disposals and non recurring items gives an underlying growth figure closer to 3.8%.

More interestingly, earnings growth moved ahead of sales growth. Profit before tax increased 37.7% to $14.3m, while adjusted earnings per share rose 15.3% to 44.3 cents.

The balance sheet also remains in good shape. Net cash improved to $30.5m, giving the company flexibility to continue investing while supporting shareholder returns. Despite this, the shares currently trade on a forward PE ratio of around 8.6 times, with a price to free cash flow multiple near 5 times. Those are not the sort of numbers normally associated with profitable software businesses.

Management is backing the story with real money

Management teams often tell investors they believe their shares are undervalued. The real question is whether they are willing to act on it.

During 2025, accesso repurchased approximately $15.9m of shares through market buybacks. Following the year end, the company also completed a further $20m tender offer.

Combined, this represents almost $36m being returned to shareholders.

For a company with an enterprise value of roughly £64m, that is meaningful. These are not token buybacks designed for headlines. Management clearly believes the market has become too pessimistic.

A new CEO arrives at an interesting time

Leadership changes can sometimes create uncertainty, particularly when a company is already under pressure. Here, the situation looks very different.

Lee Cowie officially became Chief Executive in May following a succession process that had been planned for over a year. Prior to joining accesso, Cowie served as Chief Technology Officer at Merlin Entertainments, overseeing technology across more than 125 attractions in 28 countries.

That feels relevant.

He understands the market from the customer side rather than arriving as an outsider learning the industry. His stated priorities also align closely with where management sees future growth opportunities, particularly around payments, AI capabilities and commercial execution.

The recent acquisition of AI analytics specialist Dexibit adds another piece to that puzzle. Rather than simply attaching artificial intelligence to an investor presentation, accesso appears to be embedding it into products that already sit across its existing ecosystem.

Has the selling finally run out of steam?

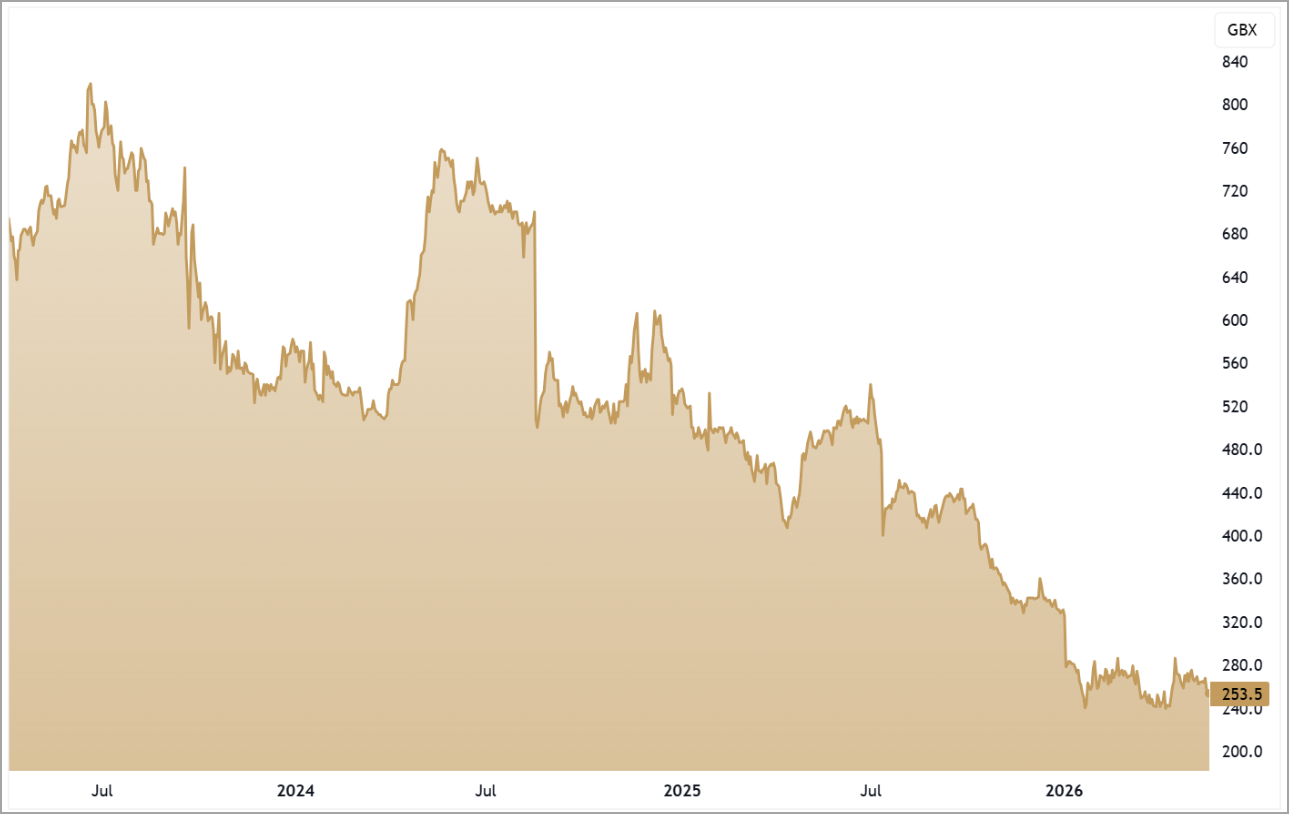

The chart remains the weakest part of the investment case.

After trading above 550p last year, the shares entered a prolonged decline and remain below the longer term moving averages. Momentum investors will look at the chart and immediately move on.

More recently though, the character of price action appears to be changing. Instead of continuing to make aggressive lower lows, the shares have spent several months stabilising around the 240p to 280p region.

Contrarian opportunities often work like this. Fundamentals stabilise first and price follows later. We are not there yet, but the early ingredients may be starting to appear.

Five Key Takeaways

1. Valuation Gap: The shares trade on earnings and cash flow multiples that look unusually low for a profitable software business.

2. Profit Growth: Profit before tax increased 37.7%, showing earnings improving faster than revenue.

3. Balance Sheet: Net cash of $30.5m provides flexibility and reduces financial risk.

4. Management Confidence: Nearly $36m has been returned to shareholders through buybacks and tender offers.

5. Contrarian Setup: The fundamentals appear to be improving while sentiment around the shares remains weak.

ASCO 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.