28th Mar 2019. 9.00am

Regency View:

BUY Clinigen (CLIN)

Regency View:

BUY Clinigen (CLIN)

Clinigen has the prescription for success

Speciality pharma firm Clinigen has been on the acquisition warpath recently. It’s made several significant purchases, some of which haven’t been cheap. This has been a tough pill to swallow for some investors (no pun intended) and, as a result, the share price has pulled back over the last 18 months or so. However, we believe Clinigen’s ambitious plans to consolidate these acquisitions will produce impressive growth that should drive the shares significantly higher once again.

Unique business model

Clinigen is a specialist pharmaceutical services company which helps hospitals around the world deliver ‘the right medicine to the right patient at the right time’. These are often hard-to-access drugs, for patients with high unmet medical needs. It does this by working with pharma companies, making their products available for a volume-based fee, as well as by buying up the rights to other drugs, which Clinigen supplies itself.

What makes Clinigen unique (enabling it to access the most innovative types of treatment available) is that it works across all three areas of drug supply: clinical trials, unlicensed and licensed medicines. It is, in fact, the only company to globally manage access to medicine across all three routes worldwide.

Expanding global footprint

With a market cap of £1.21bn, Clinigen is already one of the largest companies listed on AIM), but CEO Shaun Chilton has ambitious plans for it to become much, much bigger. He wants even greater control of the global drugs supply chain and has his sights sets on several new markets, including Latin America and Russia. Chilton reckons there are still plenty of significant growth opportunities in distributing drugs that are too small for the pharma multinationals to be interested in.

For the last couple of years, Chilton’s expansion strategy has been largely focused on acquisitive growth. In September 2017, Clinigen snapped up weaker rival firm Quantum Pharma (which operates in a similar space) for £160m. Then, in September last year, Clinigen further expanded its geographical footprint with two more acquisitions. The first of these was Swiss pharma firm iQone, for £6.7m on a cash, debt free basis. The second was CSM, a medical packaging and distribution specialist, with locations throughout Continental Europe and the US. This purchase was significantly more expensive at £115m and was funded in part by a placing, which raised £80m.

Whilst these acquisitions have been costly, we think the future rewards could be significant. Clinigen now has a much stronger position both in Europe and the US. Looking ahead, the company’s main priority will be to consolidate these purchases, as the focus shifts more towards organic growth, whilst improving operational efficiency. Quantum Pharma has already delivered over £1.1m of cost synergies and we except CMS to significantly boost revenues in all three of Clinigen’s divisions.

Revolutionary digital platform

To support the drive for global expansion, Clinigen has another trick up it’s sleeve. At an investor presentation in November last year, the company revealed plans to boost growth of its unlicensed medicine division using solution bridging the gap between busy healthcare professionals and pharmaceutical companies all over the world. Cliniport, a smart online product sourcing and ordering platform. Cliniport presents a clever

The platform allows doctors to quickly and easily source a vast array of hard-to-access speciality treatments, alternative medicines and drugs that are currently at risk of shortage. Over 3,000 of these are available for next day delivery. Cliniport also provides comprehensive information from doctors about the progress of programs using the drugs it lists and their effectiveness against different conditions. This database also offers the pharmaceutical companies a unique insight into how their products are being delivered.

Cliniport is already being used by over 11,000 health care professionals, but the highly scalable nature of this e-commerce platform could be a catalyst for substantial earnings growth, once their colleagues around the world catch on.

Game changing recent deal

As well as making several key acquisitions recently, in February this year Clinigen also spent £163m securing the US rights to cancer treatment Proleukin, from Swiss pharma giant Novartis. Having already owned the rights to Proleukin outside the States since July 2018, this deal is very big news indeed and means that Clinigen now has exclusive global ownership of the drug.

Proleukin is thought to work by encouraging the immune system to slow down, or possibly even stop, cancer cell growth. The treatment is currently active in approximately 80 clinical trials in the US, across several different types of cancer. According to Clinigen, the drug could become ‘an integral part’ of future cancer combination therapies.

The deal, which is expected to complete next month, has been forecast to increase earnings per share by 24% in the financial year to June 2021 and by 23% in the following year.

Impressive growth expected to continue

Taking a look at the figures for Clinigen already paints a very positive picture. Over the last five years, sales have posted a compound annualised growth rate of over 25%. When the group published its last set of full-year results, in September 2018, it reported a 28% rise in sales to £381.2m and a whopping 155% jump in pre-tax profit to £35.9m. These impressive gains were also backed up by a strong operational cashflow of 39.1 pence per share.

Broker forecasts predict that next year Clinigen sales will increase to £454.0m and the company will achieve a pre-tax profit of £89.2m. In our view, given the potential of its recent acquisitions, the scalability of Cliniport and its ownership of the global rights to Proleukin, these figures are more than achievable, and possibly even slightly conservative.

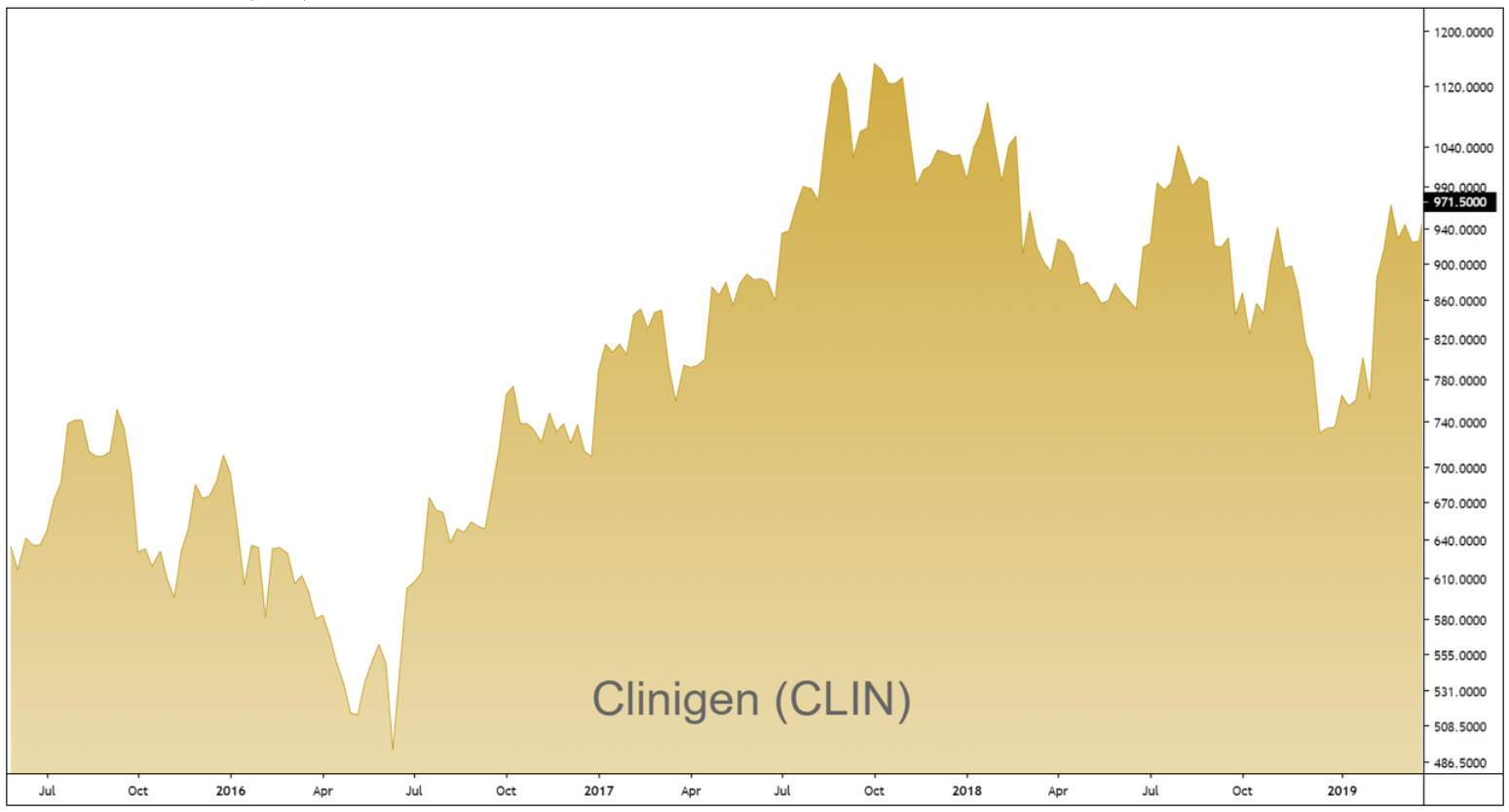

With catalysts like these to drive the share price higher again, we see no reason why they shouldn’t re-visit all-time highs of £11.86, as reached in 2017. That gives a potential upside of more than 28% from the current share price. And, with a current valuation of 13 times future earnings, we think this could be a good time for investors to join the Clinigen growth story.

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.