29th May 2026. 11.02am

Weekly Briefing – Friday 29th May

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | +0.06% |

| FTSE 250 | +2.45% |

| FTSE All-Share | +0.33% |

| AIM 100 | +3.65% |

| AIM All-Share | +3.25% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 29th May

Market Overview

Dear Investor,

In a week that’s been defined by soaring temperatures across much of the UK, it’s perhaps fitting that one market has started to cool. Brent crude has spent the past week drifting back towards the lower end of its trading range as traders become increasingly confident that a diplomatic solution to the conflict in the Middle East may eventually emerge.

The optimism stems from reports that negotiations between the US and Iran are making progress, encouraging investors to scale back some of the geopolitical risk premium that has supported oil prices in recent months. Markets, after all, are forward looking and tend to react long before events actually unfold.

However, there remains a meaningful difference between improving sentiment and improving fundamentals. This week, Chevron chief executive Mike Wirth warned that energy markets remain far tighter than headline price action might suggest, arguing that inventories continue to be drawn down and that the market’s ability to absorb further supply shocks has been significantly reduced.

That leaves oil at an interesting juncture. The market may be becoming more comfortable with the prospect of a diplomatic breakthrough, but it is far less clear that the underlying supply picture has improved to the same degree. For now, Brent remains within the broad range that has developed since the conflict began, suggesting investors are still weighing optimism over what could happen next against the realities of today’s energy market.

Wishing you a great weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: JD Sports (LSE:JD.) +10.2% on the week

JD Sports moved higher this week, extending a recovery that has now seen the shares rally more than 28% from their May lows as investors appear to be warming once again to the longer term story.

Interestingly, there has not really been one standout headline driving the move. Instead, the recovery seems to reflect growing confidence that the market may have become too pessimistic earlier in the year as concerns around weaker consumer spending and softer trainer demand weighed heavily on sentiment across the retail sector.

The group’s recent full year results painted a steadier picture than the share price had perhaps implied. Revenue increased more than 10% to £12.7bn, free cash flow jumped 36% to £462m and North America returned to like for like growth during the fourth quarter. Management also continues to push ahead with its global expansion plans, AI integration and e-commerce upgrades as it looks to improve efficiency and customer engagement across the business.

Regency View: JD still looks cheap relative to both its scale and growth profile, trading on around 7 times forward earnings despite continuing to generate strong cash flow. The shares remain well below last year’s highs, but momentum has started to improve technically and the market appears to be reassessing whether the earlier selloff had become overly aggressive.

Greencore slipped this week despite reporting strong underlying growth following its acquisition of Bakkavor earlier this year.

On the surface, the numbers looked solid enough. Pro forma revenue increased 3.2% while adjusted operating profit jumped more than 15%, helped by cost efficiencies and improving margins. Management also reiterated guidance and said integration plans remain on track, with expectations for at least £80m of annual cost synergies over the next three years.

The problem for investors was not really the operational performance, but the balance sheet and cash flow impact following the deal. Net debt has risen sharply following the acquisition, while free cash flow turned negative during the half as integration costs and working capital outflows started to weigh on the numbers. In other words, the market appears to be moving from excitement about the takeover towards scrutiny over execution.

Regency View: The long term strategic logic behind the Bakkavor deal still looks sensible, creating a dominant player in UK convenience foods with greater scale and stronger customer relationships. However, the shares have struggled to regain momentum since the acquisition completed, with investors now wanting proof that promised synergies can translate into stronger cash generation rather than simply bigger revenues.

Sector Snapshot

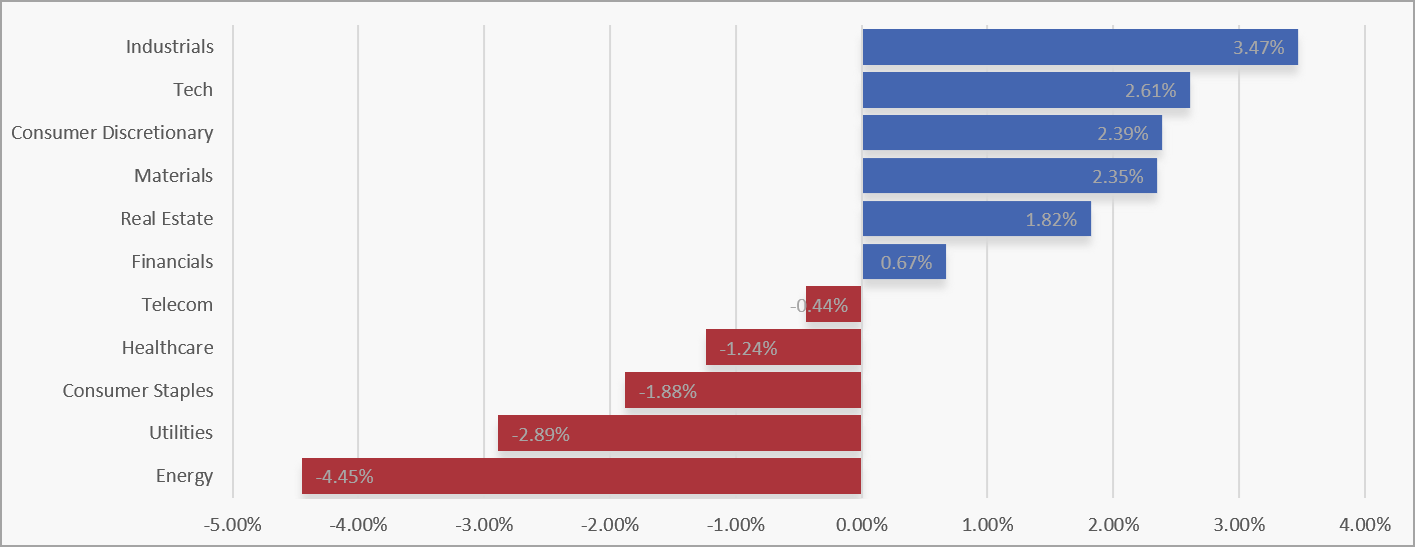

Industrials led the market this week, with Tech and Consumer Discretionary close behind as investors rotated back towards growth and economically sensitive sectors. Materials also recovered well after last week’s weakness, while Real Estate and Financials posted respectable gains. The leadership mix suggests confidence has improved, with investors showing a greater willingness to look beyond defensive areas and towards sectors more closely tied to economic activity.

At the other end of the table, Energy suffered the sharpest decline, giving back some of its recent outperformance, while Utilities and Consumer Staples also struggled. Healthcare drifted lower and Telecoms slipped modestly, reinforcing the view that defensive sectors took a back seat as money flowed back into cyclicals and growth-oriented names.

UK Sector Performance (7-Days)

UK Price Action

The FTSE’s attempted breakout has lost momentum this week, with prices failing to hold above both swing resistance and the descending trendline that connects the major lower highs from March and April. After looking as though buyers were finally ready to wrestle back control, the market has instead slipped back into its recent trading range, highlighting that sellers remain active whenever prices start to push higher.

From a technical perspective, this leaves the FTSE at an interesting crossroads. The rejection is disappointing for the bulls, but it has not yet done enough damage to suggest a fresh leg lower is underway. Instead, the market appears stuck between support and resistance, waiting for a catalyst strong enough to break the deadlock. For now, the longer term trend remains intact, but buyers will need to see the FTSE reclaim recent highs soon if they want to avoid this period of consolidation evolving into something more concerning.

UK100 Daily Candle chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.