22nd May 2026. 11.01am

Weekly Briefing – Friday 22nd May

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | +2.84% |

| FTSE 250 | +2.05% |

| FTSE All-Share | +2.74% |

| AIM 100 | -1.98% |

| AIM All-Share | -1.61% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 22nd May

Market Overview

Dear Investor,

With political uncertainty on the rise and the conflict in the Middle East still hanging over markets, it would be easy to be down on UK plc. The headlines certainly have not given investors much to work with recently. But beneath the noise, recent economic data painted a more encouraging picture than many might have expected.

The UK economy expanded by 0.6% during the first quarter, making it the strongest performer among the major developed economies so far this year. Growth was broad based, with services, manufacturing and construction all contributing despite higher energy prices and a backdrop that has felt anything but stable.

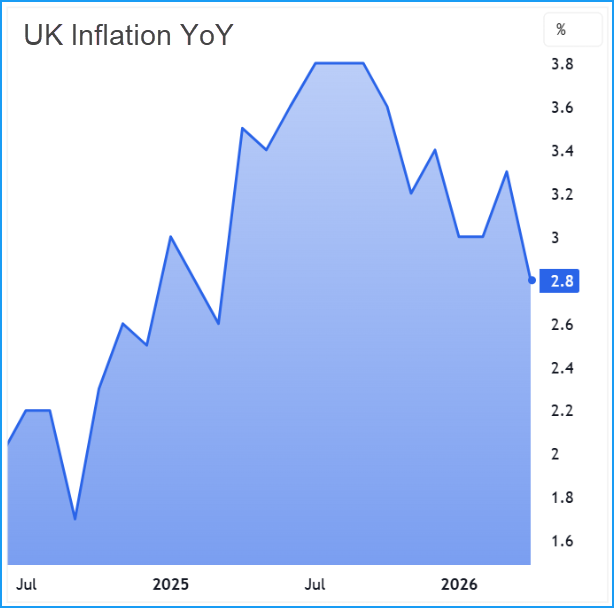

Inflation also moved lower than expected, falling to 2.8% and offering some relief after fears that higher energy costs would quickly feed through into household budgets and business costs. Taken together, stronger growth and softer inflation is not a combination many investors would have expected a few months ago.

That said, markets are already looking ahead rather than celebrating where we have just been. Some businesses appear to have brought activity forward ahead of higher energy costs, while the labour market has started to show signs of cooling. There is also a growing sense that the first quarter may prove easier than the environment businesses face over the rest of the year.

For investors though, there is an important point here. The UK economy continues to show a degree of resilience that often gets overlooked. While sentiment around Britain can swing between pessimism and outright doom fairly quickly, the underlying picture remains more balanced than the headlines often suggest.

Wishing you a great weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Marks & Spencer (LSE:MKS) +10.4% on the week

Marks & Spencer moved higher this week as investors looked beyond the disruption caused by last year’s cyberattack and focused instead on management’s confidence that profit growth is set to return.

The results themselves reflected a difficult year, with profits falling after the cyber incident disrupted online operations, impacted product availability and created additional costs across the business. The attack was not insignificant, forcing the suspension of online clothing orders and creating knock-on effects throughout parts of the group.

What appeared to reassure investors was the message around what comes next rather than what has already happened. Management highlighted a strong balance sheet and expects profits this year to move back above levels seen before the disruption. Food continued to perform well and gain market share, while the company believes there remains further upside in fashion, home and beauty as normal trading conditions return.

Regency View: The market seems increasingly willing to treat last year’s disruption as a temporary setback rather than a change in the broader story. Momentum has cooled from the highs seen earlier in the year, but the underlying turnaround still appears intact, with management now shifting the focus back towards execution rather than recovery.

Ithaca Energy moved lower this week despite reporting a steady first quarter update, with production remaining broadly stable and full year guidance reiterated. The company highlighted strong operational execution, improved liquidity and continued progress across its development portfolio.

The update also pointed to attractive shareholder returns, with dividend guidance now expected to come in above $500m for the year as elevated commodity prices support cash generation. Ithaca also extended its hedge book during the current high price environment, helping protect future cash flows while retaining some exposure to upside in oil and gas prices.

However, the shares slipped as investors looked beyond the headline dividend support and focused on the moving parts within the portfolio. Adjusted EBITDAX and profit before tax were lower year on year, operating costs increased, and an equipment handling incident at Rosebank is expected to take the rig off hire for several months. For a stock that had already enjoyed a strong run, that was enough to trigger some profit taking.

Regency View: Ithaca remains a cash generative energy stock with a significant shareholder return profile, but expectations had clearly risen after a powerful move over the past year. This looks less like a broken story and more like a reminder that even high-yield energy names can wobble when operational detail gives investors something to pick at.

Sector Snapshot

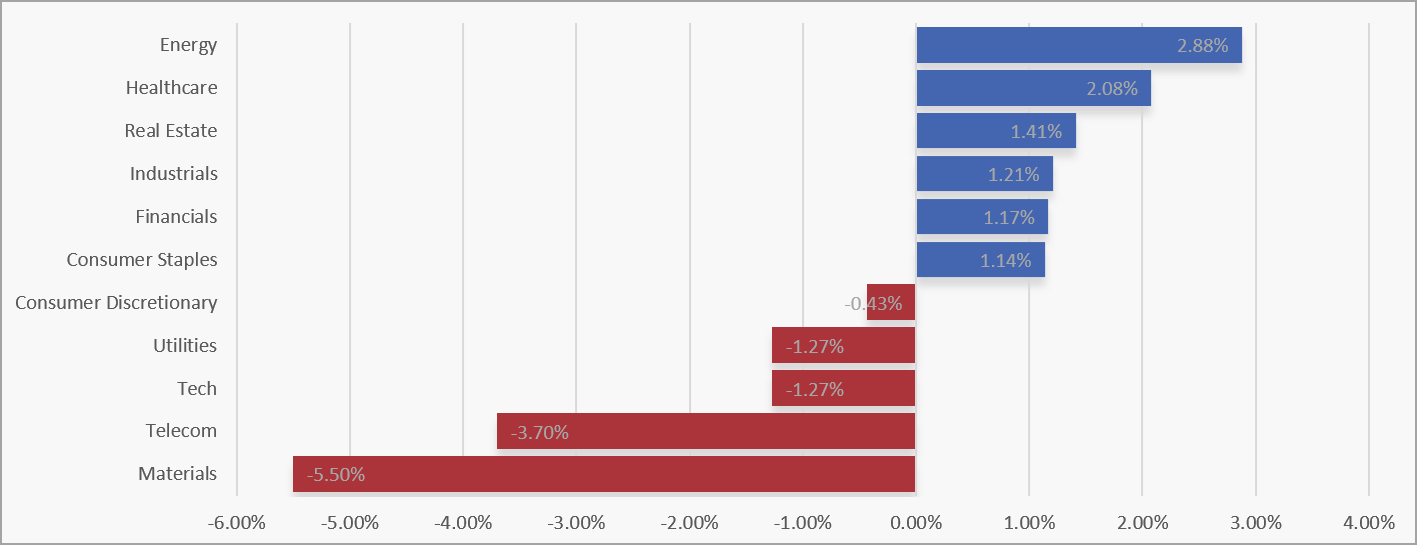

Energy moved back to the top of the table this week, with Healthcare also delivering a strong performance as investors rotated towards a mix of defensives and commodity-linked names. Real Estate, Industrials and Financials all posted healthy gains, while Consumer Staples added further support, suggesting leadership was spread across several areas rather than concentrated in one theme.

At the weaker end, Materials saw a sharp pullback after several weeks of strength, while Telecoms also struggled. Tech and Utilities slipped back too, with Consumer Discretionary only marginally lower. The shift suggests investors are becoming more selective, taking profits in recent winners while rotating into sectors offering a blend of stability and value.

UK Sector Performance (7-Days)

UK Price Action

It has been a strong week for the FTSE, with the market once again rejecting the support zone we have highlighted in recent updates and pushing firmly higher. Buyers have stepped back in with more conviction this time, helping price break above the short term descending trendline and drive into recent swing highs.

The tone has shifted noticeably over the past few sessions. Rather than repeatedly testing support and printing lower highs, the market is now starting to challenge resistance and rebuild some upside momentum. The next hurdle is whether the FTSE can convert these recent swing highs into support, because if buyers can maintain control here, the broader trend starts to look much healthier again and attention could quickly turn back towards the March highs.

UK100 Daily Candle chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.