15th May 2026. 10.42am

Weekly Briefing – Friday 15th May

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | -0.02% |

| FTSE 250 | -1.58% |

| FTSE All-Share | -0.19% |

| AIM 100 | -1.30% |

| AIM All-Share | -0.63% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 15th May

Market Overview

Dear Investor,

For a market that spent much of the past year obsessing over inflation, interest rates and AI, it has been Westminster that grabbed investors’ attention this week. And, in fairness, not even Netflix could have scripted this one particularly convincingly.

What started as a bruising set of local election results for Labour has quickly descended into something that feels somewhere between a political drama and an office leaving party that got badly out of hand. Rumours around Keir Starmer’s future, Wes Streeting stepping down and Andy Burnham preparing a possible return to Westminster have left markets wondering whether the government is still focused on running the country or simply running internal auditions for the next leader.

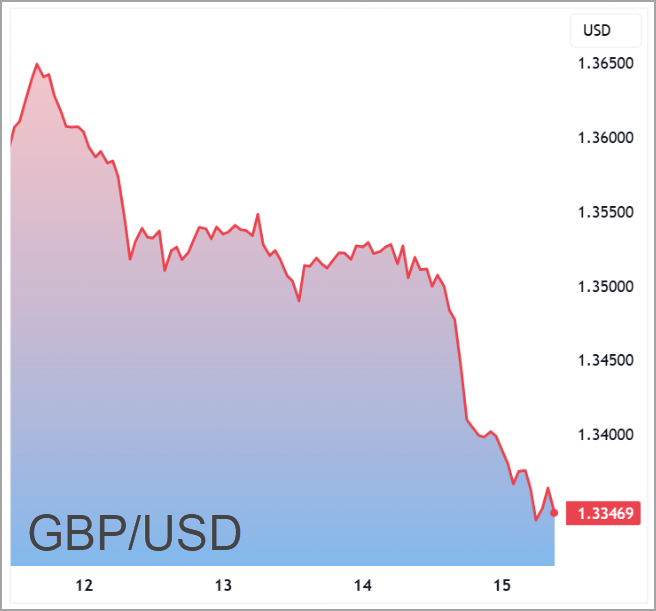

Markets rarely enjoy political uncertainty, but the real issue this week has been what it could mean for the UK’s finances. Sterling weakened, gilt yields pushed sharply higher and traders started revisiting memories of the Liz Truss era with the sort of nervous expression usually reserved for someone hearing an unexplained noise from their car engine. Fairly or unfairly, the concern is that a shift further left politically could eventually mean looser borrowing rules and more pressure on already stretched public finances.

Interestingly, the frustration from business leaders has been unusually blunt. Several FTSE executives openly criticised the chaos this week, with one reportedly describing Westminster as a “comic convention”. Harsh perhaps, but probably not entirely inaccurate from the perspective of investors trying to price UK assets while ministers appear to be spending more time briefing against each other than briefing the country.

The irony is that underneath all the political theatre, parts of the UK market have actually held up reasonably well. But politics has a habit of overwhelming everything else when investors start questioning stability itself. As we head into the weekend, the market is no longer just watching inflation prints and company earnings, it is watching Westminster, trying to work out whether this is simply another bout of political melodrama or the start of something that genuinely begins to weigh on confidence in UK assets.

Wishing you a great weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Tate & Lyle (LSE:TATE) +45.2% on the week

Tate & Lyle surged this week after confirming it had received a conditional takeover proposal from US ingredients giant Ingredion, sending the shares sharply higher as investors moved to price in the possibility of a deal.

Under the proposal, shareholders could receive value of up to 615p per share through a combination of cash and permitted dividends, representing a substantial premium to where the shares had been trading prior to the announcement. The company confirmed that discussions between the two sides are ongoing, although stressed there remains no certainty that a formal offer will ultimately be made.

The move has once again highlighted the growing trend of overseas buyers targeting UK-listed companies, particularly those with stable cash flows, established global operations and valuations that continue to look relatively undemanding compared to international peers. Tate & Lyle fits neatly into that category, with the business having spent recent years repositioning itself towards higher-growth speciality ingredients and healthier food solutions.

Regency View: Whether a formal bid materialises or not, the sharp reaction reflects a market that increasingly believes parts of the UK market remain undervalued on the global stage. Tate & Lyle had already been quietly rebuilding momentum operationally, but this week’s move underlines how quickly sentiment can change once strategic interest emerges.

Burberry moved lower this week after investors focused on the impact that the Iran conflict is now having on luxury spending and international tourism, particularly across Europe and the Middle East. While the company’s quarterly sales broadly met expectations, the market reaction reflected growing concern that the wider backdrop for luxury brands remains difficult.

The key weakness came from Burberry’s Europe, Middle East, India and Africa division, where sales slipped as the conflict disrupted tourism flows and reduced spending from Middle Eastern shoppers. That matters because luxury brands rely heavily on international travel and high-end tourist spending, particularly in major shopping hubs across Europe. Reuters also reported that the wider luxury sector has already started to feel the impact from weaker travel activity linked to the conflict.

Operationally, there were still signs that the turnaround strategy itself is making progress. Burberry continued to see stronger demand in the Americas and China as management pushes the brand back towards its heritage positioning around trench coats, scarves and classic British luxury. But this week’s reaction showed that even improving execution can struggle to overcome a weakening consumer backdrop when geopolitical uncertainty starts weighing on travel and discretionary spending.

Regency View: Burberry increasingly looks like a business that is operationally improving, but the market is becoming more concerned about the environment it is trying to recover in. Luxury demand remains highly sensitive to confidence, tourism and global stability, and this week was a reminder that even well-executed turnarounds can lose momentum when the macro backdrop deteriorates.

Sector Snapshot

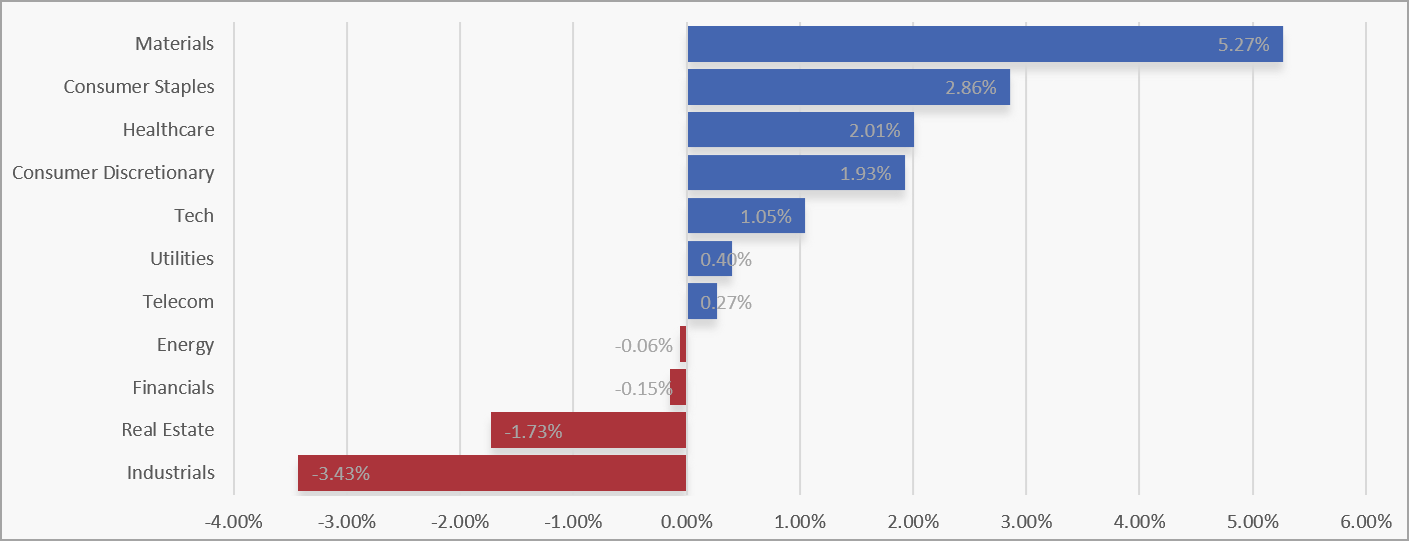

Materials once again led the market this week, extending the sector’s recent run of strength, while Consumer Staples and Healthcare also performed well. Consumer Discretionary and Tech added solid gains too, suggesting investors are still willing to back selective growth areas, although with a more balanced tone than the aggressive risk rotation seen previously.

At the weaker end, Industrials saw a sharp reversal after last week’s strong rally, while Real Estate also slipped back. Energy and Financials were broadly flat, with Telecoms and Utilities posting only modest gains, pointing to a more selective market where leadership is narrowing again.

UK Sector Performance (7-Days)

UK Price Action

What had started as a more encouraging week for the FTSE looks set to end on a softer note, with the market giving back a large chunk of its gains into the weekend. Having successfully defended the 10,171 support zone for the fourth time in less than two weeks, buyers initially stepped back in and pushed the market higher, suggesting there was still appetite to buy dips within this broader consolidation phase.

However, Friday’s price action has shifted the tone somewhat. At the time of writing, the FTSE is being sold into the weekend, forming another lower swing high and dragging price back towards support once again. The repeated tests of this area are becoming increasingly important because, while support has held so far, markets rarely enjoy knocking on the same door forever. If buyers cannot stabilise things quickly next week, the risk of a deeper breakdown starts to increase.

UK100 Daily Candle chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.