8th May 2026. 11.27am

Weekly Briefing – Friday 8th May

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | -1.24% |

| FTSE 250 | +1.99% |

| FTSE All-Share | -0.85% |

| AIM 100 | +2.47% |

| AIM All-Share | +2.33% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 8th May

Market Overview

Dear Investor,

The oil market spent much of this week trying to convince itself that diplomacy might finally be gaining the upper hand. After surging towards $115 earlier in the month, Brent crude pulled sharply lower as Donald Trump talked up progress in negotiations with Iran and suggested the Strait of Hormuz could soon reopen fully to global shipping.

For a brief moment, markets appeared willing to buy into it. Oil retreated, equities stabilised and traders began to position for the idea that perhaps the worst of the geopolitical panic was behind us. Unfortunately, by the end of the week, the situation had once again descended into something that has been widely dubbed a “Swiss cheese ceasefire” full of holes and increasingly difficult to take seriously.

That really has been the defining feature of this market. One moment Trump is talking about peace, diplomacy and progress. The next, missiles are flying, warships are exchanging fire and fresh military action is being described by the President as a mere “love tap”. At this stage, markets are not just trying to price geopolitics, they are trying to price Trump’s mood from one press conference to the next, which is not exactly a framework most traders would build into their spreadsheets voluntarily.

Interestingly though, despite the increasingly chaotic backdrop, oil has not returned to the highs. That suggests the market still believes a broader regional escalation may ultimately be avoided, even if confidence in the ceasefire itself is wearing thin. In other words, traders appear to be viewing this less as the start of a full-scale energy shock and more as an unstable negotiation process being conducted with all the subtlety of a reality television finale.

The takeaway is that volatility remains the real story. As we head into the weekend, markets are once again caught between diplomacy and escalation, with Trump’s words continuing to pull prices in one direction while events on the ground pull them in another. For now, the market still seems willing to give diplomacy the benefit of the doubt, but it is becoming increasingly clear that investors are dealing with a ceasefire that looks far more fragile than the headlines initially suggested.

Wishing you a great weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Greatland Resources (AIM:GGP) +8.5% on the week

Greatland Resources moved higher this week as renewed strength in the gold price helped push the shares back towards recent highs, with investors continuing to warm to the company’s growing position as a major gold and copper producer.

The move builds on a strong operational update released at the end of April, where the group reported another quarter of robust production alongside a record cash build. Operational performance at Telfer continues to improve under Greatland ownership, with high recoveries, rising material movements and growing confidence that full-year production will come in towards the upper end of guidance.

What continues to stand out is the strength of the balance sheet and the scale of the growth pipeline now sitting behind the story. The business remains debt free with substantial cash generation, while ongoing drilling success and the significant upgrade to the Telfer resource base are helping reinforce the market’s view that Greatland is evolving into a long-life mining platform rather than simply a single-asset success story.

Regency View: Momentum remains firmly with Greatland, with the shares continuing to benefit from both operational delivery and a supportive backdrop for gold. After years of being viewed primarily as an exploration story, the market is increasingly starting to treat Greatland as a serious producer with scale, cash flow and long-term growth potential.

Entain moved lower this week after the company confirmed that hedge fund veteran Ricky Sandler will step down from the board, with his investment firm Eminence Capital also set to liquidate its sizeable stake in the business over time.

While the move appears linked primarily to the closure of Eminence Capital itself rather than a direct loss of confidence in Entain, the news still landed awkwardly for a stock that has struggled badly with momentum over the past year. Large shareholder exits rarely help sentiment, particularly when the market already has concerns around execution, leverage and the broader direction of the business.

Sandler was brought onto the board in early 2024 as part of a push to improve shareholder value and sharpen strategic focus, so his departure inevitably raises questions around what comes next. Although he stated he retains “utmost confidence” in management and the board, the reality is that an orderly unwind of more than 40 million shares still creates a significant technical overhang for the market to absorb.

Regency View: Entain increasingly feels like a stock stuck between value and uncertainty. On paper the shares screen cheaply relative to historic earnings potential, but weak momentum, elevated debt and continued questions around execution mean the market is still struggling to regain conviction in the story.

Sector Snapshot

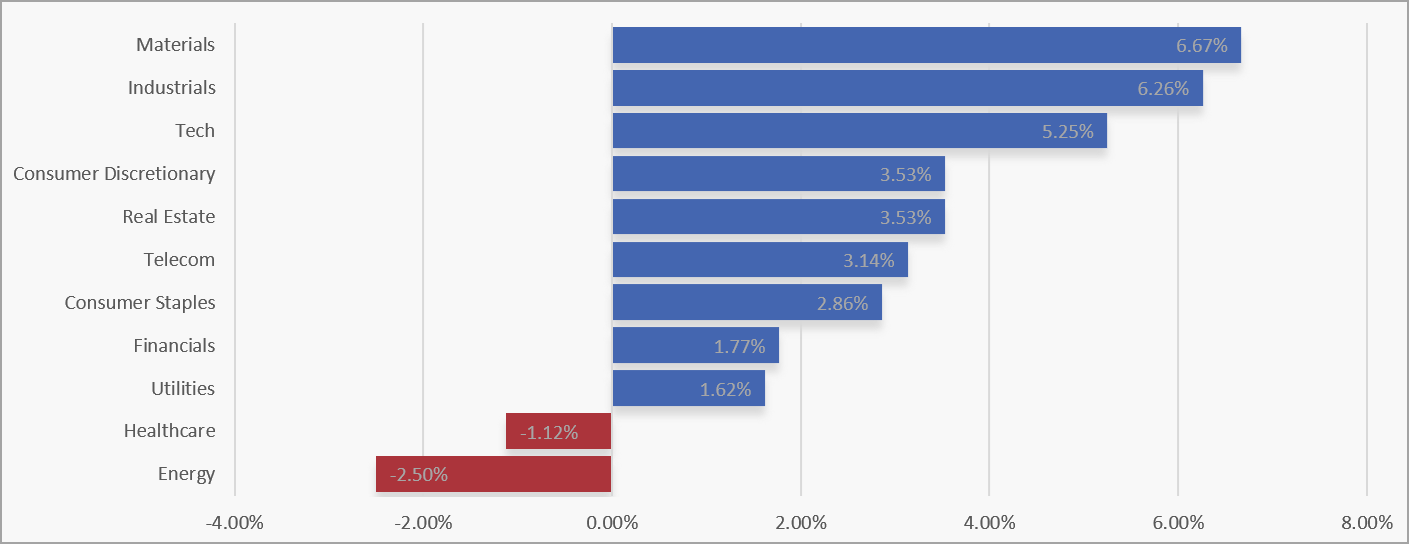

Materials and Industrials dominated this week, with Tech also posting a very strong performance as investors rotated firmly back into cyclical and growth-sensitive sectors. Real Estate and Consumer Discretionary added to the momentum, while Telecoms and Consumer Staples also delivered healthy gains, pointing to broad participation rather than narrow leadership.

At the weaker end, Energy and Healthcare were the only sectors to finish lower. Utilities and Financials still managed gains, but the clear theme this week was a decisive move back towards risk, with investors favouring sectors linked to economic activity, infrastructure and growth over traditional defensives.

UK Sector Performance (7-Days)

UK Price Action

Given the mixed macro headlines surrounding the conflict in the Middle East, it is no real surprise to see the FTSE spend much of this week chopping sideways. Under the surface though, the technical picture has weakened slightly, with the market forming another lower swing high while struggling to build any meaningful upside momentum following recent rebound attempts.

Price is now pressing against swing support as we head into the weekend, which makes this an important area to watch. A decisive break and close below this level would suggest sellers are beginning to regain control and could see next week get off to a shaky start. On the other hand, if buyers can defend support once again, we may simply remain trapped within this messy consolidation phase while the market waits for clearer macro direction.

UK100 Daily Candle chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.