1st May 2026. 11.17am

Weekly Briefing Friday 1st May

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | -0.65% |

| FTSE 250 | -0.91% |

| FTSE All-Share | -0.66% |

| AIM 100 | -0.32% |

| AIM All-Share | -0.46% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing Friday 1st May

Market Overview

Dear Investor,

$700bn is a hard number to comprehend. Yet that is roughly what the world’s largest technology companies are now set to spend on AI infrastructure this year, a figure that has continued to edge higher over the past few days.

While headlines remain focused on geopolitics, this is where the real story is unfolding. The biggest names in global markets are committing vast sums to data centres, cloud capacity and custom chips, laying the foundations for the next phase of digital growth. This is not a short-term trend, it is a structural shift that is reshaping the direction of markets.

At this stage, it is no longer just about growth. As investment ramps up, the focus naturally turns to where that capital is going and which businesses are best placed to benefit from it. Not every company exposed to AI will win, and the gap between those that execute well and those that do not is already starting to widen.

For UK investors, this is where things get interesting. While the companies driving this investment are largely US-based, the opportunities are not confined to the US. The supply chains, infrastructure providers and specialist businesses supporting this build-out are spread across global markets, and that includes the UK.

The takeaway is straightforward. The AI story is not going away, but it is evolving. From here, it becomes less about following the theme and more about identifying where the real opportunities are starting to emerge.

We are actively tracking the UK-listed companies benefiting from this shift inside our research.

ACCESS our latest FTSE & AIM ideas here

Wishing you a great weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Tullow Oil (LSE:TLW) +41.9% on the week

Tullow Oil moved higher this week following the release of its full year results, with the update highlighting a business that is starting to stabilise after a prolonged period of restructuring. The company has continued to narrow its focus around its core assets in Ghana, alongside the disposal of non-core operations and a reduction in costs.

A key milestone has been the completion of a comprehensive refinancing, which extends the group’s debt profile and provides greater financial flexibility. This has been a critical step in underpinning the investment case, allowing management to shift attention away from balance sheet concerns and back towards operational delivery.

That operational momentum is now beginning to show through. Production has improved into the early part of the year, supported by progress across the Ghana drilling programme and the extension of key field licences. With oil prices remaining elevated amid ongoing geopolitical tensions, the combination of improved execution and a supportive macro backdrop has helped to bring the shares back into focus.

Regency View: Tullow remains a higher-risk turnaround story, but momentum is beginning to build as the business shifts from restructuring towards delivery. With improving operational performance and clear exposure to energy prices, the shares are starting to reflect a market that is willing to give the story another look.

Taylor Wimpey moved lower following its latest trading statement, which pointed to steady sales but a more challenging backdrop for the UK housing market. While customer demand remains resilient overall, the company highlighted ongoing affordability pressures and a more uncertain macro environment.

Underlying trends suggest conditions are beginning to tighten. The group reported a slight decline in sales rates compared to the same period last year, alongside a modest reduction in its order book. More notably, pricing within the order book is now lower year on year, reflecting increased pressure in areas where affordability is more stretched, particularly in the South of England.

Cost pressures are also starting to come through. The company expects build cost inflation to remain in the low to mid single digits for the year, driven in part by rising energy costs and supply chain surcharges. While Taylor Wimpey continues to emphasise operational discipline and the strength of its landbank, the update reflects a market that remains sensitive to both pricing and cost dynamics.

Regency View: Taylor Wimpey remains a well-run operator, but the shares continue to reflect a housing market that is struggling to gain momentum. With affordability constraints and cost pressures still in play, the near-term outlook is likely to remain challenging despite the group’s underlying strengths.

Sector Snapshot

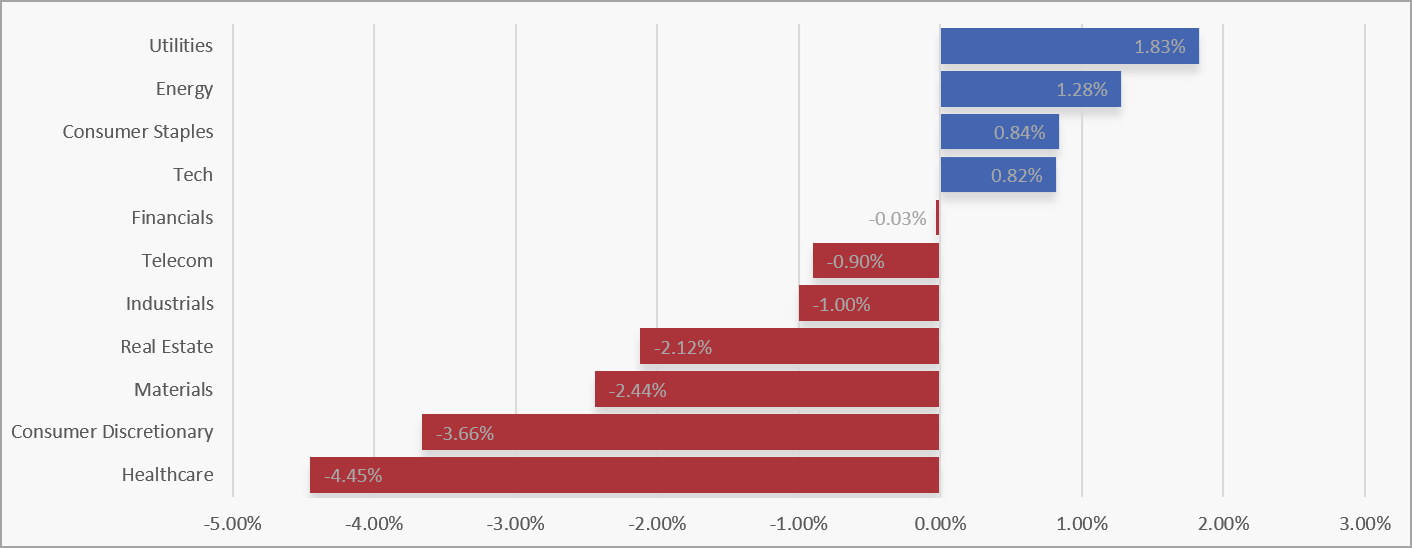

Utilities led the market this week, with Energy and Consumer Staples also finishing higher, pointing to a clear tilt towards more defensive and income-focused areas. Tech managed a small gain, but beyond that, strength was limited and fairly concentrated.

At the weaker end, Healthcare saw the sharpest decline, followed by Consumer Discretionary and Materials. Real Estate and Industrials also slipped, while Telecom and Financials edged lower, highlighting a cautious tone with investors stepping back from more cyclical and growth-sensitive sectors.

UK Sector Performance (7-Days)

UK Price Action

It is the end of the week and the FTSE has continued to move lower following the failed bull flag breakout we highlighted last week, with that loss of momentum now feeding through into a more sustained pullback. What initially looked like a pause within an uptrend has instead rolled over into a clearer sequence of lower highs, with sellers gradually taking control as the week has progressed.

That said, we did see a pick up in buying appetite on Thursday, with prices stabilising and attempting to bounce from intraday weakness. For now it looks more like a pause within the decline rather than a decisive shift in momentum, but it does suggest that buyers are still active at lower levels. The key question into next week is whether that demand can build into something more meaningful, or whether rallies continue to be sold into as the market works through this reset phase.

UK100 Daily Candle chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.