24th Apr 2026. 10.55am

Weekly Briefing Friday 24th April

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | -2.68% |

| FTSE 250 | -2.99% |

| FTSE All-Share | -2.69% |

| AIM 100 | -1.83% |

| AIM All-Share | -1.78% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 24th April

Market Overview

Dear Investor,

While the conflict in Iran continues to dominate the headlines, the real story building across equity markets is the resurgence of AI.

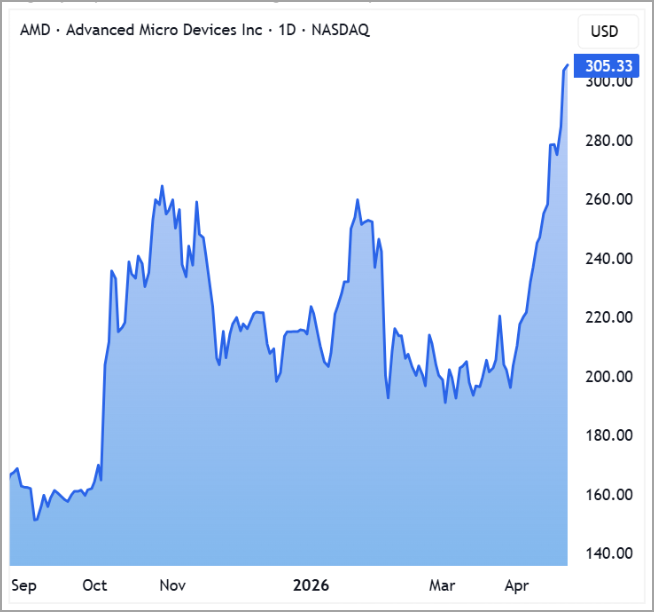

US tech stocks have surged in recent weeks, with Nvidia up more than 20% from its recent lows, Arm Holdings gaining over 30% this month, and Advanced Micro Devices rallying more than 50%. This is not a marginal move, it is a decisive shift in momentum back towards the sector that has driven global markets over the past two years.

What is increasingly clear is that this move is being underpinned by something more structural. Chipmaker SK Hynix has pointed to a “structural shift” in demand, with customers prioritising access to AI hardware over price as supply struggles to keep up. At the same time, large technology companies are committing vast sums to build out the infrastructure required to support AI, creating demand that is flowing through the entire semiconductor supply chain.

Importantly, this strength is now clearly visible within the UK market. Over the past month, semiconductors have surged nearly 100%, tech hardware is up more than 70%, and communications stocks have gained over 30%, with broader tech also delivering strong double-digit returns. This is theme is tailwind for our FTSE Investor and AIM Investor portfolios in which we hold some of the UK markets most exciting AI stocks.

The takeaway is that while the headlines remain focused on geopolitics, capital is being drawn towards structural growth, and that trend is now showing up closer to home. For UK investors, that leaves the market in a stronger position than it might first appear, with momentum building beneath the surface rather than being driven purely by global flows.

CLICK HERE to see the UK-listed AI and tech names we’re backing right now.

Wishing you a great weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Serica Energy (AIM:SQZ) +11.8% on the week

Serica Energy moved higher this week as renewed focus on energy security following the conflict in Iran supported sentiment across the sector. With concerns around supply disruption pushing oil prices higher, UK-listed producers have come back into favour, and Serica has been a clear beneficiary of that shift.

Alongside the supportive macro backdrop, the company delivered a solid operational update, reporting first quarter production of 39,100 barrels of oil equivalent per day, with second quarter output to date averaging over 49,000. Full year guidance remains unchanged at comfortably above 40,000 BOEPD, reinforcing confidence in the group’s production profile.

The update also highlighted a more proactive approach to capital allocation, with the company exploring the potential issuance of a new five-year senior unsecured bond as it looks to optimise its capital structure. While this introduces greater financial flexibility, the market reaction has been driven primarily by the combination of improving production and a more favourable energy backdrop.

Regency View: Serica remains a core holding within our AIM Investor portfolio, with momentum firmly to the upside as the shares continue to trend higher. With supportive energy prices and improving sentiment across the sector, the stock remains well positioned if the current backdrop continues to hold.

Rolls-Royce (RR.) moved lower this week, falling alongside the wider aerospace and defence sector as heightened uncertainty around US-Iran negotiations weighed on market sentiment. The sector, which had previously benefited from rising geopolitical tensions, saw a sharp reversal, with European aerospace and defence stocks posting their steepest one-day decline in over a year.

The weakness came as investors began to reassess the near-term outlook for the conflict, with markets reacting to mixed signals around a potential ceasefire. While tensions remain elevated, the shift towards negotiation, combined with positioning that had become increasingly stretched, prompted a pullback across the sector. Rolls-Royce, alongside peers such as Safran and Thales, was caught up in that broader move lower.

Adding to the pressure, broker sentiment also softened slightly, with Jefferies trimming its price target on the shares. While this was not a major downgrade, it reinforced the sense that after a strong run, expectations across the sector may have moved ahead of near-term fundamentals, leaving the shares more sensitive to any shift in sentiment.

Regency View: This looks more like a reset in momentum rather than a change in the underlying story, with the shares reacting to positioning and macro headlines rather than company-specific weakness. With momentum easing after a strong run and the shares still trading on around 30x forward earnings, the market may need to see the next leg of earnings delivery before buyers step back in with conviction.

Sector Snapshot

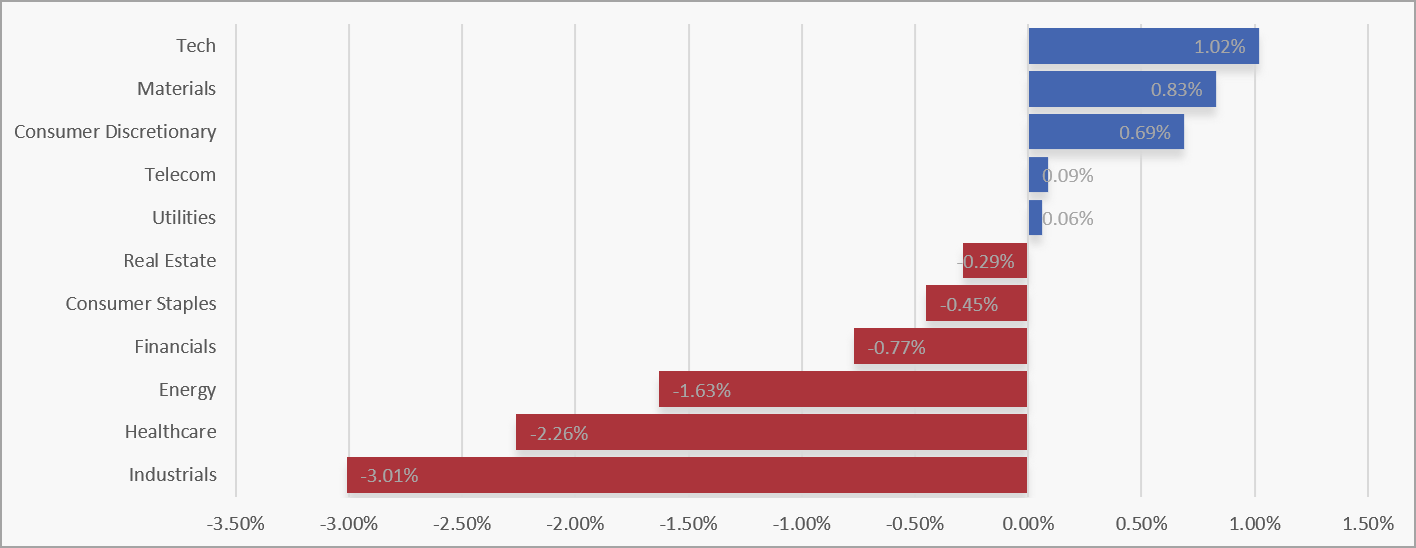

Tech led the way this week, with Materials and Consumer Discretionary also managing modest gains. Telecoms and Utilities were little changed, suggesting a fairly muted tone where only a handful of sectors were able to push higher with any conviction.

At the weaker end, Industrials saw the sharpest pullback, followed by Healthcare and Energy. Financials and Consumer Staples also drifted lower, while Real Estate edged back, pointing to a market that remains selective with limited appetite beyond a few pockets of strength.

UK Sector Performance (7-Days)

UK Price Action

The FTSE has started to print some more interesting and slightly more cautionary price action. What initially looked like a clean breakout from a small bull flag has failed, with the market rolling back over and slipping below the flag structure, the short term ascending trendline, and the 50 day moving average.

That shift matters. Failed breakouts often act as a warning sign that momentum is beginning to fade, and the speed of this move lower suggests buyers have stepped back, at least in the short term. The focus now turns to whether this is simply another shakeout within a broader uptrend or the early stages of a deeper pullback, with price now testing whether demand can re-emerge at lower levels or if sellers start to press their advantage.

UK100 Daily Candle chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.