10th Apr 2026. 9.58am

Weekly Briefing – Friday 10th April

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | +2.44% |

| FTSE 250 | +2.80% |

| FTSE All-Share | +2.47% |

| AIM 100 | +4.53% |

| AIM All-Share | +4.40% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 10th April

Market Overview

Dear Investor,

It’s been a week of bluster and brinkmanship, the likes of which we have perhaps not seen for a generation. Heinous threats from Donald Trump have been followed by a fragile ceasefire, creating a backdrop that remains extremely tense. Yet despite the increasingly extreme tone of the headlines, markets have remained far more composed than many would have expected.

For UK stocks, the rotation back into risk began before some of Trump’s most aggressive messaging had even hit the wires. The FTSE’s relief rally started to build into the Easter period and continued despite the has continued despite the escalation in tone, suggesting that positioning and sentiment were already shifting independently of the headlines.

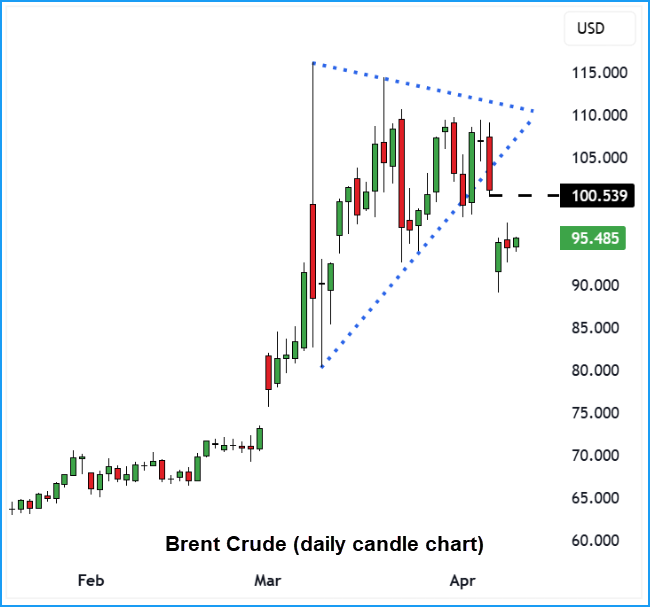

Across other asset classes, the reaction has been equally telling. Oil initially moved sharply, but the subsequent pullback has lacked conviction, pointing to a market that is still unsure how to price disruption risk. Gold has failed to behave like a traditional safe haven, trading sideways rather than pushing higher, while the US dollar has weakened and equities globally have moved higher. Taken together, this is not a market bracing for worst case outcomes.

What stands out is the growing disconnect between rhetoric and reaction. Trump’s increasingly erratic tone, swinging from threats of escalation to sudden calls for de escalation, has created a constant stream of noise, but markets appear to be filtering it out. Whether that reflects confidence or complacency remains an open question, but it is clear that words alone are no longer enough to shift positioning in a meaningful way.

The key question now is what comes next. We have had the relief rally across equities and the initial reaction in oil, but the next phase will be driven by whether rhetoric can translate into reality. Can shipping flows genuinely normalise through the Strait of Hormuz, and will Trump’s push towards de escalation hold, or will markets once again be forced to react to another abrupt shift in tone.

For now, investors appear willing to trust the deescalation narrative, but that patience may prove limited if actions fail to match the rhetoric.

Wishing you a great weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Greatland Resources (AIM:GGP) +14.8% on the week

Greatland Resources moved higher this week after delivering a strong March quarter production update, reinforcing confidence in both operational execution and cash generation. The group reported quarterly production of 82,723oz of gold alongside copper output, putting year-to-date production at just under 250,000oz and keeping the company firmly on track to meet, or slightly exceed, full-year guidance.

The standout figure, however, was the balance sheet. Cash increased by $260m over the quarter to $1.2bn, achieved after capital expenditure and tax payments, leaving the business debt free and in a position of significant financial strength. That level of cash generation at this stage of the cycle is clearly resonating with investors, particularly given Greatland’s full exposure to the gold price on the upside.

There was also reassurance around operations in the context of the current Middle East conflict. The company confirmed that Telfer remains insulated from supply disruptions, with secure fuel sourcing, on-site power generation and more than 12 months of stockpiles. In a market increasingly focused on geopolitical risk, that level of operational resilience adds another layer of confidence to the investment case.

Regency View: Strong production, a rapidly growing cash pile and zero debt underline the quality of the business at current gold prices. With earnings momentum building and full exposure to the gold price, this remains one of the cleaner ways to play strength in the sector.

Entain has continued to decline in recent months, with the shares now down around 30% year to date and nearly 50% below last summer’s highs. The move reflects a sustained period of weakness in price action, with the stock consistently trading below its key moving averages.

Recent updates have been limited, with one of the more notable developments being confirmation that the UK accounting watchdog has taken no action following its investigation into the company’s 2022 audit. Broker coverage has also remained cautious, with Citigroup recently trimming its price target.

Financially, the group continues to report modest revenue growth, but profitability remains under pressure. Operating margins are negative, returns on capital remain weak, and net debt has continued to trend higher, while book value has declined over recent years.

Regency View: The trend remains firmly to the downside, with persistent weakness in both price action and underlying metrics. Until there are signs of stabilisation, the burden of proof remains on the bulls.

Sector Snapshot

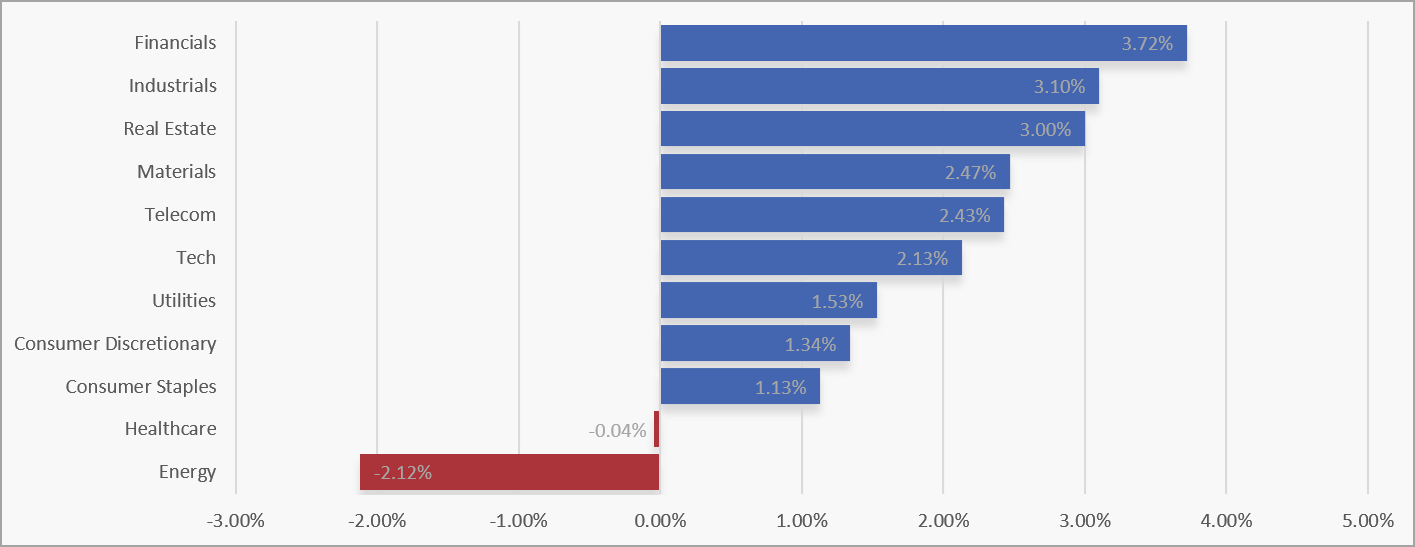

It has been a strong week across the board, with Financials, Industrials and Real Estate leading the move higher as money rotates back into cyclicals. Materials and Telecoms also posted solid gains, while Tech joined the advance, suggesting this is more than just a narrow bounce. The FTSE had already started to lean back into risk ahead of the Easter break, and that shift has carried through this week as sentiment has steadied.

At the other end of the spectrum, Energy was the clear laggard, giving back some of its recent outperformance, while Healthcare was broadly flat. Utilities and Industrials sat towards the weaker end despite still closing higher, pointing to a market that is rotating rather than moving in one clean direction, with leadership shifting away from defensives and back towards growth-sensitive areas.

UK Sector Performance (7-Days)

UK Price Action

It is a new week and having broken out from its descending retracement channel last week, the FTSE has held onto its gains and is now consolidating above the 50 day moving average. The recovery has been sharp and, somewhat incredibly, the market now sits just a few percent below its recent highs. From a technical perspective, that shift in behaviour is worth noting as it suggests the recent sell off may have been more of a shakeout than a structural change, with buyers quickly reasserting control and keeping the broader uptrend firmly intact.

UK100 Daily Candle Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.