1st Apr 2026. 9.00am

Regency View:

BUY RELX (REL)

- Growth

- Income

Regency View:

BUY RELX (REL)

RELX: A Data Powerhouse Built on Recurring Revenue

RELX has gone from being one of the FTSE’s most consistent performers to one of its biggest laggards over the past year. The shares have been caught in a sharp de-rating driven by AI disruption fears and a shift away from premium-rated growth stocks. However, the latest results suggest the fundamentals remain firmly intact, highlighting a growing disconnect between price and performance.

Mission-Critical Products with High Customer Stickiness

RELX is not a traditional publisher, despite its roots. Today, it is a global provider of data, analytics and decision tools, serving customers across risk, scientific research, legal services and exhibitions. In simple terms, it helps professionals make better decisions using proprietary data and increasingly sophisticated analytics.

This is an attractive model. Revenues are largely recurring, driven by subscription-based products that are deeply embedded in customer workflows. Whether it’s insurers assessing risk, researchers accessing scientific data, or legal professionals using analytics tools, RELX’s products are mission-critical, which supports both pricing power and retention.

Over time, the group has steadily shifted its business mix towards higher-value analytics and decision tools. This matters. It means the business is not just growing, but improving in quality, with higher margins and stronger long-term visibility as customers rely more heavily on its data-driven platforms.

Growth Still Intact, Margins Still Expanding

The latest full-year results underline just how well this model is working. Revenue grew 7% on an underlying basis to £9.59bn, while adjusted operating profit increased 9% to £3.34bn. Earnings per share rose 10% on a constant currency basis, continuing a long track record of consistent growth.

What stands out most is margin progression. The adjusted operating margin expanded to 34.8%, up from 33.9% the year before. That is an exceptionally high level for a business of this scale, and it reflects a combination of pricing power, operational discipline and a continued shift towards higher-margin analytics products.

Cash flow remains a core strength. Cash conversion came in at 99%, allowing the company to both invest in growth and return significant capital to shareholders. The dividend increased by 7% to 67.5p, while £1.5bn was returned via buybacks in 2025, with a further £2.25bn planned for 2026.

There is also no sign of growth slowing. Management expects another year of strong underlying revenue and profit growth in 2026, supported by continued momentum across all divisions. The ongoing integration of artificial intelligence into its products is not a new initiative, but an evolution of a strategy that has been driving value for over a decade.

A Sell-Off Driven by Pressure, Not Performance

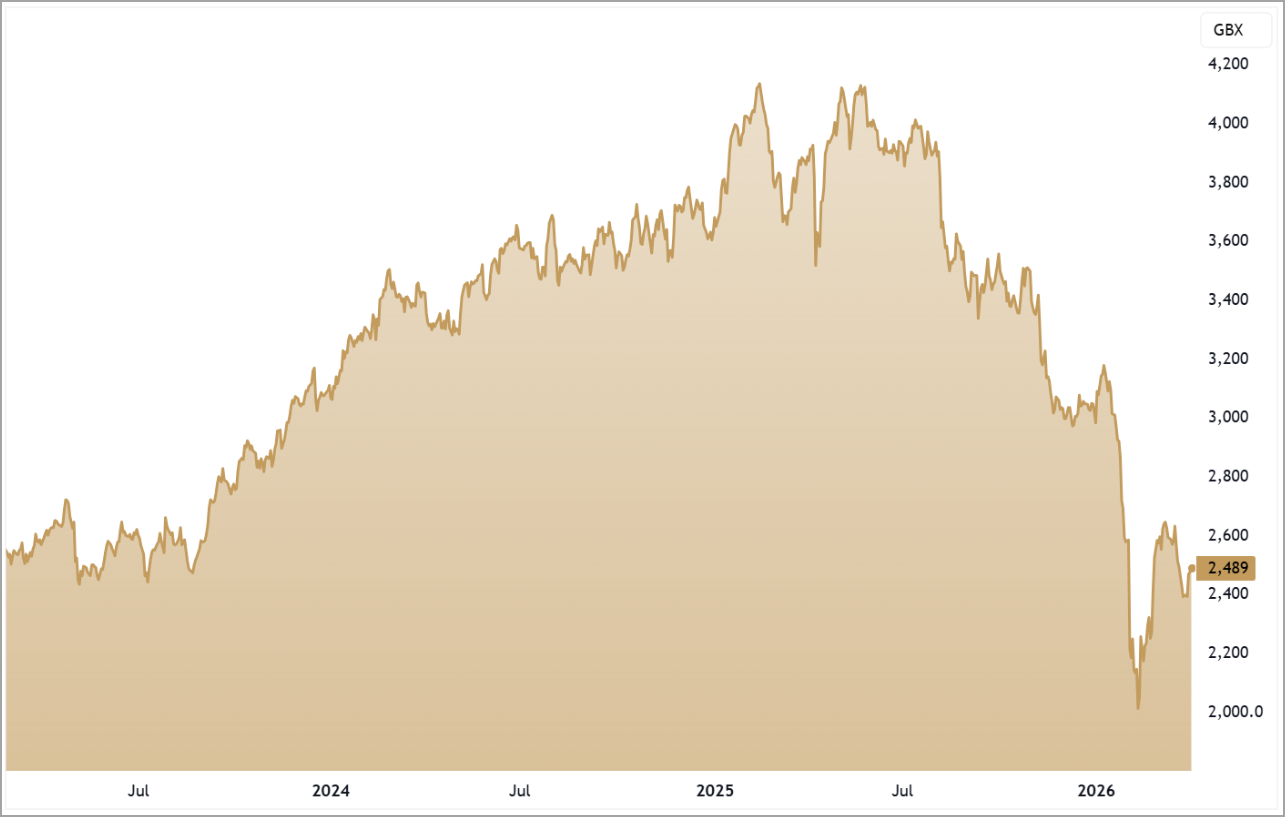

Despite this, the share price tells a very different story. RELX has fallen sharply from its highs, leaving the shares trading well below their 52-week peak and firmly under the 200-day moving average.

The reasons for this move are not hard to identify, but they are largely external. A broader valuation reset has hit premium-rated compounders as interest rate expectations have shifted higher. At the same time, capital has rotated aggressively into sectors directly benefiting from geopolitical tensions, leaving steady growers like RELX out of favour.

More recently, technical pressure has played a role. A large institutional shareholder exited a significant position via a secondary placing in mid-March, adding a substantial amount of supply to the market. Importantly, the placing was completed at only a modest discount and was well supported, suggesting demand for the shares remains intact.

Concerns around artificial intelligence have also weighed on sentiment, with some investors questioning whether advances in AI could disrupt RELX’s business model. However, this overlooks a key point. RELX is not being disrupted by AI, it is actively embedding it into its products, enhancing functionality and strengthening its competitive position.

Valuation Reset Meets Capital Support

With the share price under pressure, valuation has moved to a more reasonable level. The shares now trade on around 17x forward earnings, with a PEG ratio close to 1 and a dividend yield of approximately 3%. For a business delivering double-digit earnings growth, 30% plus margins and strong free cash flow, that no longer looks stretched.

Crucially, management appears to agree. Shortly after the placement, RELX announced a £350m buyback programme to be executed over just one month. This sits within the broader £2.25bn capital return plan for 2026 and represents a meaningful deployment of cash into the market at current levels.

This is an important signal. The company is effectively stepping in to absorb recent supply, reinforcing confidence in both the valuation and the long-term outlook. Combined with the strong underlying cash generation, this provides a layer of support that was not present earlier in the sell-off.

In a market driven by macro headlines, it is easy for high-quality businesses to become temporarily mispriced. RELX is not a turnaround story or a momentum play, but a steady compounder that has gone through a valuation reset. With growth continuing, margins expanding and management actively returning capital, the current weakness looks more like a period of adjustment than a deterioration in the underlying story.

Five Key Takeaways

1. Strong growth: revenue and profit continue to expand, highlighting the resilience of the underlying business model.

2. High margins: operating margins remain elevated, reflecting pricing power and a shift towards higher-value analytics.

3. Cash generation: strong cash flow supports growing dividends and significant share buybacks.

4. Temporary pressure: recent weakness appears driven by external factors rather than any deterioration in fundamentals.

5. Valuation reset: the de-rating has brought the shares back to more reasonable levels for a high-quality compounder.

RELX 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.