12th Mar 2026. 9.06am

Regency View:

BUY Ramsdens Holdings (RFX)

Regency View:

BUY Ramsdens Holdings (RFX)

A gold tailwind for a diversified compounder

Some businesses thrive when conditions are stable. Others come into their own when markets become uncertain. Ramsdens Holdings (RFX) belongs firmly in the second category. In fact, the current environment may be almost perfectly suited to the way this business is structured.

At a time when gold prices have surged to record levels and consumers remain increasingly value conscious, Ramsdens finds itself operating in a part of the market where demand can strengthen rather than weaken during periods of economic tension. That positioning is now starting to show up clearly in the numbers, with the latest trading update indicating profits for the current financial year will come in ahead of expectations.

A simple business model that works exceptionally well

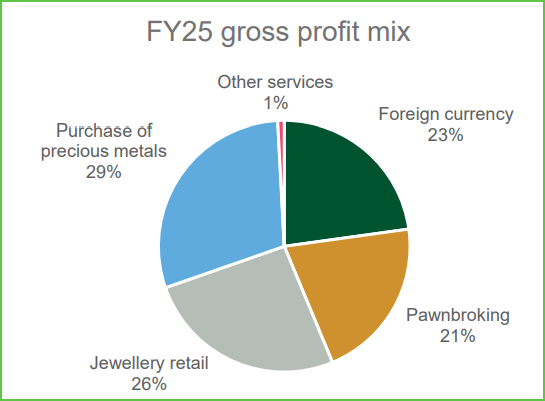

Ramsdens operates a nationwide network of retail stores that provide a range of everyday financial services. At its core, the business revolves around four primary activities: pawnbroking, foreign currency exchange, the purchase of precious metals and jewellery retail.

Pawnbroking remains one of the most important divisions. Customers can obtain short-term loans secured against valuable items such as jewellery or watches. Because these loans are backed by physical assets, the risk profile is significantly different from unsecured consumer lending. Ramsdens lends conservatively relative to the underlying value of the collateral, which allows the company to generate attractive margins while maintaining a disciplined approach to risk.

Foreign currency services provide another steady income stream. Customers purchase travel money through Ramsdens stores or increasingly through online click-and-collect orders. The company also offers a multi-currency travel card, allowing it to capture additional spending from customers travelling abroad.

Jewellery retail and the purchase of precious metals complete the model. Customers frequently sell unwanted gold jewellery directly to Ramsdens, which can either be recycled through the precious metals division or refurbished and sold through the retail network.

What makes this structure particularly effective is the way these divisions support each other. Jewellery purchased from customers becomes inventory for retail sales, while those same assets can underpin lending in the pawnbroking business. The precious metals division allows Ramsdens to monetise unwanted gold quickly, capturing value at multiple stages of the asset lifecycle rather than relying on a single transaction.

This interconnected model creates a business that is both diversified and operationally efficient.

Gold prices are creating a powerful tailwind

The latest trading update highlights just how supportive the current environment has become. Ramsdens reported that its purchase of precious metals division is performing significantly ahead of expectations as gold prices continue to climb.

The gold price has risen roughly 20% since the start of the financial year, reaching fresh record highs during 2026. This has encouraged customers to sell unwanted jewellery while also improving margins on precious metals transactions.

Higher gold prices do more than simply boost the value of scrap gold purchases. They also strengthen the collateral underpinning Ramsdens’ pawnbroking book. Because loans are secured against jewellery, rising gold prices increase the asset coverage of the lending portfolio. This allows Ramsdens to expand lending activity while maintaining conservative loan-to-value ratios.

In other words, a rising gold price improves both sides of the business at the same time

Alongside this precious metals strength, other divisions are also performing well. Pawnbroking lending reached record levels in January as customers sought short-term asset-backed loans. Jewellery retail continues to perform strongly both in-store and online, helped by the launch of a newly upgraded ecommerce platform.

Foreign currency trading has remained broadly stable, with volumes broadly flat year-on-year. The mix is gradually shifting toward lower-margin online ordering and multi-currency card usage, but the division continues to provide a reliable revenue stream.

Taken together, these trends have pushed management to upgrade expectations for the year ahead. Ramsdens now expects profit before tax for FY26 to exceed £21m, comfortably ahead of previous market forecasts.

Financial strength that stands out on AIM

One of the most appealing aspects of Ramsdens is the quality of its financial profile. For a company operating in retail and consumer finance, the balance sheet remains notably conservative.

Operating margins currently sit around 14.6%, while returns on capital exceed 24%. Those numbers place Ramsdens comfortably above many comparable AIM businesses in terms of efficiency.

Revenue has also been trending steadily higher. Sales increased from £83.8m in 2023 to £95.6m in 2024 before rising further to £116.8m in the most recent financial year. Profitability has followed a similar path, with net profit reaching £11.9m and earnings per share climbing significantly during the same period.

Cash generation remains solid, supported by the asset-backed nature of the lending book and disciplined cost control across the store network. Net debt remains minimal and liquidity remains strong, providing the company with considerable financial flexibility.

Dividend growth has been another attractive feature. Ramsdens increased its total dividend to 13.5p per share, and forecasts suggest this could rise to roughly 16p. That places the shares on a forward yield above 4% while maintaining comfortable earnings cover.

Few AIM companies combine this level of profitability, cash generation and balance sheet strength.

Store expansion provides a clear growth runway

Alongside strong trading conditions, Ramsdens continues to expand its physical footprint across the UK. Management expects to open between eight and twelve new stores during the current financial year, building on the steady growth of the estate in recent years.

New locations in Wakefield and Hull are already trading well, while the recently acquired store on the Isle of Sheppey has been refurbished and integrated into the network.

This expansion strategy has historically delivered attractive returns. Ramsdens stores require relatively modest capital investment yet can reach profitability quickly thanks to the range of services offered in each location. Pawnbroking, jewellery retail, precious metals purchases and travel money can all operate from the same premises, allowing each store to generate multiple revenue streams from a single customer base.

That combination means the store rollout provides a relatively low-risk pathway for earnings growth.

Buying the pullback

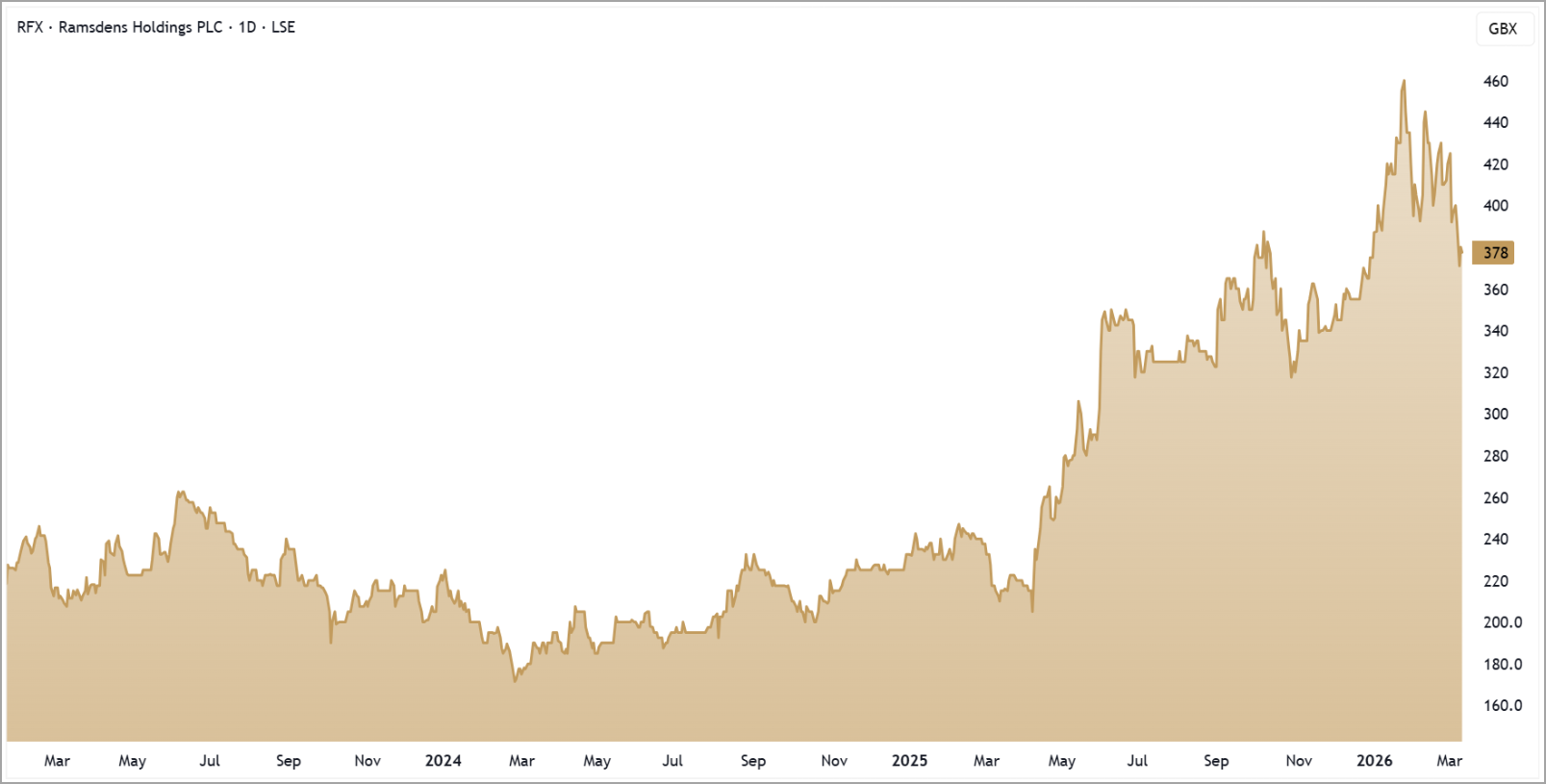

Ramsdens price action supports the improving fundamental story. Over the past year the shares have delivered a strong advance, forming a clear pattern of higher highs and higher lows as investor confidence in the business has strengthened.

More recently the shares have pulled back from their highs and are consolidating near the rising 200-day moving average. This kind of consolidation often represents a healthy pause within a longer-term uptrend rather than a reversal.

In Ramsdens’ case the latest trading update reinforces the underlying strength of the business. Rising profits, expanding store numbers and supportive commodity dynamics all suggest the broader trend remains supported by fundamentals.

Periods of consolidation after strong advances are often where long-term investors begin building positions.

For investors looking for a profitable, cash-generative small cap with exposure to supportive macro trends, Ramsdens continues to demonstrate many of the characteristics associated with steady compounders.

RFX 3-Year Chart

Five Key Takeaways

1. Diversified earnings: Ramsdens generates income from pawnbroking, precious metals purchasing, foreign currency and jewellery retail, creating a resilient multi-stream model.

2. Gold tailwind: Rising gold prices are boosting margins in the precious metals division while strengthening collateral values in the lending book.

3. High-quality financials: Operating margins above 14% and returns on capital exceeding 24% highlight the efficiency of the business.

4. Store expansion: Opening 8–12 new locations provides a clear and scalable pathway for growth.

5. Trend intact: The shares remain within a strong long-term uptrend, with recent consolidation occurring alongside improving fundamentals.

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.