20th Feb 2026. 10.52am

Weekly Briefing – Friday 20th February

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | +2.39% |

| FTSE 250 | +1.10% |

| FTSE All-Share | +2.23% |

| AIM 100 | +0.45% |

| AIM All-Share | +0.34% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 20th February

Market Overview

Dear Investor,

Two of the market’s mining heavyweights reported this week, and together Antofagasta and BHP offered a useful snapshot of where we are in the cycle. Strip away the headlines and what stands out is not exuberance, but discipline. Strong pricing is doing the heavy lifting, yes, but so too is operational control and increasingly selective capital allocation.

Antofagasta’s results were punchy. Revenues jumped, profits more than doubled at the underlying level, and margins widened to levels most producers would envy. Yes, higher copper prices helped, but this was not simply a rising tide lifting all boats. Costs were held in check, by-product credits did their job, and despite peak capital expenditure on major growth projects, the balance sheet remains comfortable. Management is investing heavily today to lift production meaningfully over the next few years, while still sticking to a clear dividend policy.

BHP, operating on a different scale, told a similar story. Copper has become the dominant earnings engine, which is exactly where BHP wants to be given the structural demand story. Cash flow was strong, margins held up well, and the group moved proactively to unlock value through its silver streaming deal. In plain English, it has monetised a non core by-product to free up billions in cash without increasing debt. That is active capital management rather than sitting back and hoping prices do the work.

So where are we in the cycle? Copper prices have been firm, supported by electrification, grid investment and the steady drumbeat of energy transition demand. But what stands out to me is the behaviour of management teams. There is investment, yes, but it is targeted. There are dividends, but they are covered. Balance sheets are being protected, not stretched. That does not feel like late cycle excess.

Is this a mining super cycle? It is too early to hang that label on it. What we are seeing right now looks more like a disciplined upswing. Prices are supportive, demand trends are credible, and the majors are behaving like adults. For long term investors, that is often a healthier foundation than a frenzy.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: BAE Systems (LSE:BA.) +8.7% on the week

BAE Systems jumped to highs this week after reporting a solid set of full year numbers. Sales rose 10% year on year, slightly shy of consensus expectations, but adjusted operating profit edged ahead of forecasts. The more important detail was the continued strength in demand, with the order backlog climbing to a record £83.6 billion, underlining the visibility built into the business.

That backlog reflects a steady stream of contract wins across key markets. Increased defence spending across NATO continues to provide a powerful tailwind, while recent awards such as the UK Türkiye Typhoon aircraft agreement and a US Space Force missile tracking contract reinforce BAE’s positioning in critical long term programmes. In an uncertain geopolitical environment, demand for defence capability is not proving cyclical.

Looking ahead, management guided to further growth in 2026, with sales expected to rise by 7% to 9% and underlying profit forecast to increase by 9% to 11%. Free cash flow guidance for the 2024 to 2026 period has also been upgraded to exceed £6 billion. In short, the company is not just growing, it is converting that growth into cash.

Regency View: BAE remains one of our preferred holdings in the FTSE Investor portfolio. Strong order visibility, rising cash generation and structural defence spending support continue to make this a core long term position.

Pinewood’s shares came under heavy pressure this week after private equity firm Apax formally withdrew its potential offer for the company, citing challenging market conditions. The stock fell sharply on the news, with investors quickly repricing the business once the prospect of a takeover premium disappeared. In markets like this, when a bidder walks away, the reaction is rarely gentle.

The company moved to steady nerves, reiterating confidence in its long term prospects and pointing to its position as a mission critical software provider to automotive retailers and OEMs. Management highlighted its AI capabilities, North American expansion and a significant contract win with Lithia that is expected to build meaningful revenue over the next few years. Medium term guidance remains intact, with a target of underlying earnings of £58 to £62 million by 2028.

That said, the numbers today still reflect a business in transition. Earnings have been volatile, return metrics remain modest and the valuation, even after the fall, still assumes a good deal of future delivery. With the takeover angle removed, the focus shifts squarely back to execution and whether the growth strategy can translate into consistent profitability.

Regency View: When a bid disappears, so does the safety net. Pinewood now needs to prove that its AI and North American expansion story can deliver hard earnings growth rather than just long term ambition.

Sector Snapshot

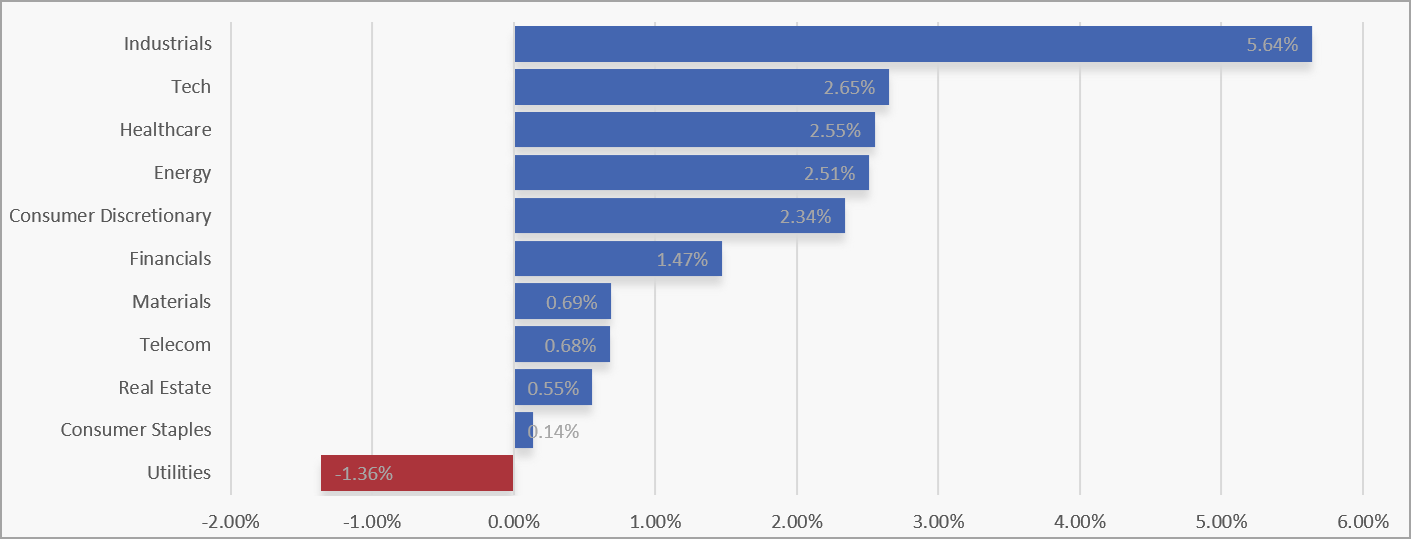

Industrials led the market this week, with Tech, Healthcare and Energy also posting solid gains, marking a clear shift back towards cyclical and growth-sensitive areas. Consumer Discretionary and Financials added to the upside, suggesting a broader improvement in risk appetite after recent defensive leadership.

Further down the table, Materials, Telecom and Real Estate made more modest progress, while Consumer Staples were little changed. Utilities were the only sector to slip, standing out as investors rotated away from defensives and back towards areas more closely tied to economic momentum.

UK Sector Performance (7-Days)

UK Price Action

It has been another solidly bullish week for the FTSE, with the market pushing to fresh highs and then consolidating close to them. That kind of behaviour is exactly what you want to see in a strong trend, with price holding its ground rather than showing any signs of rejection or exhaustion.

What stands out on the chart is the developing fan of rising trendlines, which underlines how momentum is continuing to build rather than fade. As long as pullbacks remain shallow and contained within this structure, the path of least resistance remains higher and the broader uptrend stays firmly in control.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.