4th Feb 2026. 9.00am

Regency View:

Wise (WISE) Second Tranche

- Growth

Regency View:

Wise (WISE) Second Tranche

When execution earns a second bite

Wise (WISE) is not a new idea for us. We first backed the shares last year on the basis that the business was building something structurally valuable in global payments, even if near-term sentiment was moving the other way. That patience has been tested, with the shares spending much of the past year in consolidation rather than celebration.

What has changed is not the narrative, but the evidence. Recent trading has provided clearer confirmation that Wise’s strategy is translating into sustained growth, improving mix, and resilient profitability. Rather than chasing a bounce, this second tranche is about responding to execution and increasing confidence in the long-term trajectory.

A business that is quietly strengthening

Wise’s January trading update was one of its strongest in some time, not because of a single headline number, but because of the breadth and balance of progress across the platform.

Quarterly cross-border volumes grew 25% year-on-year to £47.4bn, with active customers rising 20% to nearly 11 million. That alone would be healthy. More encouraging is what is happening beneath the surface. Customer holdings rose 34% to £27.5bn, reflecting deeper engagement with the Wise account rather than one-off transactional use.

This matters because it changes the quality of revenue. Card and other revenue grew 30%, Wise Business customers increased 25%, and business volumes jumped 37%. The platform is becoming more embedded in day-to-day financial activity, which improves predictability and long-term monetisation.

The take rate eased slightly to 52bps, but this is best viewed as a strategic choice, not a competitive problem. Management are consciously reinvesting pricing into growth and infrastructure while still delivering strong income growth.

Margins holding up better than expected

Underlying income rose 21% year-on-year in the quarter, keeping Wise firmly within its 15–20% full-year growth guidance. More importantly, management now expect underlying profit before tax margins to land towards the top end of the 13–16% target range for FY26, even after absorbing dual-listing costs.

That combination of sustained growth and resilient margins is not common in global fintech. It speaks to a platform that is scaling efficiently rather than burning capital to defend share.

Returns remain strong, with operating margins above 30%, return on capital around 30%, and free cash flow conversion running well ahead of earnings. Wise continues to operate with substantial net cash, giving it strategic flexibility without balance sheet risk.

Valuation still reflects caution

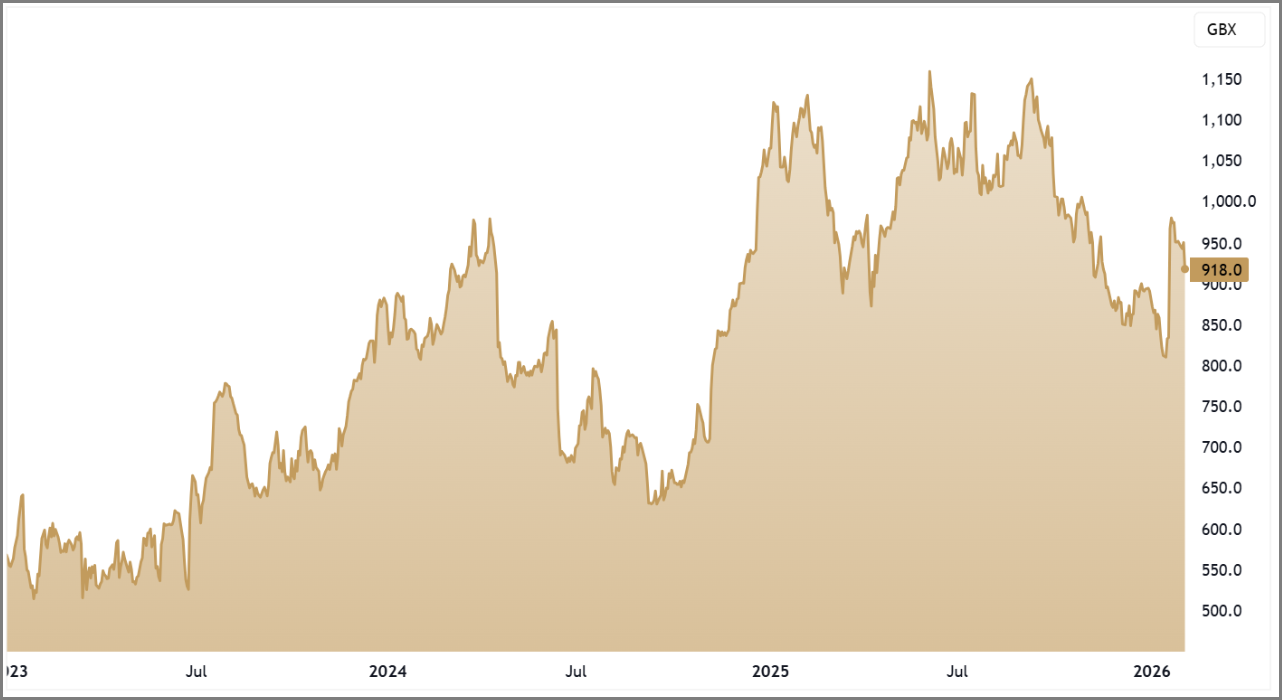

At around 25x forward earnings, Wise is not a bargain in traditional value terms. However, valuation needs to be viewed in context. The shares remain more than 20% below their 52-week high and have already absorbed a significant derating from earlier optimism.

Free cash flow generation remains robust, with a price-to-free-cash-flow multiple close to 2x on trailing numbers reflecting the capital-light nature of the model. The market is still pricing Wise as a business facing structural uncertainty, despite growing evidence that execution is improving.

Consensus forecasts imply mid-single-digit EPS growth in the near term, but that largely reflects reinvestment rather than demand weakness. If growth continues to compound at the platform level, earnings leverage should re-emerge.

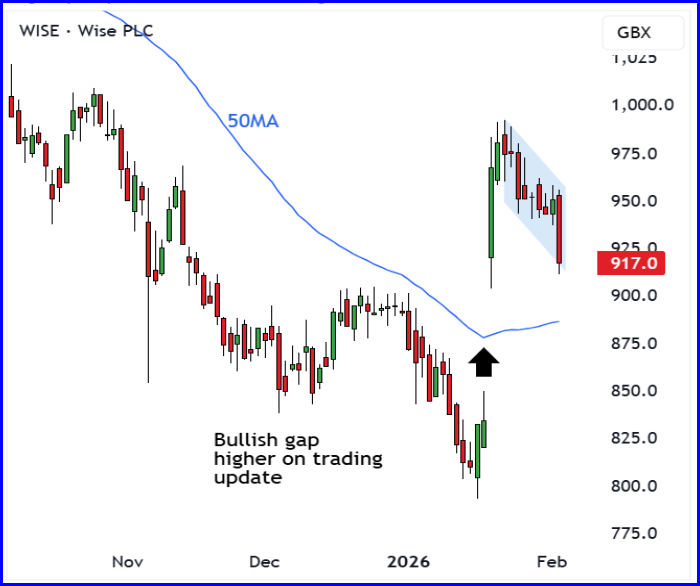

Price action is starting to align

From a technical perspective, Wise’s price action has quietly improved. Following the January update, the shares gapped higher and have since consolidated in a small descending channel or flag formation. That pattern suggests acceptance of higher prices, not exhaustion.

While the longer-term trend is still in recovery mode, the stock is now holding above its shorter-term averages and stabilising relative to the broader market. This is consistent with institutions building positions gradually rather than trading around results.

This second tranche is therefore not about buying strength blindly. It is about responding to improving fundamentals and early signs of sentiment stabilisation.

Why add now

Adding a second tranche at this stage improves exposure to a business where risk has reduced, but upside remains intact. Wise is still executing against a large global opportunity, with growing customer engagement, disciplined margins and strong cash generation.

The original investment case remains valid. What has changed is the level of evidence supporting it.

This is a growth-led quality play, not an income stock and not a short-term trade. Position sizing remains important, but we believe the balance of risk and reward now justifies increasing exposure.

Five Key Takeaways

1. Operational confirmation: Strong volume, customer and income growth reinforce confidence in execution.

2. Deeper engagement: Customer holdings and non-transfer revenue are growing rapidly, improving revenue quality.

3. Margin discipline: Profitability is holding up better than expected despite continued reinvestment.

4. Valuation reset absorbed: Shares still reflect caution, even as fundamentals strengthen.

5. Measured add: This second tranche responds to confirmation, not momentum chasing.

WISE 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.