10th Dec 2025. 8.58am

Regency View:

BUY Persimmon (PSN)

- Value

- Income

Regency View:

BUY Persimmon (PSN)

The quality way to play a housing recovery

There is a moment in every cycle where the market feels gloomy but reality is already improving quietly in the background. UK housebuilders have lived through a rough patch with higher mortgage rates, wobbly consumer confidence and no shortage of gloomy headlines. Yet beneath that surface, the recovery seeds are being planted. Sales rates are rising, pricing is stable and land pipelines are expanding. The share prices just have not caught up yet.

This is usually where opportunity lives. It is tempting to wait until everyone feels cheerful again. The problem is by that point the best gains have normally already been made. Persimmon (PSN) looks like one of those names where sentiment has lagged the facts on the ground. And if the UK housing market continues to gradually thaw, this is the builder best placed to warm up fastest.

Choosing quality over a bargain-bin bet

We looked closely at Taylor Wimpey as well. TW does catch the eye. A 9% plus dividend yield and a share price that looks like it is searching for a basement will always grab attention. But there is a difference between cheap and good value. Taylor Wimpey’s margins have shrunk considerably, dividend cover is thin, and the share price trend has been firmly south for the last six months. That makes the investment case more of a timing call and a hope for a sharp sentiment flip.

Persimmon, in contrast, is already proving it can grow through the tougher part of the cycle. Sales rates are up. Forward orders are up. Outlet numbers are up. Pricing is holding. And its balance sheet gives management the flexibility to keep improving the platform rather than waiting for conditions to improve. Yes, the dividend yield is lower at just under 5%, but it is comfortably covered by earnings. Reliability beats drama.

Execution that speaks louder than headlines

Let’s start with the numbers that matter right now. Forward sales are up 15% year on year at £2.79bn. Private forward sales are also 15% higher at £2.09bn. Average selling prices in the forward book have grown to around £295k, up 1.5% despite affordability challenges. Total weekly sales are up 14% compared to a year ago.

These are not the stats of a business sitting still in a downturn. Persimmon has been opening new developments rather than closing them. Sixteen new sites recently joined the pipeline and the Charles Church premium brand is gaining traction after its relaunch. The strategy to broaden the offering while maintaining value remains intact and visibly effective.

Affordability remains a hurdle across the industry, but the company has responded proactively with shared equity products to open the door for more buyers. This is the sort of practical, impact-first execution that builds trust and keeps volumes moving even in softer markets.

Proof of value starting to show in the chart

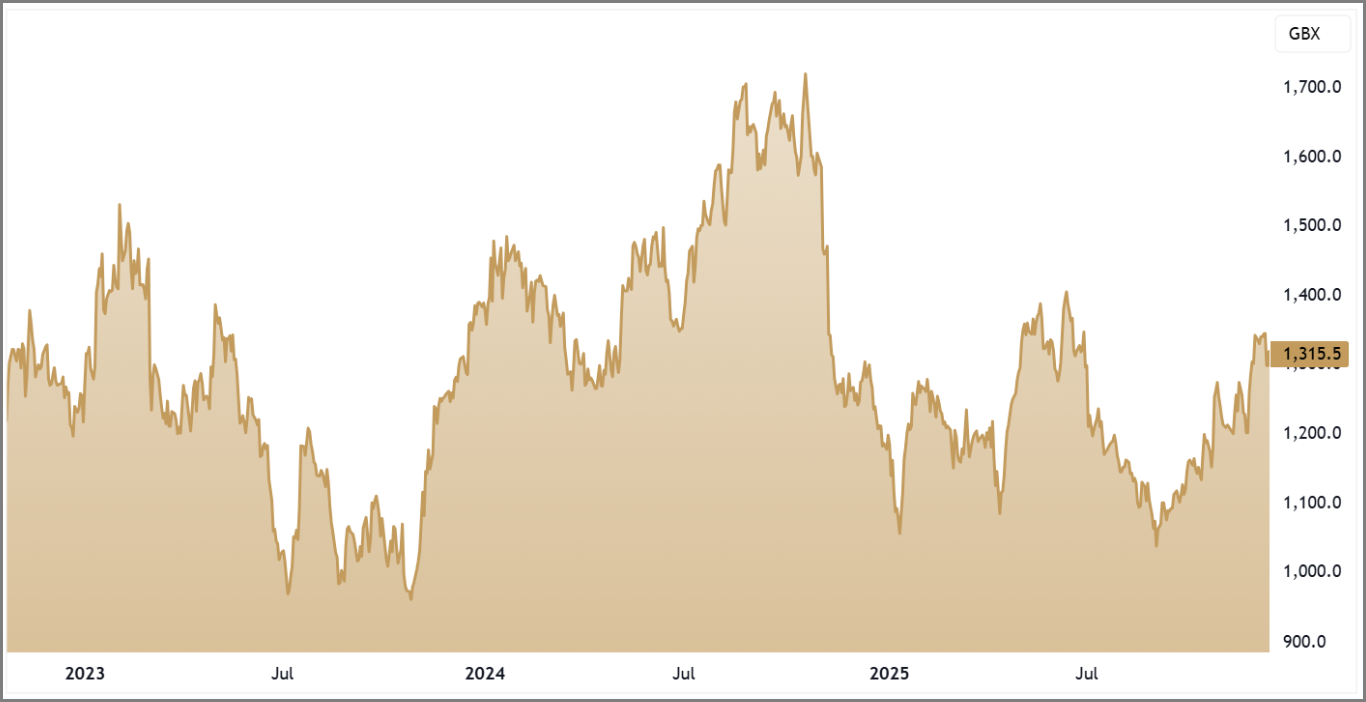

Markets tend to react late, but they do react. Over the last three months Persimmon shares have climbed more than 14%, helped along by investors spotting that the business is outperforming gloomy expectations. The shares now trade above both their 50 day and 200 day moving averages. Those are the kind of technical signals that often mark the start of a more meaningful rerating.

There is still work to do. The shares remain around 8% below their 52 week high, which gives buyers a margin of safety and room to benefit as sentiment continues to recover. There is also solid support around the 1200p to 1250p levels where past consolidation has occurred. If the price holds that area during market choppiness, it could act as the springboard for the next leg higher.

Technical traders often say downtrends end with disbelief. The recent shift in momentum suggests disbelief is fading.

Financial strength that supports patience

The market has spent a year worrying about affordability and mortgage rates. Persimmon has spent that same year protecting margins, investing in land and keeping its balance sheet clean. It has a net cash position of around £123m. Gearing is low. That means no stress if recovery takes a little longer and no desperate need to chase volume with aggressive discounts.

Operating margins remain above 11% and return on capital is approaching 10%. These numbers are already respectable for a cyclical sector operating in second gear. As volumes improve, those returns should naturally strengthen. At around 12.5 times forward earnings and roughly 1.2 times book value, the shares still reflect caution more than optimism.

Income investors can relax too. The dividend yield near 5% is well covered by earnings more than 1.3 times. It rewards patience while the fundamentals continue to turn.

A sensible way to lean into the recovery

The danger with cyclical investing is feeling the need to catch the exact turning point. That is a stressful and often costly game. Persimmon removes much of that pressure. It is already performing well in a tougher environment, it has strengthened its competitive position and the business is aligned with the parts of the housing market that will recover first.

Over the next 12 to 24 months three forces are likely to play into its hands. Mortgage affordability improves even modestly. Political uncertainty fades. The chronic supply shortage becomes harder to ignore. When that combination arrives, demand typically responds quicker than expected.

Persimmon is not promising fireworks. It is promising progress. And at this point in the cycle that is exactly what investors should want. With a solid dividend, improving momentum and a valuation that still leaves room for upside, this is a measured and intelligent way to gain exposure to UK housing.

If there is one housebuilder built to benefit from the next phase of the cycle without requiring heroics on timing, it is Persimmon. Quality eventually gets recognised. Here, it is already starting.

Five Key Takeaways

1. Higher quality play: Persimmon is already growing volumes and protecting pricing through the downturn which sets it apart from peers relying on a bounce.

2. Value with support: A forward PE of around 12.5 and price to book near 1.2 suggest a valuation still anchored in caution rather than recovery.

3. Financial strength: A net cash position and secure dividend coverage provide stability and allow continued investment without stress.

4. Positive shift in sentiment: Shares have moved above key moving averages and recent gains signal investors are beginning to reprice the outlook.

5. Sensible exposure to the cycle: A near 5% yield offers income while higher margins and volumes emerge over the next 12 to 24 months.

PSN 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.