28th Nov 2025. 10.47am

Weekly Briefing – Friday 28th November

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | +1.81% |

| FTSE 250 | +3.45% |

| FTSE All-Share | +2.01% |

| AIM 100 | +2.80% |

| AIM All-Share | +2.22% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 28th November

Market Overview

Dear Investor,

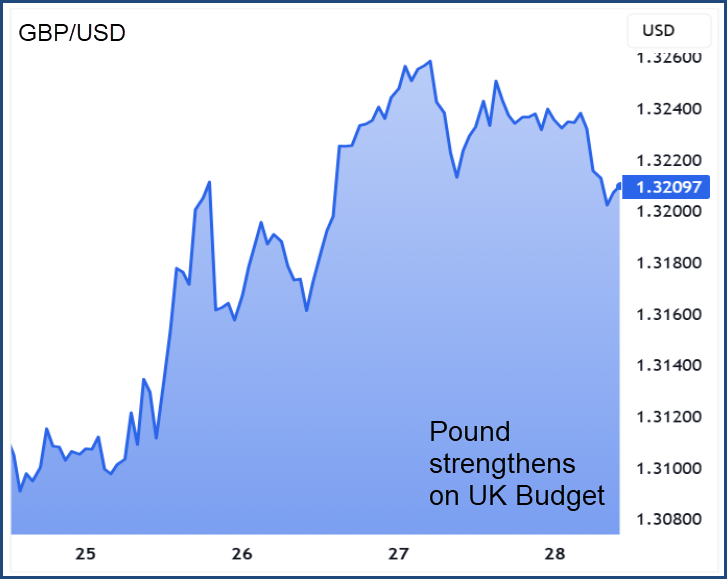

Rachel Reeves will have breathed a sigh of relief this week as her Budget came and went without a market meltdown. The FTSE 100 ticked higher, the FTSE 250 followed and sterling firmed against both the dollar and the euro. After several weeks of wobble and rising tension the absence of fresh turmoil was enough to steady nerves. Markets did not celebrate but they stopped flinching and in the current climate that counts as progress.

The lead up to this Budget has been anything but calm. Expectations have been scattered and confidence has been low with political noise adding uncertainty that investors dislike. Investors have been wrestling with mixed signals ranging from stalled growth and a softer inflation backdrop to doubts about how much fiscal room the chancellor really has. Sterling option markets told the story clearly as demand for downside protection picked up in the days before the announcement. This was a market preparing for volatility not because it expected a shock on the day but because the build up had been disorderly.

Against that backdrop the Budget itself leaned heavily on revenue raising. Reeves outlined £26bn additional taxation aimed mainly at higher earners and areas of perceived under taxation in pensions property and savings. The Office for Budget Responsibility (OBR) said the measures were not large enough to change its potential growth forecast which underlined the view that this was a stabilising rather than growth focused Budget. Policy continues to move towards building fiscal headroom rather than stimulating activity.

Businesses have been slow to hide their disappointment. Retailers, hospitality groups and service led industries face higher costs from the minimum wage increase and tighter employment rules. The business rates settlement left many smaller firms frustrated as expected relief failed to materialise and some now face significantly higher bills next year. Households also remain under pressure with the continued freeze on income tax thresholds dragging more people into higher bands even as real incomes struggle to improve.

One sector that felt an immediate sense of relief was the banking industry. The long rumoured levy on interest earned from Bank of England reserves did not appear and bank stocks stabilised as a result. Major lenders responded by announcing new commitments to support business lending and mortgage affordability. For investors it was a reminder that in a Budget built on raising revenue, sometimes the most important outcome is what the chancellor chooses not to do.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Lloyds (LSE:LLOY) +9.8% on the week

Lloyds and other UK based banks were given a boost this week after the Budget confirmed that the sector would not face new taxes. The OBR’s documentation contained no reference to a levy on interest earned from reserves at the Bank of England, removing the main source of speculation that had weighed on the industry in recent months.

The share price reaction reflected a continuation of recent momentum. Performance over 1 month, 3 months and 1 year has remained positive, and the stock continues to trade above its 50 day and 200 day moving averages. Trading volumes have also been running above the 10 day trend when compared with the 3 month average.

Forecast data for the bank remains stable. Market analysts expect earnings growth above 30% in the year ahead, with the shares trading on a forward price to earnings ratio of 9.9. Consensus projections also point to a dividend yield above 4%.

REGENCY VIEW: Lloyds has finally been given the clarity it needed. With political noise fading the bank can get back to lending discipline and capital returns rather than watching for new fiscal surprises.

Tullow slipped again despite releasing a detailed November update. Production to the end of October averaged just over 40,000 barrels of oil equivalent per day and remained within guidance although field decline continues to weigh on volumes.

Operational activity in Ghana is picking up. Jubilee performance has been held back by earlier issues but new wells are contributing and drilling has restarted. TEN production has been ahead of expectations and new seismic data is helping to refine future well planning.

The financial backdrop remains demanding. Asset sales in Kenya and Gabon have provided more than $400m in proceeds but net debt is still around $1.2bn. Tullow is in active discussions with creditors ahead of the May 2026 bond maturity and continues to work through a large receivables backlog from the Government of Ghana.

REGENCY VIEW: Operational improvements are encouraging but the balance sheet still dominates the story. Until refinancing progress becomes clearer the market is likely to stay cautious no matter how well the underlying assets perform.

Sector Snapshot

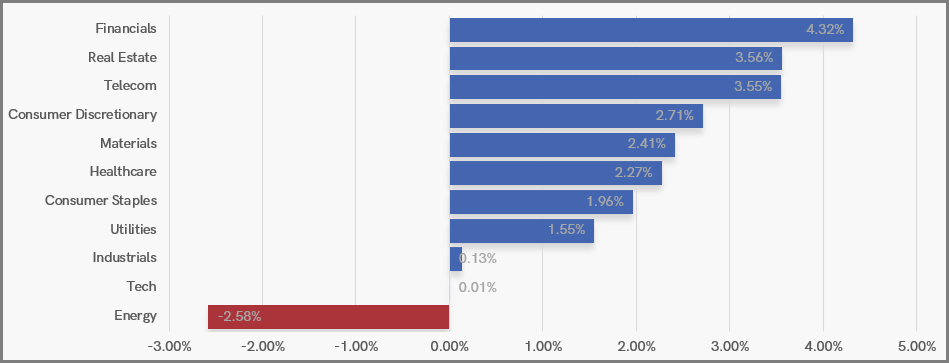

Financials surged to the top of the rankings this week, helping to drive a broad recovery across most sectors. Real Estate and Telecom followed closely behind, while Consumer Discretionary, Materials and Healthcare all posted strong gains, signalling a clear improvement in risk appetite.

Consumer Staples and Utilities also advanced, adding a layer of defensive support, while Industrials and Tech were little changed. Energy was the lone laggard, slipping back after its recent strength, as investors rotated toward sectors more leveraged to growth and sentiment.

UK Sector Performance (7-Days)

UK Price Action

The FTSE found its footing this week as prices rotated higher from the 50-day moving average. This is classic behaviour for an established uptrend, with buyers stepping in at dynamic support to steady the market.

There are, however, signs to be cautious. The recovery has so far shown less momentum than the recent sell off, which raises the possibility that the current bounce is a pullback rather than the start of a fresh leg higher. If momentum stalls beneath the mid-November swing highs, the market may be setting up for a second leg lower before the broader trend can reassert itself.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.