19th Nov 2025. 8.59am

Regency View:

Update

Regency View:

Update

It’s been a mixed bag this week as we approach the end of earnings season…

Aviva impressed with upgraded targets, 4imprint jumped on stronger than expected profitability, 3i dipped despite an excellent set of numbers, and ITV surged after confirming talks over a major divisional sale.

Aviva raises the bar as integration momentum builds

Aviva (AV.) delivered one of its most confident trading updates in years, telling the market it now expects to hit its 2026 financial targets a full year early. Operating profit is set to reach around £2.2bn in 2025, helped by strong general insurance premium growth and robust flows across wealth and workplace pensions. Management also lifted its medium-term ambitions, targeting 11% operating EPS growth between 2025 and 2028 and IFRS return on equity above 20% by 2028.

The Direct Line acquisition is already proving more accretive than planned. Expected cost synergies have been raised to £225m, almost double the original figure, while capital synergies of more than £500m are now quantified. Pricing discipline, better underwriting and improved weather impacts helped the combined operating ratio drop to 94.4%, with a discounted measure of 90.4%. Liquidity remains strong at £2.2bn and the solvency ratio of 177% leaves the door open for resumed buybacks next year.

For investors, the message is one of accelerating momentum. Aviva’s pivot towards capital-light products is beginning to reshape its earnings quality and the upgraded synergy guidance suggests further upside to group returns. The tone of the update was unequivocally confident and the company appears well positioned to surprise positively again in early 2026.

AV. Daily Candle Chart

Market applauds 4imprint’s resilience

A sharp move higher in 4imprint (FOUR) reflected the market’s relief that trading has held up better than feared in a challenging promotional products environment. Full year revenue is now expected to be at least $1.32bn, which sits at the top of analyst forecasts, while profit before tax of not less than $142m is above the upper end of expectations. The shares responded immediately, rallying as investors recalibrated their view of the group’s earnings power.

Despite order intake running around 3% below last year, margins have remained strong with gross profit just under 33% and a double-digit operating margin maintained throughout the period. Retention from existing customers has stayed high and cash generation remains a standout feature, with the group ending October on a cash balance of $124m. That financial strength has allowed the board to approve around $10m of investment to consolidate its Wisconsin operations.

The steady performance again highlights 4imprint’s disciplined marketing model and strong customer economics. In a softer macro environment, the company continues to show it can defend margin, manage costs and sustain cash growth. The market reaction confirms that investors are willing to pay up for visibility and execution.

FOUR Daily Candle Chart

Strong results but a softer share price for 3i

3i Group (III) reported another excellent set of half year numbers including a £3.3bn total return, a 13% uplift on opening shareholders’ funds, and growth in NAV per share to 2,857p. Flagship holding Action delivered outstanding trading, with net sales up to €11.2bn and like for like growth of 6.3%, supporting a valuation uplift of more than £2.1bn. New realisations such as MPM and MAIT added £542m of proceeds, while the infrastructure portfolio also delivered strong gains.

Despite this, the shares traded lower on the results, with some investors concerned about the pace of capital deployment and the impact of recent market volatility. While liquidity is healthy at £1.6bn and gearing remains low at 3%, management was careful to highlight a cautious stance on new investments given macro uncertainty. That note of restraint, combined with a year of exceptional gains, likely contributed to the muted market reaction.

For long-term holders, the fundamentals remain unchanged. Action continues to compound at an exceptional rate and the wider portfolio is in strong shape. However, after a long run of outperformance and a rich valuation, expectations were high and the market used the update as an opportunity to rebalance exposure.

III Daily Candle Chart

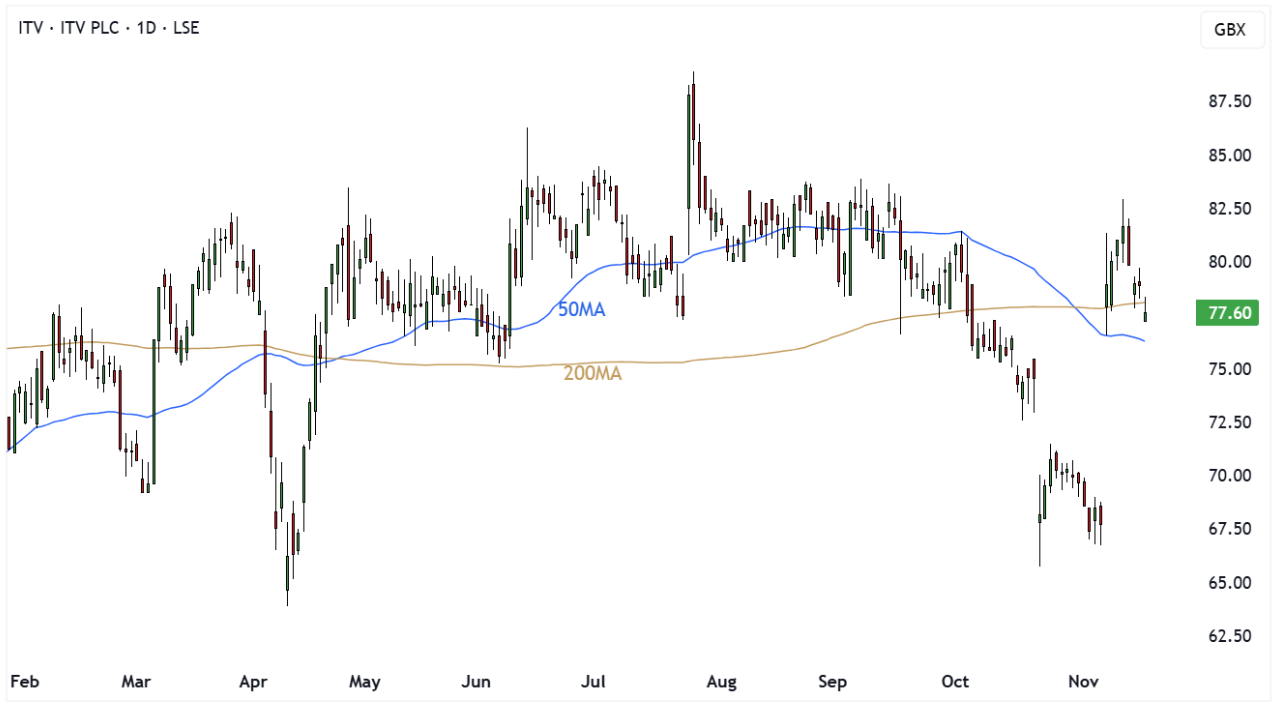

ITV lifts as a major sale comes into view

ITV (ITV) enjoyed one of its strongest trading days of the year after confirming it is in early discussions with Sky over a potential £1.6bn sale of its media and entertainment division. While talks are still preliminary, the confirmation of negotiations validated press speculation and ignited hopes of a transformational transaction that could reshape the group’s balance sheet and strategic focus.

A divestment of this scale would give ITV considerable financial flexibility and could allow management to double down on ITV Studios, the faster-growing production arm that increasingly defines the company’s value proposition. Investors were quick to price in the optionality, sending the shares sharply higher on the day of the announcement. Even though there is no guarantee a deal will be secured, the strategic logic is clear.

The strong market response shows just how much value investors believe sits within the business when assets are separated and valued independently. If ITV can secure terms that reflect the £1.6bn mooted valuation, the company would enter 2026 with a stronger balance sheet, a sharper focus and a far more compelling equity story. Let me know if you would like a punchier intro line or any tweaks to tone or emphasis.

ITV Daily Candle Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.