14th Nov 2025. 10.48am

Weekly Briefing – Friday 14th November

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | -0.10% |

| FTSE 250 | -0.26% |

| FTSE All-Share | -0.11% |

| AIM 100 | -0.76% |

| AIM All-Share | -0.64% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 14th November

Market Overview

Dear Investor,

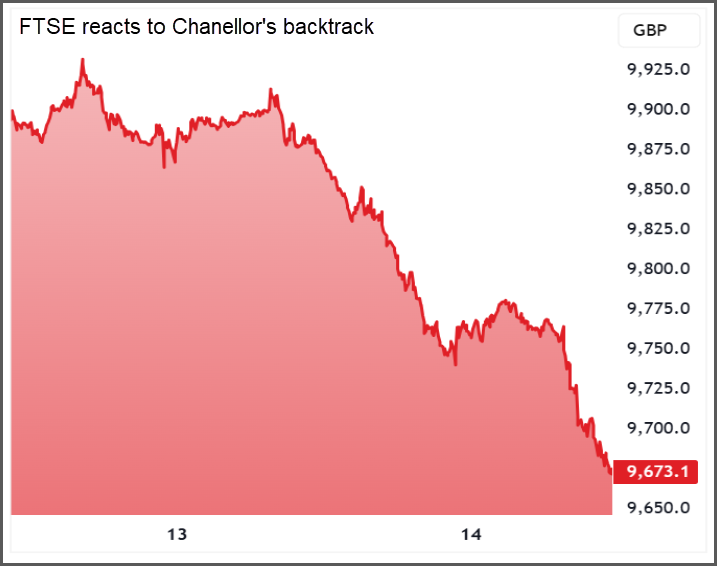

This week has put the health of the UK economy under the spotlight, and markets have responded with unease. Fresh data showing a 0.1% contraction in GDP for September reignited concerns about slowing growth just as the government’s fiscal plans came into question. The weakness was partly linked to a cyberattack at Jaguar Land Rover, but it also pointed to a broader loss of momentum. By Thursday, attention had shifted to Westminster, where reports that the government had abandoned plans to raise income tax rates triggered a sharp market sell-off.

The reaction was immediate. Gilt yields jumped to 4.54% before easing slightly to 4.49%, while the pound slipped 0.2% against the dollar and hit a two-year low against the euro. Investors saw the move as politically driven rather than economically strategic, raising doubts about the government’s appetite to tackle the deficit. The decision to back away from income tax rises has been described as a blow to fiscal credibility, with potential alternatives such as stamp duty or electric vehicle taxes viewed as less reliable revenue sources.

The Treasury moved quickly to contain the fallout, assuring investors that Rachel Reeves still intends to keep a £15 billion fiscal buffer after an improved outlook from the Office for Budget Responsibility narrowed the expected shortfall from £30 billion to nearer £20 billion. Those reassurances helped steady gilt markets by Friday, but sentiment remains cautious. The episode underscored how fragile confidence has become and how sensitive investors are to even small shifts in fiscal tone.

For investors, it was a week where weak data met political drama. The chances of a December rate cut have increased as growth cools and market nerves tighten, yet all eyes are now on the Budget. The question is no longer whether the government can balance the books, but whether it can restore belief that Britain’s economic story is still heading in the right direction.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise

SSE (LSE:SSE) +19.1% on the week

SSE shares climbed this week after the group unveiled a transformational £33 billion five-year investment plan alongside its half-year results. The move will triple spending and strengthen SSE’s position at the centre of Britain’s energy transition, with about 80% of capital directed towards regulated UK electricity networks and the remainder focused on renewables and flexible generation. Management expects the plan to lift earnings by around 50% by 2030 and expand the regulated asset base from £14 billion to roughly £40 billion by the end of the decade.

The latest results were steady and in line with expectations. Adjusted operating profit fell 24% to £655 million, reflecting typical seasonal trends and lower renewable output, while the regulated networks division delivered robust growth thanks to rising investment in SSEN Transmission. Capital spending increased 22% to £1.6 billion and net debt rose to £11.4 billion as the group accelerated work on key grid projects. An interim dividend of 21.4 pence was declared, one third of last year’s full-year payout.

Chief Executive Martin Pibworth described the investment programme as a once-in-a-generation opportunity to modernise the UK’s electricity system and support thousands of jobs. The plan will be financed through cash flow, debt, asset sales and a £2 billion equity placing, with management maintaining a disciplined balance sheet and reaffirming full-year guidance. Capital expenditure is expected to exceed £3 billion this year as major transmission and offshore wind projects gather momentum.

REGENCY VIEW:

SSE is shifting from dependable utility to growth-driven infrastructure leader. The near-term numbers may be muted, but the £33 billion plan puts a strong current behind the long-term investment case.

Shares in The Works slipped this week after the retailer reported a small dip in half-year sales and ongoing challenges in its online business. Total sales for the 26 weeks to 2 November came in at £123.8 million, down 0.3% on last year, though store like-for-likes rose 4% thanks to better marketing, new product ranges and improvements in store operations. The strong in-store performance wasn’t enough to offset a 36% collapse in online sales, which now account for less than a tenth of total revenue, following problems with a new third-party fulfilment partner.

Despite the digital disruption, management struck an upbeat tone. Gross margins improved by 300 basis points, supported by better sourcing and cost control, while progress on a £2 million cost-saving plan helped cushion inflationary pressures. Net debt improved to £5.3 million from £8.5 million a year earlier, reflecting careful stock management ahead of the crucial Christmas period. Chief Executive Gavin Peck said the company remains on track to deliver full-year profit in line with expectations, targeting pre-IFRS 16 adjusted EBITDA of around £11 million.

Even so, investors are clearly wary of the near-term headwinds. While The Works continues to carve out a niche with its family-friendly, screen-free product range, the ongoing logistics issues risk dulling momentum through the vital festive quarter. With consumer confidence still subdued and online operations under repair, the market wants to see smoother execution before sentiment recovers.

REGENCY VIEW:

The Works is doing plenty right in its stores, but the online disruption has stolen the spotlight. For now, it’s less a question of what customers want and more about whether the company can get it to them fast enough.

Sector Snapshot

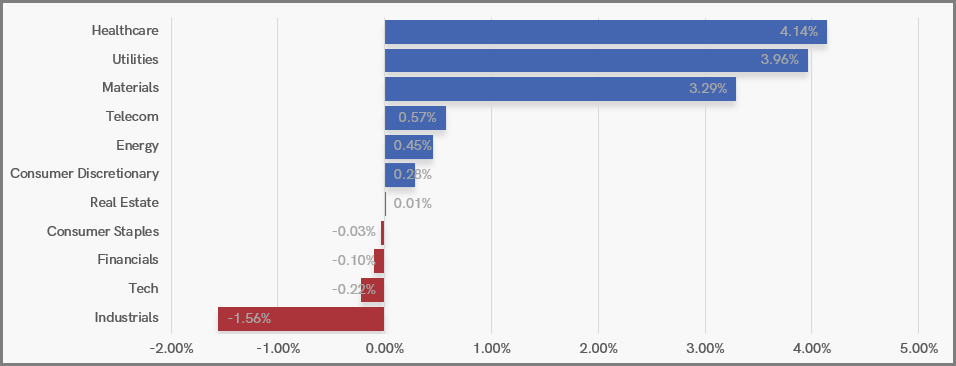

Healthcare and Utilities took centre stage this week, driving a clear defensive rebound as investors gravitated back toward sectors offering earnings stability and predictable cash flow. Materials also posted strong gains, extending its recovery on the back of firmer commodity sentiment, while Telecom and Energy added modest support.

At the softer end, Industrials saw the sharpest pullback, while Tech and Financials also edged lower after recent gains. Real Estate and Consumer sectors were largely flat, suggesting that investors were taking a more selective approach and favouring reliability over risk.

UK Sector Performance (7-Days)

UK Price Action

At the time of writing, the FTSE has completely erased its gains for the week. After breaking to new trend highs on Monday and extending those gains on Tuesday, prices have fallen sharply through Thursday and Friday, unwinding the early optimism.

Should the market close within the lower half of today’s range, it would confirm a bearish reversal week, signalling that short-term momentum has shifted and that a deeper pullback may be underway. The 9,580 level, which acted as previous resistance, will now be watched closely to see if it can hold as support in the days ahead.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.