1st Aug 2025. 9.30am

Weekly Briefing – Friday 1st August

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | -0.62% |

| FTSE 250 | -1.35% |

| FTSE All-Share | -0.71% |

| AIM 100 | -2.86% |

| AIM All-Share | -2.25% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 1st August

Market Overview

Dear Investor,

This week saw earnings from two of the FTSE’s heavyweights in two of its most important sectors, Asian banking powerhouse HSBC and global mining giant Rio Tinto. Both delivered results that missed forecasts, but beneath the headlines there were some important signals about how each business is positioned for the road ahead. While the short-term numbers gave markets reason to flinch, we think the longer-term narratives remain intact.

HSBC’s 29% drop in pre-tax profit wasn’t pretty, dragged down by a hefty $2.1 billion impairment on its stake in China’s Bank of Communications and a rise in restructuring costs. But this isn’t the start of a downward spiral. The bank is mid-way through a major strategic reset under new leadership, and despite the noise, UK revenues rose 7% quarter on quarter. Wealth and premier banking stood out as a bright spot, growing 19% in the first half, and we think the expansion of this segment will be a key driver of margin resilience over time.

We recommended HSBC to clients during a period when sentiment was low and valuation looked completely detached from fundamentals. Since then, the shares have moved nicely higher, and we remain confident that Elhedery’s simplification strategy, combined with the group’s capital strength, leaves the bank well placed to weather short-term bumps. Risks from China and global rates are real, but they’re priced in. What’s not fully appreciated yet is how a leaner, better-aligned HSBC could deliver stronger returns in a more stable macro environment.

As for Rio Tinto, its results marked a five-year low in earnings, with a 16% drop in underlying profits driven by softer iron ore prices and operational disruption from cyclones. But the story isn’t all about iron ore anymore. Copper and aluminium are starting to play a more meaningful role, and Rio’s recent move into lithium looks well timed as demand from electric vehicles and battery storage begins to rebound. The dividend was cut, which disappointed the market, but the balance sheet remains strong and the growth pipeline is far from empty.

Looking ahead, both companies are entering new chapters. HSBC is reshaping itself to become a more focused, profitable lender with a growing foothold in wealth. Rio is shifting gears under new leadership and expanding into metals of the future. Neither journey will be without setbacks, but both stocks remain well supported by strong fundamentals and compelling long-term themes.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Card Factory (LSE:CARD) +13.2% on the week

Card Factory jumped higher this week following the release of a positive trading update and confirmation of its acquisition of Funky Pigeon from WH Smith for £24 million. The deal, which is expected to complete subject to regulatory approval, is aimed at accelerating Card Factory’s digital and omnichannel strategy. Management reiterated its expectations for mid-to-high single-digit sales and profit growth for FY26, and confirmed that the acquisition is expected to enhance earnings in the financial year ending January 2027.

The acquisition gives Card Factory control of an established online personalised card and gifting platform, with Funky Pigeon averaging £32 million in revenue and £5 million in EBITDA over the past two financial years. Once integrated, the combined group is set to become the UK’s second-largest online card and gift retailer. Synergies of over £5 million are targeted through fulfilment efficiencies and a unified technology platform, with Funky Pigeon’s capabilities complementing Card Factory’s in-house production and store network.

Alongside the acquisition, Card Factory reported a mid-single digit year-on-year increase in group sales for the five months to 30 June 2025. First-half profits are expected to be slightly lower due to the early investment in a new point-of-sale system, but management remains confident in delivering full-year targets. The company highlighted a strong second-half trading calendar, supported by additional operational efficiencies and ongoing benefits from its Simplify and Scale programme.

REGENCY VIEW:

Card Factory is a value-focused retail play with solid fundamentals and a forward P/E of just 6.2. The Funky Pigeon deal adds a digital growth angle to what has historically been a bricks-and-mortar success story, giving the business more ways to win in the celebration space.

Greatland Resources share prices dropped sharply lower this week following the release of its June quarter activities report, which confirmed a strong finish to FY25 but introduced higher cost guidance and a more cautious production outlook for FY26. The company reported production of 198,319 ounces of gold and 8,429 tonnes of copper in just seven months, generating over $600 million in operating cash flow. The quarter also marked the successful integration of the Telfer and Havieron assets and the completion of Greatland’s ASX listing, which raised $490 million.

FY26 guidance outlined a gold production range of 260,000 to 310,000 ounces, with an all-in sustaining cost between $2,400 and $2,800 per ounce. The company noted that the increase in forecast costs reflects the risk-weighted potential for lower gold grades from stockpiles mined before the acquisition and from certain open pit areas scheduled for development in the year ahead. Greatland plans to invest over $230 million in Telfer life extension projects and continue work on the Havieron feasibility study, which is expected to be completed in the December 2025 quarter.

The report also confirmed June quarter production of 78,283 ounces of gold and 3,729 tonnes of copper at an AISC of $1,736 per ounce. Sales for the period totalled 87,529 ounces of gold and 3,740 tonnes of copper, generating net revenue of $487 million. The company closed the quarter with $575 million in net cash and remains debt-free. Drilling activity increased during the quarter, with six rigs in operation and 27,840 metres drilled, as part of a broader programme targeting Telfer resource extensions and future mine planning.

REGENCY VIEW:

Greatland is shaping up to be a serious player in the gold-copper space, but the numbers suggest the market is already giving it plenty of credit. With a £1.7 billion market cap and a forward P/E of 11.3, there’s a lot riding on the team delivering cleanly on its growth plans and proving those forecast earnings aren’t just theoretical.

Sector Snapshot

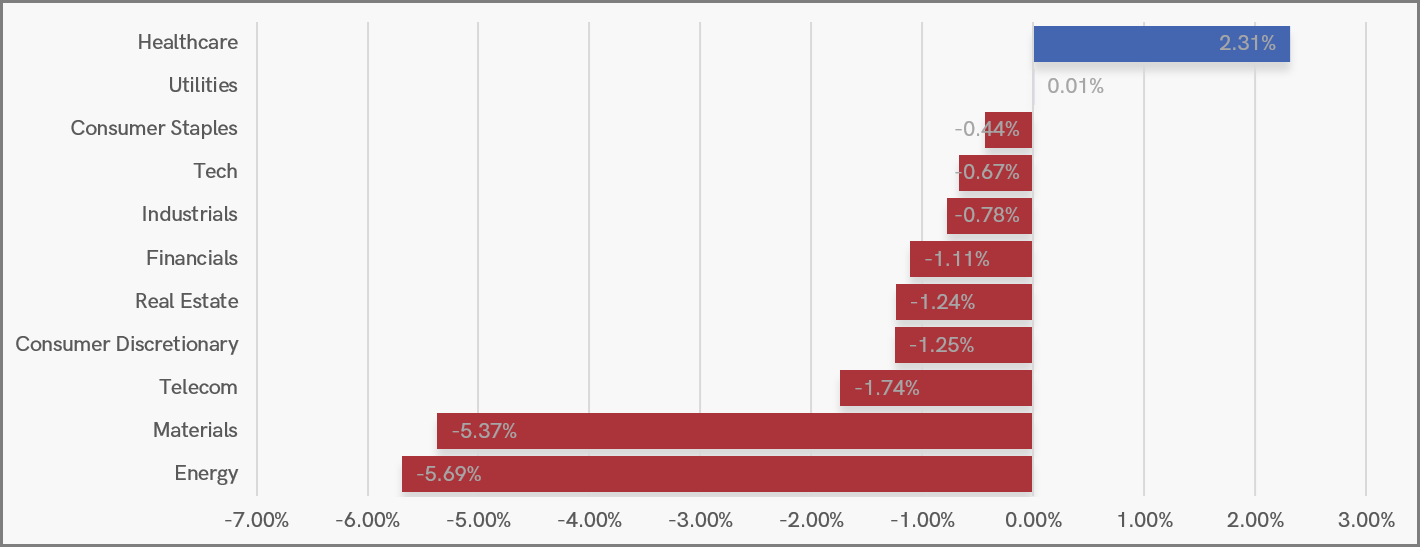

Healthcare stood out this week as the only sector delivering meaningful gains, offering a rare bright spot in an otherwise dull market. Utilities managed to hold steady, while Consumer Staples limited losses, reflecting a defensive tilt as sentiment soured.

At the bottom of the board, Energy and Materials suffered heavy losses, dragging down the broader commodities space. Telecom and Consumer Discretionary also came under pressure, while Tech and Financials edged lower in line with the risk-off tone.

UK Sector Performance (7-Days)

UK Price Action

The FTSE gave back some of its summer momentum this week, slipping below the clean ascending trendline that had guided the rally since the breakout. The move had been foreshadowed by the RSI, which showed negative divergence while in overbought territory. For now, the pullback looks contained, and attention turns to whether nearby support levels can steady the price.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.