24th Jul 2025. 8.58am

Regency View:

Update:

Regency View:

Update:

CML Microsystems powers ahead with long-term GNSS contract

CML Microsystems’ (CML) share price has had a strong month, boosted by a landmark contract valued at over $30 million…

This new agreement marks a significant milestone for the company, reinforcing its position in the global satellite technology market. The 12-year design and supply contract, signed with a leading industrial Global Navigation Satellite System (GNSS) equipment manufacturer, highlights CML’s growing role in the fast-evolving GNSS sector. The deal is a testament to the trust placed in CML’s ability to deliver advanced semiconductor solutions that meet the stringent demands of high-precision satellite applications.

CML said, this contract is not just a win, it underscores their strategic commitment to long-term growth in the satellite technology space. By securing this agreement, CML said it is enhancing its global footprint and demonstrating its capability to support the rigorous manufacturing and supply chain processes required for high-performance GNSS equipment. CML added that the inclusion of in-house production test facilities both in the UK and Silicon Valley strengthens its resilience in the face of an increasingly complex global supply chain.

The partnership highlights the company’s expertise in mixed-signal, RF, and microwave semiconductors, further solidifying its status as a key player in the communications sector. With this long-term agreement, CML is well-positioned to drive innovation in next-generation positioning technologies, ensuring its place at the forefront of the industry.

CML Daily Candle Chart

Concurrent Technologies faces market disappointment despite strong results

Concurrent Technologies’ (CNC) latest update disappointed the market, with shares continuing their pullback from recent highs.

Despite reporting record results for the first half of fiscal year 2025 (H1 FY25), the company’s stock has faced downward pressure, reflecting investor concerns and a cautious outlook. The trading update revealed impressive growth, with revenue reaching approximately £21.3 million, up from £16.8 million in H1 FY24, and a slight increase in profit before tax to £2.4 million. However, a negative impact from the USD exchange rate and the market’s reaction to the news of potential challenges have weighed on the company’s share price.

While Concurrent Technologies continues to secure design wins, which typically lead to long-term contracts, there remains a cloud of uncertainty over the company’s short-term outlook. The first half of the year saw strong order intake, amounting to £22.3 million, and a promising start to the second half of FY25. However, concerns about dependency on US defence contracts and the risk of global supply chain disruptions are starting to cloud investor sentiment. The company’s growth is also being held back by planned up-front investments in its Systems business unit, which is yet to break even, although it is on track to do so by the year’s end.

Despite these challenges, the company remains confident in its ability to meet full-year expectations. The Kratos product, launched in H1 FY25, continues to generate significant interest due to its unique features, particularly its integration with the industrial variant of the Intel® Xeon® 6 processor. The strong performance of the Products business unit and the mobilisation of the Systems business give reason for optimism, though the broader market seems to be waiting for further signs of stability before fully embracing the company’s growth potential.

CNC Daily Candle Chart

Craneware shares surge on strong FY25 update

Shares in Craneware (CRW) jumped higher last week following a trading update that exceeded market expectations…

The US healthcare fintech company reported a 12% increase in adjusted EBITDA to over $65 million, driven by strong revenue growth. With revenue climbing 9% to $205.7 million, Craneware is solidifying its position as a leader in the US healthcare market. The transition of its 340B software offerings into recurring revenue streams, alongside the company’s strong Net Revenue Retention (NRR) of 107%, underscores its successful strategy in capturing long-term, stable growth.

The group’s positive performance is further bolstered by robust operating cash conversion, which has allowed Craneware to reduce debt and strengthen its balance sheet. Total bank debt was lowered to $27.7 million from $35.4 million in the previous year, while cash reserves grew to $55.9 million. This financial strength positions Craneware well for continued expansion, particularly as it capitalises on its ongoing partnership with Microsoft. The collaboration is already enhancing the visibility of Craneware’s AI-powered Trisus platform among hospital CIOs across the US, paving the way for greater market penetration in the years to come.

Looking ahead, the outlook remains positive, with Craneware confident that the US healthcare sector’s push for greater efficiency will sustain demand for its solutions. The company’s strong backlog, fuelled by growing uptake of its 340B software and new third-party offerings, provides a solid foundation for continued growth. With accelerating EBITDA, Annual Recurring Revenue (ARR), and NRR, Craneware is well-positioned to achieve its goal of sustainable, double-digit growth in FY26. The company’s strategic role in the US healthcare ecosystem, coupled with its strong cash generation, provides confidence for the future as it continues to enhance its service offering and expand its market share.

CRW Daily Candle Chart

IXICO rise on strong revenue update and growth strategy

Shares in IXICO (IXI) have jumped following a positive trading update, with the company anticipating revenues to surpass expectations for the year ending 30 September 2025.

The neuroscience imaging and biomarker analytics leader expects revenues to reach at least £6.3 million, reflecting a 9% increase over 2024 figures. This growth cements IXICO’s return to an upward trajectory, and with the momentum expected to continue into 2026, the company is well-positioned to achieve medium-term profitability. The strong performance highlights the success of its ‘Innovate Lead Scale’ strategy, which focuses on driving scientific innovation and expanding the company’s commercial and geographical footprint in key therapeutic areas.

The company’s positive sales momentum is underscored by its increasing market presence and investment in new technologies. IXICO has successfully diversified its offerings, expanding into new market verticals and developing differentiated biomarker analytics products. These advancements in technology are expected to scale, reinforcing IXICO’s competitive edge in the neuroscience sector. Furthermore, the company’s strategy to increase investments in 2025 is aimed at driving sustained revenue growth into the coming years, with a solid cash position of at least £3.0 million expected by the end of the financial year.

CEO Bram Goorden expressed confidence in IXICO’s progress, noting that the company’s disciplined execution of its growth strategy is delivering tangible results. The ability to expand into new therapeutic areas and refine its technology platform is setting the stage for continued commercial success.

IXI Daily Candle Chart

Johnson Service Group drop following trading update

Johnson Service Group (JSG) dropped sharply earlier this month following the release of its trading update for the six months to 30 June 2025. Despite reporting a 5.5% increase in revenue, reaching £257.6 million, the company faced challenges that weighed on investor sentiment. The Group’s performance in its HORECA division was affected by a slower start to the summer season, reflecting broader issues in the hospitality market. Although the company observed a slight improvement in volumes over the last two weeks, uncertainty around future consumer discretionary spending has created concerns for the second half of the year.

Despite stable performance in the Workwear segment and strong new installations, the company remains cautious about the broader economic environment. Operating costs are being tightly managed, particularly in anticipation of the typically busy summer months in HORECA. While the company remains on track towards its targeted margin of 14% by 2026, these ongoing market challenges and the unpredictable consumer spending outlook have dampened investor confidence. As a result, shares in Johnson Service Group saw a sharp drop, despite the company’s confidence in continued revenue and margin growth for the year.

In addition to the trading update, JSG also provided an update on its intention to move from AIM to the Main Market of the London Stock Exchange. The Group confirmed that its ordinary shares will be admitted to the Main Market on 1 August 2025, with the shares to be cancelled from AIM on the same day. While the move is a significant step for the company, the absence of a fund-raising initiative alongside this transition leaves some investors cautious. The market will closely monitor the company’s next steps as it navigates through the current challenges in both its HORECA and Workwear divisions.

JSG Daily Candle Chart

Netcall break new trend highs on strong FY25 update

Netcall (NET) shares surged to new trend highs this week following the release of a robust FY25 trading update, which highlighted significant growth and momentum across the company’s core cloud and AI offerings.

The Group reported a 23% increase in revenue, reaching £48.0 million, driven by organic growth and contributions from recent acquisitions. Adjusted EBITDA grew by 17%, reaching £9.8 million, underpinned by continued profit growth and strategic investments in the Liberty Cloud platform. The sharp rise in Cloud Annual Contract Value (ACV) by 52% to £33.9 million, with 26% of that being organic growth, demonstrates the accelerating adoption of AI and automation capabilities, and underscores the strong market demand for Netcall’s solutions.

A key highlight of the update was the strong performance of the Liberty Cloud platform, which now accounts for 80% of Netcall’s total ACV. The growing success of the platform, bolstered by its enhanced AI capabilities, is driving substantial recurring revenues, with the Group’s overall ACV increasing by 31%. This reflects both expansion within existing customers and an uptick in new customer wins, particularly in the Public Sector, where Netcall’s ability to deliver rapid, measurable outcomes has resonated. The integration of strategic acquisitions, including Govtech and Parble, has further extended the company’s reach in key verticals, unlocking cross-selling opportunities and contributing to a robust pipeline for future growth.

Netcall’s cash position remained strong at £27.2 million, despite the £12.5 million spent on acquisitions during the year. The company’s debt-free status and strong cash generation put it in an excellent position for continued growth, both organically and through further acquisitions. With a solid base of recurring revenues, a record pipeline, and market tailwinds supporting the company’s trajectory, Netcall is well-positioned for the next phase of growth. The accelerating momentum in cloud adoption and the successful integration of AI into its platform suggest that Netcall will continue to expand its footprint and capture increasing market share in the rapidly evolving digitalisation and automation sectors.

NET Daily Candle Chart

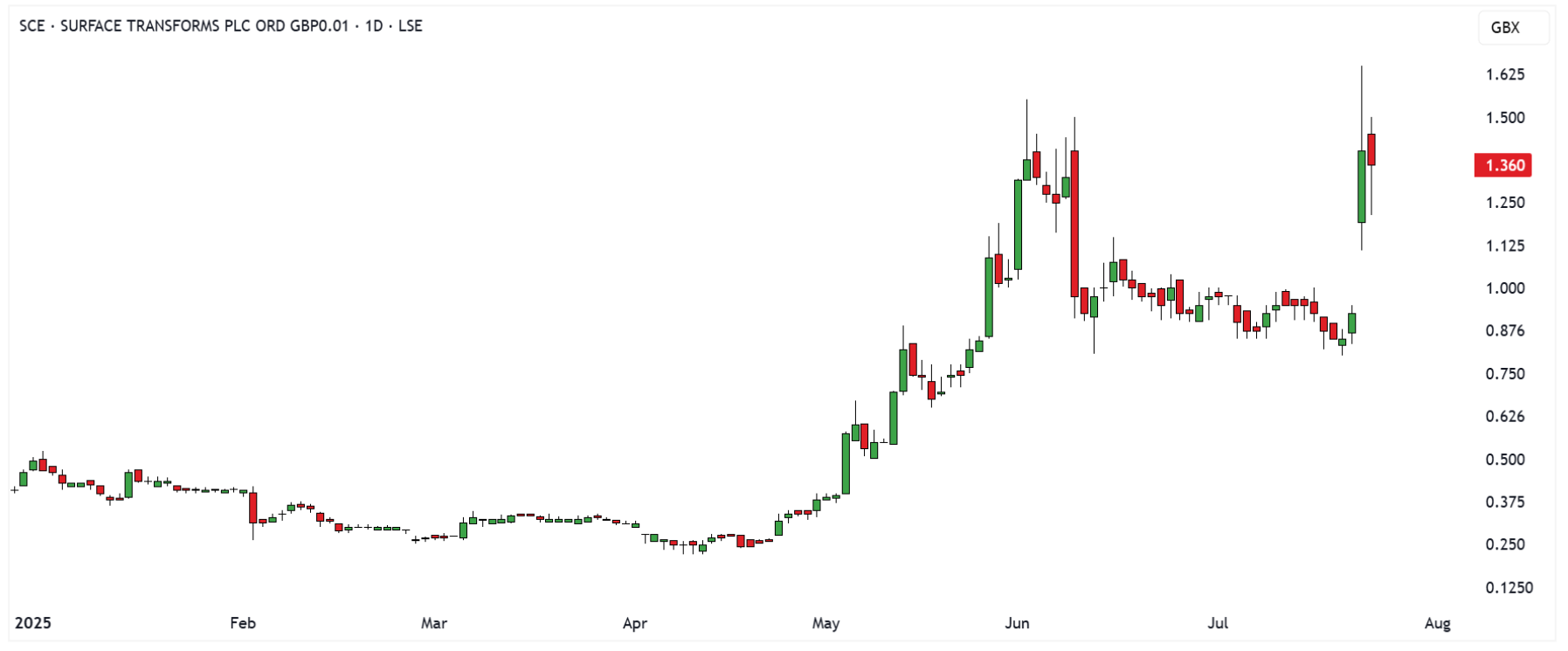

Surface Transforms on the road to recovery as operational gains drive growth

Shares in Surface Transforms (SCE) continued their recent recovery following a trading and operational update for the six months ended 30 June 2025, revealing significant progress in manufacturing yield and financial performance.

The company, known for its carbon fibre reinforced ceramic automotive brake discs, reported a 72% increase in revenue to £8.1 million, driven by a substantial improvement in manufacturing yield, which rose to 77% in Q2 2025 from 49% in Q1. This operational breakthrough has enabled Surface Transforms to address previous ramp-up challenges and reduce production disruptions, positioning the company to meet customer order patterns and move towards financial sustainability.

Despite the challenges of ramping up production, Surface Transforms has secured strong support from key customers, resulting in cash advances of £12.9 million by 30 June 2025. This financial backing has been critical in enabling the company to continue its operational improvements, and repayment of these advances is expected to begin in H2 2025. While gross cash at the end of H1 2025 stood at £1.2 million, a careful focus on cash management has allowed the company to sustain its growth trajectory. With H2 2025 revenues expected to grow by approximately 20% compared to H1, Surface Transforms is cautiously optimistic about continuing its momentum, with further improvements in yield and output forecasted.2

The company’s operational focus and improved financial position were further underscored by the appointment of Gareth Laker as the new COO, effective 1 August 2025. Laker, who has been with the company for two years, brings valuable experience from his time as an international automotive plant manager and has played a pivotal role in the company’s operational improvements. CEO Kevin Johnson expressed cautious confidence in the company’s ability to maintain these improvements in the second half of the year, noting that there is still room for further operational enhancements to ease financial pressure. With strong customer support and the company’s growing operational stability, Surface Transforms is set to continue its positive momentum in the coming months.

SCE Daily Candle Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.