3rd Jul 2025. 9.02am

Regency View:

BUY Gaming Realms (GMR) Second Tranche

Regency View:

BUY Gaming Realms (GMR) Second Tranche

Slingo reloaded: Why we’re buying a second tranche of Gaming Realms

Back in May 2024, we made the case for Gaming Realms (GMR) as a high-quality, underappreciated way to ride the growth of online gambling in the US and beyond.

Since then, the mobile-focused content licensor has gone from quiet performer to full breakout. The fundamentals have never looked stronger, and now the chart is finally catching up.

A licensing business that prints cash

Gaming Realms is a mobile gaming content company, best known for Slingo which is a hybrid of slots and bingo. It licenses out to online casino operators across regulated markets. This licensing model is capital light, highly scalable, and increasingly profitable as the group grows its partner network and distribution footprint.

The company reported record results for 2024, with revenue up 22% to £28.5m and adjusted earnings (EBITDA) climbing 30% to £13.1m. It’s worth pausing on that margin, nearly half of every pound in revenue is dropping through to EBITDA. That’s the power of the licensing model. No heavy R&D costs, no bloated marketing budgets, just content deals that keep compounding.

Licensing now accounts for 86% of group revenue and nearly all of its profit. And the trajectory remains steep. Unique players were up 22% last year, the number of distribution partners rose to 44, and 12 new Slingo titles hit the market. All of this adds leverage to what’s already a high-return model. Return on equity hit 30% last year, while operating margins reached 28%.

Perhaps most impressive, Gaming Realms remains debt free and finished the year with £13.5m in cash. That’s allowed the board to announce a £6m share buyback which is a rare move for a growth stock of this size and one that speaks volumes about their confidence in the model.

Breaking America

The core of the bull case back in 2024 was simple: online gambling is going mainstream in the US, and Gaming Realms is one of the few UK-listed plays with meaningful exposure. That theme is still intact and if anything, the pace of expansion has accelerated.

North America is now the company’s largest market, contributing 54% of content licensing revenue in 2024. Growth in the region hit 59% year-on-year, with launches in West Virginia, Michigan, Pennsylvania, and Connecticut through partners like FanDuel and Fanatics. The group has also landed deals with PENN Entertainment and BetMGM, adding further weight to an already impressive US roster.

The international story is building too. The company recently entered the newly regulated Brazilian market, going live with four partners within weeks of the green light. Launches in British Columbia and South Africa are on deck for 2025, giving Gaming Realms exposure to three high-growth markets that most UK investors are overlooking.

It’s also worth noting that GMR is doing this with zero reliance on gimmicks. This isn’t a brand-heavy, high-burn operator trying to out-market its rivals. Instead, it’s becoming the engine room behind some of the fastest-growing online casinos, offering partners unique, sticky content that keeps users engaged.

GMR Slingo

Strong foundations, stronger price action

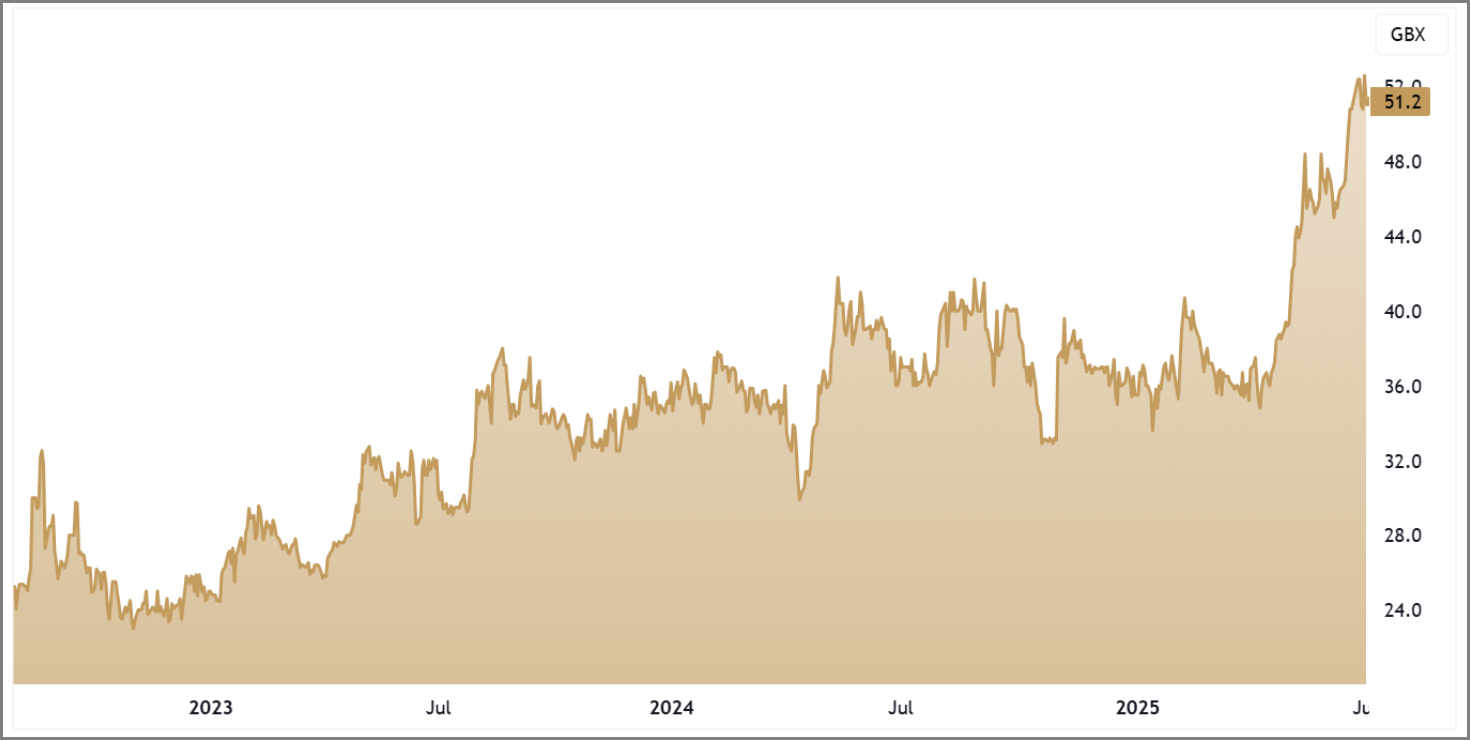

While the business has been humming along for some time, the share price took a breather in 2024. Volatility in the wider tech space, coupled with lacklustre small cap sentiment, kept Gaming Realms stuck in a range between 30p and 40p for most of the year.

That’s now changed. After quietly building support around its 50- and 200-week moving averages at the start of the year, the shares began to rally in April and haven’t looked back. Volume picked up, price pushed through the April 2021 highs, and the breakout has held firm.

What makes this move more compelling is that it hasn’t been sparked by a single news announcement. There’s been no flashy RNS or market-moving deal just consistent buying, underlining the strength of the business and a growing appetite from investors looking for quality growth at a reasonable price.

GMR Weekly Candle Chart

Valuation still offers headroom

Despite the breakout, GMR isn’t expensive. The forward PE is 14.5, with EPS forecast to grow 16.6% this year. The PEG ratio sits right around 1.0, which is typically considered fair value for a quality growth stock. EV/EBITDA of 11.6 also looks reasonable, especially when stacked against peers in the digital gaming and IP licensing space.

The quality metrics remain excellent: high return on equity (30%), solid return on capital employed (22.9%), and a consistently rising book value per share. This isn’t a one-hit wonder. It’s a profitable, well-run business with a global rollout story and plenty of room to scale.

Add in the fact that the company generates strong free cash flow and has committed to buying back shares, and it’s clear that management sees the disconnect too.

We’re not buying this breakout because we’re chasing price. We’re buying it because the technicals have caught up to a story that’s been quietly compounding for years. That kind of alignment doesn’t come around often.

GMR 3-Year Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.