20th Jun 2025. 10.44am

Weekly Briefing – Friday 20th June

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | -0.20% |

| FTSE 250 | +0.36% |

| FTSE All-Share | -0.12% |

| AIM 100 | -0.72% |

| AIM All-Share | -0.36% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 20th June

Market Overview

Dear Investor,

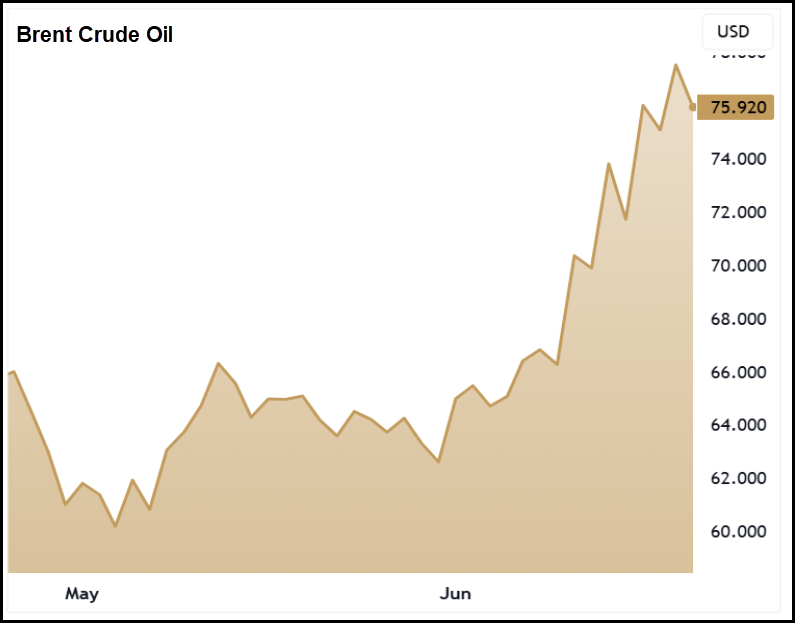

This week has been all about the Middle East. The escalating conflict between Israel and Iran has dominated the headlines and pushed oil prices sharply higher, reigniting fears of supply disruption through the Strait of Hormuz. That narrow stretch of water, just 21 miles wide at its tightest point, carries around a fifth of the world’s crude. When things flare up there, the oil market tends to pay attention.

On the ground, the risk is clear, but so far, the impact on supply has been more about fear than fact. Tankers are still moving through the strait, though with more caution, and insurers have hiked rates by more than 60% for ships heading into the region. That tells you sentiment has shifted. The US is flexing its muscles, with more naval assets moving into position, and President Trump has signed off on a plan to strike Iranian nuclear facilities, although he hasn’t yet made the final call. In Tehran, the mood is defiant. Iran’s Supreme Leader rejected demands for surrender and promised a steep price for any intervention. It’s tense, but still contained.

At the same time, the International Energy Agency dropped a bit of a reality check. In its latest report, the IEA expects oil supply to outpace demand this year, with production rising by 1.8 million barrels a day. Demand growth is soft, particularly in China and the US, and inventories are building fast. Unless something blows up in a literal sense, it’s hard to see a sustained structural rally in crude. That’s not to say there won’t be short-term volatility, this is still a headline-driven market, but the longer-term fundamentals look well supplied.

UK energy stocks have been among the biggest beneficiaries. BP is up more than 9% from this month’s swing lows as crude strength and broader risk appetite for the sector returned. On the flip side, travel names like EasyJet have taken a hit, down more than 9% from last week’s highs as higher fuel prices, airspace closures and longer reroutes all start to bite.

Outside of the energy sensitive sectors, the markets reaction has been mild and we would expect it to stay that way unless we see a significant change in stance from the US.

Wishing you a fantastic weekend in the sun,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: The Works (AIM:WRKS) +30.3% on the week

TheWorks shares have gained strongly following the company’s May trading update, which included an upgrade to profit guidance for both FY25 and FY26. The retailer reported a solid Q4 performance, with like-for-like store sales rising 6.9% and a return to flat online sales after earlier fulfilment issues.

Since the update on 16 May, the shares have risen more than 140%, reflecting investor optimism about the progress of the company’s ‘Elevating The Works’ strategy. The group highlighted sustained margin growth, cost-saving measures, and a more efficient store estate as key drivers behind the improved profitability.

Pre-IFRS 16 adjusted EBITDA increased to approximately £9.5m for FY25, compared with £6m the previous year, exceeding market expectations. The company also confirmed plans to complete the transition to a new third-party logistics provider by autumn 2025, which is expected to deliver further cost savings and improved service levels.

Overall, the trading update signals a positive turnaround in performance and a stronger outlook for the year ahead.

REGENCY VIEW:

The Works is demonstrating solid operational progress with sustained margin improvement and a clear focus on cost efficiency, supporting its upgraded profit guidance for FY26. With the shares showing strong momentum, it’s a case of carefully timing the entry – our AIM Investor service will be watching this stock closely in the coming months.

Shares in Revolution Beauty dropped sharply this week following confirmation that Frasers Group has abandoned its interest in acquiring the troubled cosmetics retailer…

The announcement, made on Thursday, sent Revolution’s shares down as much as 9% in early trading, as investors digested the news that one of the highest-profile potential bidders had stepped back from the formal sale process. Frasers, which has acquired strategic stakes in several distressed UK retail names including THG and Boohoo, had been seen as a likely suitor given its recent pattern of opportunistic acquisitions.

Revolution Beauty launched a formal sale process in May, prompted by a challenging period of trading, shareholder disputes, and the financial burden of a legal settlement with its co-founder. The group also continues to face pressure from stock clearances and a looming refinancing deadline, with its £32m credit facility set to expire in October. Market value has now dropped below £25m which is down over 95% since its 2021 IPO at 170p per share and the company has warned that failure to secure new funding could jeopardise its position further.

Despite Frasers’ withdrawal, Revolution said it remains in “constructive engagement” with several other interested parties. It confirmed that multiple proposals have been received and are being evaluated, though it stressed there is no certainty any offer will be made. In parallel, management is continuing discussions with shareholders around a potential equity raise as it seeks to stabilise its balance sheet.

REGENCY VIEW:

Revolution Beauty remains a highly distressed name with deep structural issues. Profitability is elusive, the balance sheet is fragile, and with a forecast PE of 122, the valuation reflects hope rather than fundamentals. Unless a credible bidder emerges or the business executes a radical turnaround, it’s hard to see this as anything other than a value trap dressed in lipstick.

Sector Snapshot

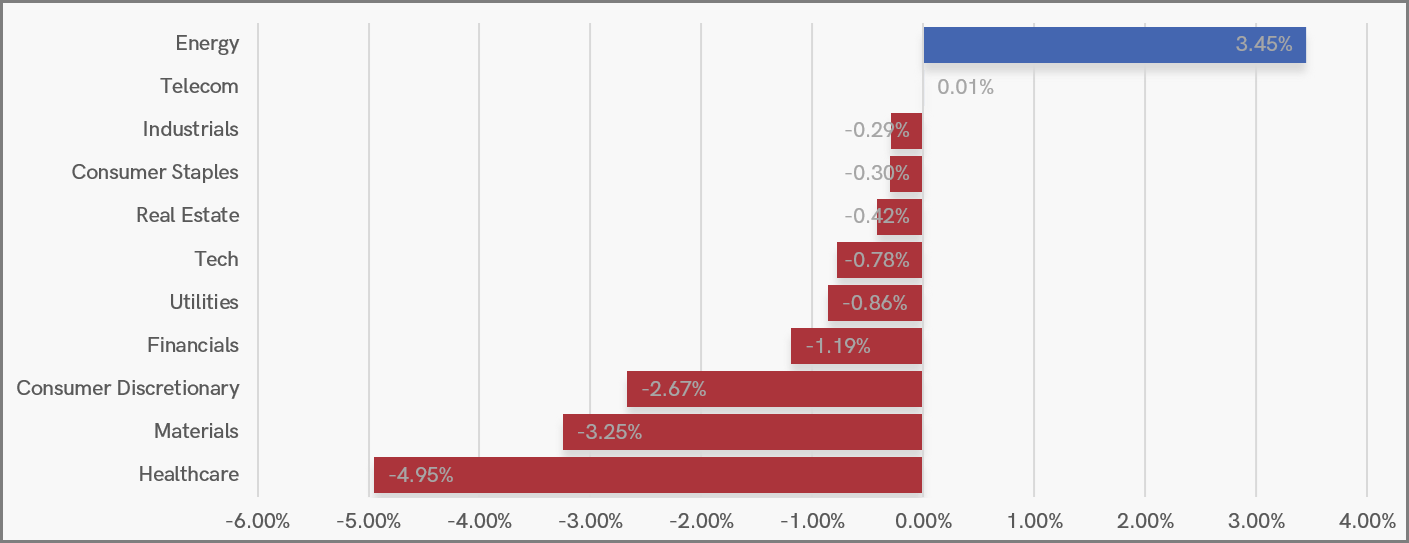

It was a broadly negative week for UK equities, with only Energy managing to post meaningful gains as investors responded to the war in the Middle East. Telecoms held steady, while Industrials and Consumer Staples showed relative resilience despite the wider pullback.

At the bottom of the table, Healthcare led the declines in a sharp reversal from recent strength, followed by steep losses in Materials and Consumer Discretionary. The overall tone suggests a shift to risk-off, with selling pressure concentrated in more economically sensitive and growth-oriented sectors.

UK Sector Performance (YTD)

UK Price Action

We mentioned last week that it was ‘breakout or fakeout’ time for the FTSE, but what we’ve seen over the past few sessions has been far less dramatic. Prices have wilted at resistance like a house plant in the summer sun, with no strong signs of rejection or momentum either way. For now, it’s sensible to assume the FTSE’s long-term trend remains the dominant force, and that prices may yet make another attempt to break through resistance in the sessions ahead.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.