12th Jun 2025. 9.05am

Regency View:

Update

Regency View:

Update

Filtronic flies on record SpaceX deal

Shares in Filtronic (FTC) have continued to power higher following the announcement of its largest contract to date, a landmark $32.5 million follow-on order from SpaceX for its high performance E band Cerus 32 Solid State Power Amplifiers. This contract, which will be materially fulfilled in FY2026, marks a significant milestone in Filtronic’s transformation into a key supplier within the booming low Earth orbit satellite market. It not only confirms SpaceX’s growing reliance on Filtronic’s RF technology but also underscores the company’s position as a mission critical enabler of next generation space communications infrastructure.

The deal follows the March 2025 extension of Filtronic’s Strategic Partnership with SpaceX, under which this latest order has triggered the full vesting of 10.95 million share warrants, representing 5% of Filtronic’s share capital. In total, nearly 10% of the company’s shares are now subject to vested warrants, a tangible reflection of the deepening relationship between the two firms. This high level of contractual and equity commitment is rare in the small cap tech landscape and provides investors with a clear signal that Filtronic is becoming increasingly embedded in the low Earth orbit supply chain. Meanwhile, unvested warrants tied to the success of new technology suggest further upside potential as the company rolls out its development roadmap.

Filtronic’s leadership has responded by doubling down on R&D investment, with CEO Nat Edington highlighting the size of the market opportunity and the momentum gained from recent wins. With the board now confident that FY2026 revenues will exceed current expectations, investors appear to be pricing in the step change in earnings visibility and long term growth. As the global space economy continues to accelerate, this deal cements Filtronic’s credentials as a UK listed tech firm with real commercial traction in one of the most exciting high growth sectors.

FTC Daily Candle Chart

GBG drops despite profit growth and main market plans

GBG (GBG) dropped sharply this week after releasing full year results that, while solid on paper, appear to have underwhelmed investors looking for clearer top line momentum or a more bullish outlook. Revenue rose just 3% on a constant currency basis to £282.7 million, a modest improvement that was largely in line with prior guidance. The core Identity and Location businesses showed positive net revenue retention, and adjusted profits grew nearly 10% to £67 million, helped by margin expansion. But despite the profit growth and a 14.9% jump in earnings per share, the market reaction suggests disappointment around either the pace of revenue growth or perhaps concerns over the continued decline in the Fraud segment.

Adding to the uncertainty may be the lack of any material upgrade to the outlook. While GBG confirmed that the new financial year has begun in line with expectations, no change was made to full year guidance, which may have been viewed as conservative given the improvements in profitability and cash generation. The Group has taken steps to reposition for long term growth, including operational fixes in the Americas Identity division and the ongoing development of GBG Go, a new platform that aims to unify the firm’s identity capabilities. However, these longer term ambitions are yet to translate into clear revenue acceleration, and it seems investors were hoping for stronger early evidence of impact.

Perhaps most notably, GBG also announced its intention to move from AIM to the Main Market, a sign of growing maturity and confidence in its strategic direction. The company returned over £21 million to shareholders through buybacks and dividends in the year and has reduced net debt to £48.5 million, giving it flexibility for further investment. Yet despite these positives, the sharp sell off reflects a market keen to see more convincing growth at the top line, not just improved margins. The transition may take time to fully re rate in investors’ eyes, especially in a market increasingly focused on revenue momentum and platform scalability.

GBG Daily Candle Chart

GlobalData ends buyout talks with ICG and KKR

GlobalData (DATA) has officially ended takeover talks with private equity group ICG, bringing to a close months of speculation around a potential acquisition. ICG confirmed it would not be making a bid, following the collapse of earlier negotiations with KKR in May. No further details were provided by either party, but the breakdown marks the end of a strategic review that began in April.

Global Data had been in discussions over a possible cash offer that also included an option for unlisted equity. These talks had initially attracted strong interest from both ICG and KKR, but neither has now chosen to proceed.

With the June 11th deadline for ICG now passed, GlobalData remains an independent company. The end of discussions could provide some clarity for investors, although it leaves questions over the company’s next steps for growth and shareholder value creation.

DATA Daily Candle Chart

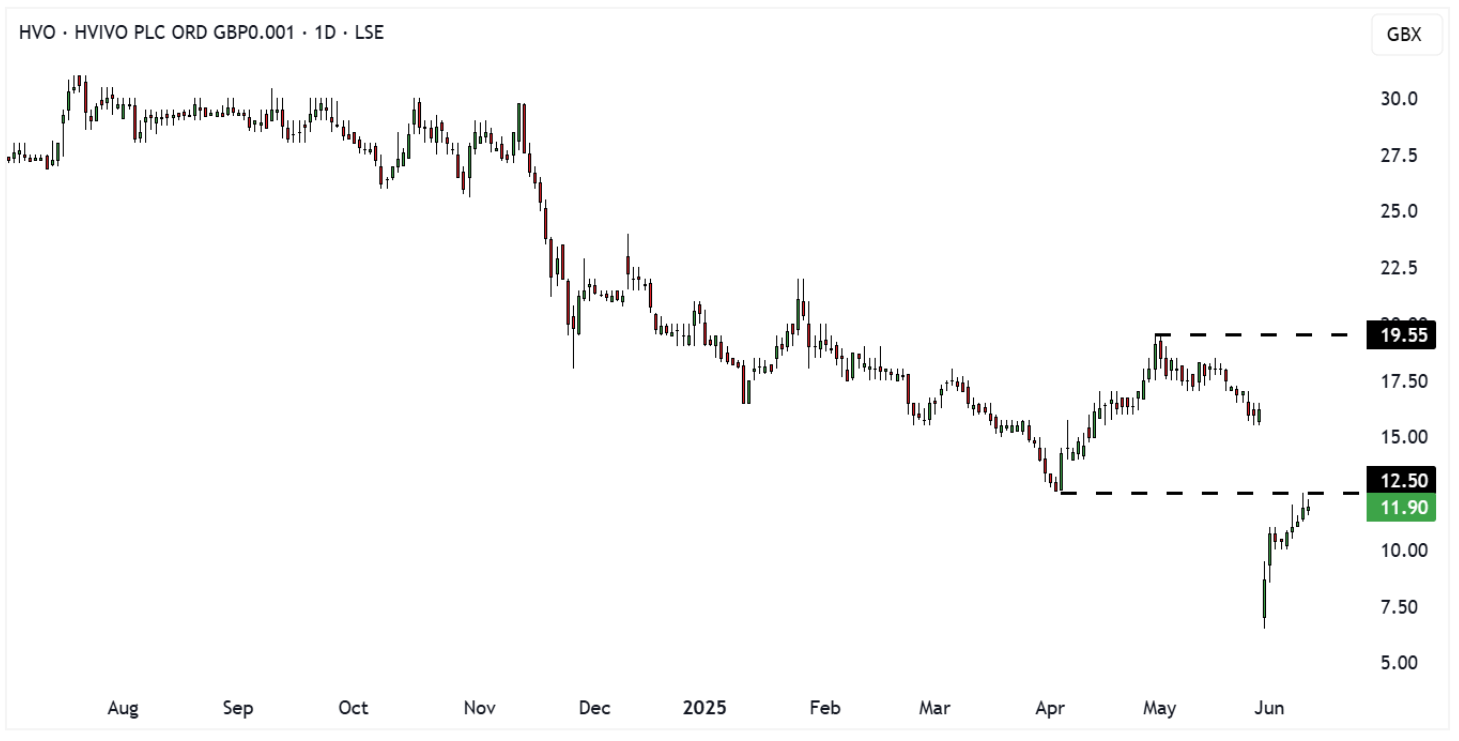

hVIVO slumps on contract cancellations and industry headwinds

hVIVO’s (HVO) share price gapped significantly lower at the end of May due to the unexpected cancellation of a major human challenge trial contract, alongside the postponement of another and a further smaller cancellation. The company attributed these developments to broader macro uncertainty across the pharmaceutical and biotech landscape, particularly in the US, where a tough funding environment and regulatory delays are prompting CRO clients to defer or abandon trials. While this disruption is being felt across the industry, the scale and timing of hVIVO’s cancellations caught investors off guard, raising near-term concerns over revenue visibility for FY25.

The company moved quickly to reassure shareholders, stating that £47 million of revenue remains contracted for FY25, even after accounting for cancellation and postponement fees. While that figure provides a base level of cover, management acknowledged that unless further contract wins are secured, this could result in a mid single digit operating loss for the year, excluding exceptional items. That statement likely added to the pressure on the share price, with the market quick to factor in the downside scenario. Encouragingly, the company emphasised that nearly all FY25 contracts have already commenced, reducing the risk of further cancellations, and promised a more detailed trading update in July.

Despite the setback, hVIVO remains upbeat about its long-term prospects. The sales pipeline is at a record high, including major contracts under discussion that could begin in late 2025 and deliver substantial revenue in FY26. CEO Dr Mo Khan also highlighted the successful integration of CRS and Cryostore, as well as growth in new revenue streams like hLAB services and early phase clinical trials. The company maintains a strong cash position and insists its strategy to build a diversified, sustainable CRO remains intact. But in the short term, investor sentiment is likely to remain cautious until more clarity emerges on new contract wins and the broader recovery in biotech funding.

HVO Daily Candle Chart

IG Design jumps after exiting struggling US business

IG Design (IGR) jumped higher recently following news of the disposal of its entire US operations, DG Americas, in a bold move to streamline the group and draw a line under years of underperformance. The disposal, announced on 30 May, will see the division transferred to a vehicle backed by Hilco Capital. While the headline consideration is a nominal one US dollar, the deal includes a potential share of future sale proceeds—should the new owner realise value from the business. IG Design will receive 75% of any such proceeds, though there is no guarantee any will materialise.

DG Americas has been a long-standing drag on group performance, caught in the crossfire of a shrinking US retail environment, customer bankruptcies and more recently, a fresh wave of trade tariffs that have hit margins and order volumes. In FY24 the division generated $500 million in revenue but only delivered $4.9 million in pre-tax profit, and the board made it clear that further deterioration was expected. With another seasonal working capital squeeze approaching, IG Design opted to act decisively and cut its exposure.

While the near-term financial impact of the disposal will include a non-cash write-down and the loss of trading contribution from DG Americas, the market responded positively to the clarity and simplification of the group structure. Investors appear to have welcomed the company’s renewed focus on its core international business across the UK, Europe and Australia, where it retains strong retail partnerships and healthier margins. The move also paves the way for new financing arrangements, with a three-year agreement expected to be finalised by the end of June.

IGR Daily Candle Chart

Mitie confirms £366m acquisition of Marlowe in cash-and-stock deal

Marlowe (MRL) has confirmed that it will be acquired by FTSE 250-listed Mitie Group in a deal worth approximately £366 million. The agreement, which combines cash and new shares, will see Marlowe shareholders receive 290p in cash plus 1.1 new Mitie shares for each share held. The offer values Marlowe at around 466p per share and represents a 26.5% premium to its price before the initial talks were announced. Marlowe shares rose nearly 8% on the news, while Mitie shares dropped around 10% in early trading.

Mitie is a long-standing holding in our FTSE Investor portfolio and this acquisition adds significant depth to its compliance and risk management offering. Marlowe brings expertise in safety inspections and regulatory services, which complements Mitie’s existing operations in fire and security, as well as air and water hygiene. As part of the transaction, Mitie has paused its £125 million share buyback programme to help fund the purchase, which may explain the initial negative market reaction.

The acquisition underscores a broader trend of consolidation in the UK business services sector, with Mitie strategically positioning itself to capture more value in regulated and recurring revenue markets. Marlowe, which features in our AIM Investor portfolio, will now become part of a larger and more diversified platform. The deal is expected to close later this year, subject to shareholder and regulatory approvals.

MRL Daily Candle Chart

Inspecs eyes steady 2025 despite US tariff drag

Inspecs (SPEC) provided a cautious but measured update at today’s AGM, as outgoing Chair Robin Totterman acknowledged the drag from ongoing US tariff uncertainty. Group sales were down year-on-year by the end of May, with American demand proving unpredictable. However, management noted that momentum is picking up in Europe, and key projects with major retailers in the US and Canada remain on track, suggesting that H2 could offer some recovery in volumes if macro conditions stabilise.

The strategic review of Norville, Inspecs’ lens business, remains ongoing and is expected to conclude by the end of June. While no outcome has been confirmed, the review signals that the board is open to restructuring underperforming parts of the Group to sharpen its focus and improve profitability. Alongside this, the company is actively recruiting a new Independent Non-Executive Chair and CFO, which will be important steps in shaping the next phase of leadership as Totterman steps down after more than three decades at the helm.

Despite a challenging start to the year, Inspecs is maintaining its full-year revenue and EBITDA guidance, supported by ongoing operational efficiency measures and cost-saving initiatives. These are expected to ramp up into the second half of the year, helping to buffer the Group against macro headwinds. As the leadership baton is passed, Inspecs is entering a transition period, but with a clear focus on returning to growth and delivering long-term shareholder value.

SPEC Daily Candle Chart

Science Group cashes in as Ricardo agrees sale to WSP

Science Group (SAG) is set to receive a windfall of £53.5 million after agreeing to sell the majority of its stake in Ricardo to Canadian firm WSP Global, which has announced a £363 million takeover of the UK-based environmental and engineering consultancy. The all-cash deal values Ricardo shares at 430p, representing a 28.4% premium to the previous day’s close.

The sale marks a victory for Science Group, which has been actively pushing for structural change at Ricardo over recent months, citing strategic underperformance. As the company’s second-largest shareholder, Science Group had called for the removal of senior board members and encouraged a broader review of the business, paving the way for a sale.

With the deal now on the table, Science Group has confirmed it supports WSP’s offer and will seek an adjournment of Ricardo’s general meeting, originally scheduled for 18th June. The decision not only delivers immediate value but also strengthens Science Group’s own balance sheet, potentially opening the door to further strategic investments.

SAG Daily Candle Chart

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.