6th Jun 2025. 10.15am

Weekly Briefing – Friday 6th June

| Market | Movement this week (%)* |

|---|---|

| FTSE 100 | +0.49% |

| FTSE 250 | +0.23% |

| FTSE All-Share | +0.46% |

| AIM 100 | +1.48% |

| AIM All-Share | +1.42% |

* Price movement from Monday's open at 8am

Regency View:

Weekly Briefing – Friday 6th June

Market Overview

Dear Investor,

This week brought a heavy dose of reality from the world’s economic heavyweights. The OECD slashed its global growth forecasts, blaming Trump’s renewed trade war for dragging momentum to post-Covid lows. The numbers say it all. US growth is now expected to nearly halve to just 1.6% in 2025. The tariffs, which have pushed the average US rate above 15%, are the highest we’ve seen since World War II. This isn’t just a US problem either. The economic hit is radiating outwards, with the OECD cutting forecasts for three-quarters of the G20 including the UK.

From a UK perspective, this comes at an awkward time. The economy is crawling forward, and any disruption to global trade or investment is going to add weight to already tired legs. The OECD now sees UK growth at just 1.3% this year, slipping to 1% in 2026. That’s a downgrade, albeit a modest one, but it underlines how vulnerable we are to shocks from abroad. With the Federal Reserve likely holding off on rate cuts thanks to higher US inflation, global monetary conditions could remain tighter for longer, yet another headwind for businesses and households here at home.

And then there’s China. Manufacturing activity there just posted its worst monthly drop since 2022. The Caixin PMI slumped to 48.3, with new export orders collapsing. The message is pretty simple – Trump’s tariffs are biting, and demand is buckling. Add in a shaky property sector, stubborn deflation and a job market under pressure, and suddenly that ‘engine of global growth’ looks like it’s misfiring. Beijing is cutting rates and trying to loosen the purse strings, but the stimulus so far feels more like patchwork than a bold fix.

Despite all this gloomy data, markets seem surprisingly unfazed. Investors are clearly betting that the weak numbers will spur central banks to ease monetary policy sooner rather than later. The hope is also that Beijing will step up with more substantial stimulus measures to revive growth. This cautious optimism is keeping stocks afloat, even as the economic backdrop darkens.

What does all this mean for UK investors? For starters, we may need to reassess the global earnings picture. Trade-sensitive sectors and exporters could feel the chill, particularly if demand from China and the US keeps softening. Domestically focused companies may offer some shelter, especially those with pricing power and resilient margins. But overall, the narrative is moving from recovery to resilience, and that usually calls for a more cautious stance.

Wishing you a fantastic weekend,

Tom

Thomas Light – Chartered FCSI

Director of Research

Market Movers

On the rise: Doc Martins (LSE:DOCS) +24.3% on the week

Shares in shoe maker Dr. Martens leapt higher this week after the company delivered a reassuring set of full-year results and outlined a clear strategy to get the business back on a growth footing…

While revenue fell 10% and adjusted pre-tax profit dropped to £34.1 million, management hit all four of its turnaround objectives for the year. These included returning direct-to-consumer sales in the Americas to growth, refocusing marketing on the core product range, delivering £25 million in annualised cost savings and significantly strengthening the balance sheet. Investors also welcomed the sharp reduction in net debt and confirmation of the final dividend.

The new leadership team has laid out a strategy called Levers for Growth, with the goal of repositioning Dr. Martens as the world’s most-desired premium footwear brand. The business is shifting from a channel-led model to one that puts the consumer at the centre, aiming to increase both product purchase occasions and market reach. Distribution will be tailored by region, blending wholesale and direct channels depending on what works best locally. Management is focused on improving full-price sales, simplifying the operating model and capitalising on the brand’s strength in markets like China and Japan, where demand remains robust.

Guidance for a return to profit growth in the current financial year helped support the upbeat reaction. There are still challenges, particularly in the UK and broader EMEA region where trading remains soft, and tariffs in the US add a layer of uncertainty. But a stronger wholesale order book, stable pricing and ongoing cost discipline suggest that the worst may be behind it. With the brand owning just 0.7% of a £179 billion addressable market, long-term growth potential remains firmly intact.

REGENCY VIEW:

Dr. Martens is showing real signs of life, with strong recent momentum and forecast earnings growth of over 90% helping to reignite interest in the brand. Valuation still looks reasonable at just 15.5x forward earnings and 4.1x free cash flow, making this a potential recovery story worth keeping an eye on.

Shares in Wizz Air dropped sharply following full-year results that revealed a 62% slide in operating profit, as the low-cost carrier continued to grapple with the disruptive impact of Pratt & Whitney’s GTF engine groundings. While total revenue rose 3.8% to €5.27 billion and passenger numbers reached a record 63.4 million, the gains were overshadowed by rising costs and operational inefficiencies, with over 40 aircraft grounded at year-end. Ex-fuel unit costs surged nearly 20% year-on-year, dragging EBITDA down 4.9% and taking a heavy toll on overall profitability.

Despite a stronger load factor and improved on-time performance, the sharp drop in net profit to €213.9 million from €365.9 million a year earlier reflected the ongoing pressure on Wizz’s cost base. The company has made progress in adapting to the engine challenges, receiving 26 new A321neos and 14 spare engines during the year, and expects the number of grounded aircraft to fall to around 34 by the end of the first half. However, the disruption has inflated fixed costs, reduced network productivity, and delayed margin recovery.

Looking ahead, management is optimistic that fiscal 2026 will mark a turning point. Capacity is expected to grow by around 20%, with forward bookings suggesting revenue should exceed last year’s levels. Yet the market remains cautious, as Wizz Air declined to issue formal guidance and flagged ongoing uncertainties around trading conditions, summer pricing trends, and the pace at which cost pressures will ease.

REGENCY VIEW:

Wizz Air’s stock looks battered, reflecting deep challenges with a sharp drop in momentum and a market cap that feels modest compared to its hefty enterprise value. Despite an appealing low price-to-earnings ratio and strong value scores, the company’s weak quality metrics and sliding profitability raise questions about its near-term recovery prospects.

Sector Snapshot

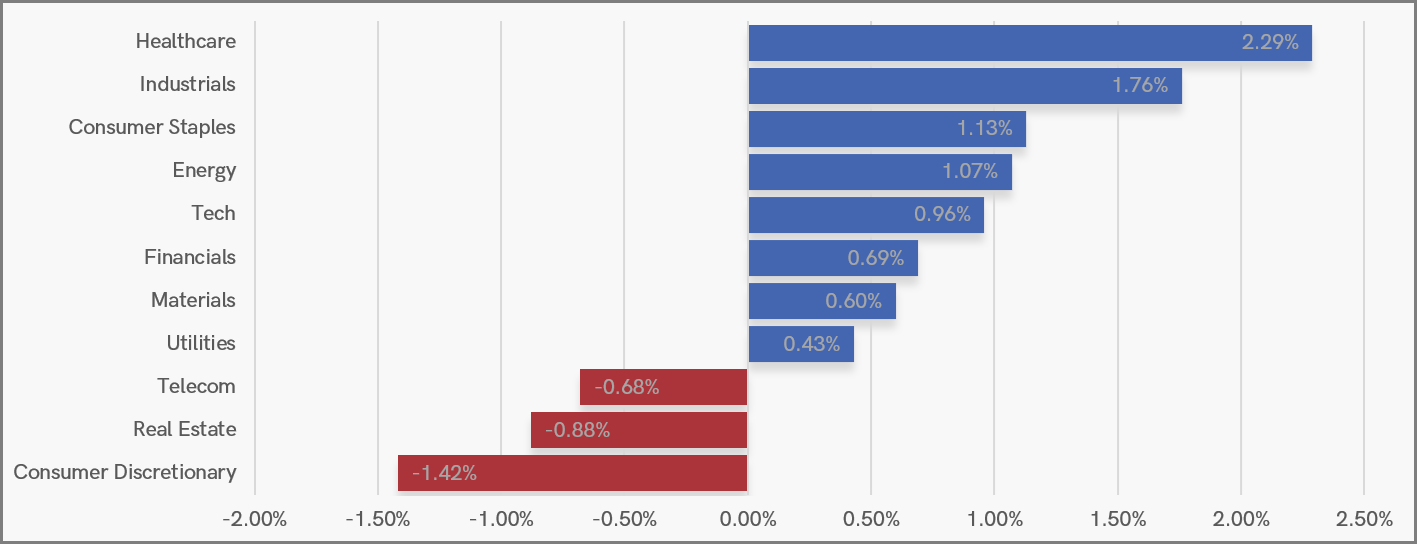

This week, Healthcare led the way with solid gains, supported by steady demand and defensive qualities. Industrials and Consumer Staples also showed resilience, benefiting from stable earnings and modest economic optimism. Energy and Tech followed closely, reflecting a balanced risk appetite across sectors.

On the downside, Consumer Discretionary struggled to find traction amid broader market caution, while Real Estate and Telecom also lagged behind. The contrast highlights a shift towards more reliable, income-focused sectors as investors navigate an uncertain backdrop.

UK Sector Performance (YTD)

UK Price Action

It’s another week of coiling and compression just below the key resistance area we’ve highlighted in previous weeks. This price action increases the potential for an explosive directional move – in what direction remains to be seen.

FTSE 100 Rolling Futures (Daily Candle Chart)

Disclaimer:

All content is provided for general information only and should not be construed as any form of advice or personal recommendation. The provision of this content is not regulated by the Financial Conduct Authority.